Meritage Homes Corp. (NYSE:MTH) after market close Tuesday reported net earnings of $25.4 million, or $0.65 per diluted share, for the first quarter of 2019 ended March 31, compared to $43.9 million, or $1.07 per diluted share, for the first quarter of 2018. The results beat the analyst consensus estimate by a penny per share.

The year-over-year reduction in earnings was due to a combination of slightly lower home closing revenue, home closing gross margin and resulting loss of overhead leverage, as well as an increase in interest expense. In addition, first quarter 2018 net earnings benefited from a favorable legal settlement of approximately $4.8 million and a lower tax rate.

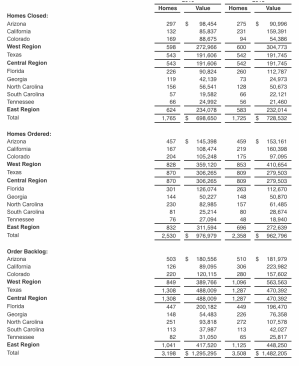

Home closing revenue decreased 4% on a 2% increase in home closing volume and a 6% decrease in average selling price over the first quarter of 2018. The lower ASP reflected the company’s strategic shift toward more affordable entry-level and first move-up homes, as well as incremental incentives offered in the fourth quarter of 2018 and first quarter of 2019. This was most evident in the West region, where home closing revenue was down 10% year-over-year on flat home closings and a 10% reduction in ASP, primarily driven by softness in California. Similarly, East region home closing revenue was up 1% on a 7% increase in closings and 6% decline in ASP. The Central region’s first quarter of 2019 was consistent with the first quarter of 2018’s closing volume and revenue.

Home closing gross profit declined 6% due to the 4% decline in home closing revenue and a 40 bps decrease in gross margin compared to the first quarter of 2018, which includes targeted incentives on slow-moving inventory or homes in communities with more competitive market conditions.

Selling, general and administrative expenses (SG&A) were 12.3% of first quarter 2019 home closing revenue, compared to 11.5% in the first quarter of 2018, due to higher brokerage commissions, severance expenses and accelerated equity compensation expense into the first quarter of 2019 due to changes in tax rules. The combined impact of these items increased SG&A for the first quarter of 2019 by approximately 50 bps over 2018. Additional expenses associated with 7% more average actively selling communities producing 4% less home closing revenue for the first quarter of 2019 resulted in a loss of leverage compared to 2018.

Other income decreased $4.3 million year-over-year, primarily due to a $4.8 million favorable settlement in the first quarter of 2018 from long-standing litigation related to a previous joint venture in Nevada.

Interest expense increased $3.9 million year-over-year, primarily due to less interest capitalized to assets under development on faster construction cycles and turnover of entry-level inventory.

First quarter effective tax rate was approximately 21% in 2019, compared to 10% in 2018, which benefited from $6.3 million of energy tax credits taken in 2018 on homes closed in 2017 that qualified for the credits. Those federal tax credits have not been renewed for homes closed in 2018 or 2019.

Total orders for the first quarter of 2019 increased 7% year-over-year, driven by a 7% increase in average active community count with an absorption pace consistent with the prior year’s first quarter. Central and East region orders grew 8% and 20%, respectively, while West region orders were 3% lower year-over-year due to a 24% decline in California, continuing a trend that began at the start of 2018 due to affordability constraints.

Partially offsetting the 7% increase in orders was a 5% decrease in ASP as the ratio of lower-priced entry-level homes increased to 45% in the first quarter of 2019 compared to 38% in the first quarter of 2018. As a result, the total value of first quarter orders increased slightly over 2018. The Central region was the only region that experienced an increase in orders ASP for the first quarter of 2019 over 2018.

Cash and cash equivalents at March 31, 2019 totaled $327.5 million, compared to $311.5 million at December 31, 2018, due to positive cash flow from operations. Real estate assets remained consistent at $2.7 billion.

Meritage ended the first quarter of 2019 with approximately 33,800 total lots owned or under control, compared to approximately 34,000 total lots at March 31, 2018. All of the lots added during the first quarter of 2019 were in communities planned for entry-level product.

Debt-to-capital ratios were 42.9% at March 31, 2019 and 43.2% at December 31, 2018, with net debt-to-capital ratios of 36.0% and 36.7%, respectively.

“Home buying activity improved throughout the first quarter of 2019, led by affordable entry-level and move-up homes, as buyers responded positively to lower interest rates and targeted incentives,” said Steven J. Hilton, chairman and chief executive officer of Meritage Homes. “We believe the demand we’ve seen so far in the spring selling season reflects sustained positive macroeconomic factors for the housing industry.

“Meritage continues to benefit from our strategic focus on the entry-level and first move-up markets, which together represented nearly 90% of our first quarter 2019 orders, driven by growing demand for more affordable homes to meet the needs of Millennials and Baby Boomers. Our first quarter orders increased 7% year-over-year and matched our first quarter 2018 six-year high absorptions pace of 9.5 orders per average community.

“We also closed more homes in the first quarter of 2019 than we did last year, despite entering the year with 15% fewer homes in backlog than we had at the beginning of 2018,” Hilton added. “We achieved those results primarily due to our strategic decision to have more spec homes ready to sell and close quickly to meet the demands of home buyers. More than two-thirds of our first quarter 2019 closings were from previously started spec homes, up from a little more than half of our closings from spec homes in the first quarter of 2018. Most of those came from our entry-level LiVE.NOW.® communities, but they also included move-up homes in inventory that we marketed with targeted incentives, especially in slower-selling communities that we are looking to close out quickly.”

He continued, “As expected, our average sales price (ASP) continued to come down as our product mix shifts further toward entry-level and affordable first move-up homes. That reduction in ASP, combined with the incentives that helped drive our order growth during the quarter, resulted in reduced home closing revenue and gross margin compared to the first quarter of 2018. However, we expect our higher backlog conversion and simplified product offerings will help us gain leverage and drive further profitability as we move through the year.”

Hilton concluded, “We are encouraged by the outlook for interest rate stability and optimistic that the spring selling season will continue as it has begun in 2019, but remain cautious in projecting quarterly results due to choppiness in the market. We are currently projecting 2019 home closings and total home closing revenue of approximately 8,200-8,700 and $3.25-3.45 billion, respectively, for the full year. We are anticipating home closing gross margin to be around 18% for the year, which we estimate will translate to approximately $4.65-4.95 diluted earnings per share.”