The New Home Company Inc. (NYSE: NWHM), Aliso Viejo, California early Thursday reported net income of $2.5 million, or $0.12 per diluted share, compared to net income of $4.3 million, or $0.21 per diluted share in the prior year period. Wall Street was looking for a gain of $0.08 per share.

The year-over-year decrease in net income was primarily attributable to a 170 basis point increase in selling and marketing expenses as a percentage of home sales revenue and a 150 basis point decline in home sales gross margin, partially offset by a 5% increase in home sales revenue, a 50 basis point improvement in general and administrative expenses as a percentage of homes sales revenue and a lower effective income tax rate.

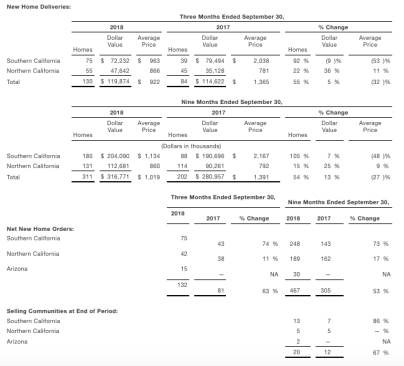

Total revenues for the 2018 third quarter were $159.1 million, compared to $157.9 million in the prior year period. Home sales revenue for the 2018 third quarter increased 5% to $119.9 million, compared to $114.6 million in the prior year period. The increase in home sales revenue was driven by a 55% increase in deliveries, which was partially offset by a 32% decline in average selling price to $922,000 as we delivered more affordably priced homes during the quarter.

Gross margin from home sales for the 2018 third quarter was 14.8% as compared to 16.3% in the prior year period. The 150 basis point decline in home sales gross margin was primarily due to higher interest costs included in cost of home sales. Home building gross margin excluding interest in cost of home sales was 18.4% for both the 2018 and 2017 third quarters. On a sequential basis, gross margin from home sales for the 2018 third quarter increased by 220 basis points as compared to the 2018 second quarter.

SG&A expense ratio as a percentage of home sales revenue for the 2018 third quarter was 12.8% versus 11.6% in the prior year period. The 120 basis point increase in the SG&A rate was primarily due to higher selling and marketing costs related to advertising for recently opened communities, increased master marketing fees, higher co-broker commissions, and higher sales personnel costs associated with increased community count. These items were partially offset by a lower G&A rate due to an increase in home sales revenue and lower compensation-related expenses.

Net new home orders for the 2018 third quarter increased 63% to 132 homes and was primarily driven by an 82% increase in average selling communities during the quarter. The monthly sales absorption rate was 2.2 sales per average selling community for the 2018 third quarter, compared to 2.5 per month in the 2017 period. The company’s active selling community count was up 67% as of the end of the 2018 third quarter at 20 communities and its cancellation rate for the 2018 third quarter was 12% as compared to 11% in the prior year period.

The dollar value of the company’s wholly owned backlog at the end of the 2018 third quarter was $310.8 million and totaled 309 homes compared to $330.6 million and 182 homes in the prior year period. The decrease in backlog dollar value resulted from a 45% lower average selling price of homes in backlog at $1.0 million as compared to $1.8 million a year ago. The year-over-year decline in the company’s average selling price of homes in backlog was driven primarily by the mix of homes in backlog in Southern California as it expanded its product offerings to include more affordably priced communities. In addition, the 2017 third quarter backlog included homes from two higher-priced luxury communities located in Newport Coast, CA that closed out during 2017.

Fee building revenue for the 2018 third quarter was $39.2 million, compared to $43.3 million in the prior year period. The fee building gross margin was $1.1 million compared to $1.5 million in the prior year period. The lower fee building margin resulted from lower revenues and a lower fee arrangement. Management fees from joint ventures and construction management fees from third parties totaled $1.7 million for the 2018 third quarter compared to $1.3 million in the prior year period.

The Company’s share of joint venture income was $34,000 for the 2018 third quarter, down from $99,000 in the prior year period. The reduction in JV income was primarily the result of lower home building gross margins and the mix of joint venture deliveries.

Joint venture net loss totaled $0.2 million, compared to a net income of $0.4 million in the prior year period. Joint venture home sales revenue totaled $24.9 million, compared to $45.2 million in the prior year period, while joint venture land sales revenue totaled $30.6 million for the 2018 third quarter, compared to $0.6 million in the prior year period.

At the end of the 2018 third quarter, joint ventures had seven actively selling communities compared to eight at the end of the 2017 third quarter. Net new home orders from joint ventures for the 2018 third quarter decreased slightly to 41 homes. The dollar value of homes in backlog from joint ventures at the end of the 2018 third quarter was $93.3 million from 107 homes compared to $69.8 million from 83 homes at the end of the 2017 third quarter.

As of September 30, 2018, the company had real estate inventories totaling $562.3 million and owned or controlled 2,903 lots through its wholly owned operations (excluding fee building and joint venture lots), of which 1,360 lots, or 47%, were controlled through option contracts. The company ended the 2018 third quarter with $44.1 million in cash and cash equivalents and $381.8 million in debt, of which $62.0 million was outstanding under its $200 million revolving credit facility. As of September 30, 2018, the company had a debt-to-capital ratio of 59.7% and a net debt-to-capital ratio of 56.6%.

“Although we made progress with the transition in our strategy during the quarter, higher home prices and interest rates have recently created buyer hesitancy at certain communities,” said Larry Webb, chairman and CEO. “While we believe this indecisiveness may prove to be temporary given the strong underlying fundamentals of our submarkets, we recognize that there may be a period of sales softness as buyers adjust to this new affordability landscape.”

Webb continued, “We continue to have confidence in the long-term outlook for our industry and our company, and as a result of this confidence, we accelerated our stock repurchase activity during the third quarter. We believe that our stock is being undervalued by the equity markets and intend to continue to buy shares in an opportunistic fashion as we position our company for long-term success.”