M.D.C. Holdings, Inc. (NYSE: MDC), Denver on Thursday reported net income of $53.4 million, or $0.93 per diluted share, for the third quarter ended September 30, down 13% from $61.2 million or $1.07 per diluted share. Analysts were expecting a gain of $0.95.

Among the results, compared to the prior-year quarter:

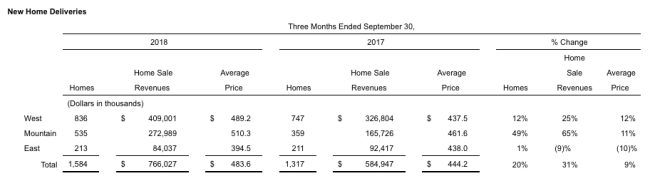

- Home sale revenues up 31% to $766.0 million from $584.9 million, homes delivered up 20% to 1,584

- Average selling price of homes delivered up 9% to $483,600

- Pretax income of $67.4 million vs. $89.7 million in 2017 third quarter

- $52.2 million gain on investments in 2017 third quarter vs $3.0 million gain in 2018 third quarter

- Excluding gain on investments, pretax income increased 72% to $64.4 million from $37.5 million

- Effective tax rate of 20.8% vs. 31.8%

- Gross margin from home sales up 140 basis points to 17.7% from 16.3%

- $11.1 million impairment charge in 2018 third quarter vs. $4.5 million in 2017 third quarter

- Excluding impairments, gross margins increased 210 basis points to 19.2% from 17.1%

- Selling, general and administrative expenses as a percentage of home sale revenues improved by 90 basis points to 10.9% from 11.8%

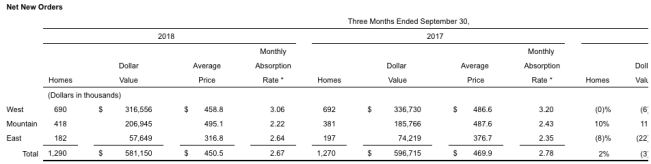

- Dollar value of net new orders of $581.2 million vs. $596.7 million in 2017 third quarter

- Unit net orders increased 2% to 1,290

- Monthly sales absorption pace of 2.67

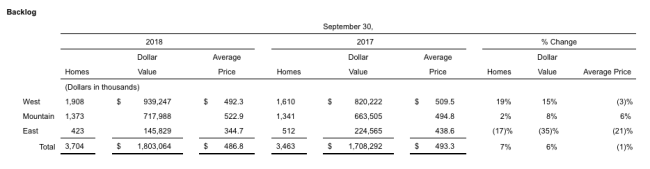

- Backlog dollar value at September 30, 2018 up 6% year-over-year to $1.80 billion

- Gross margin from home sales in backlog at 9/30/2018 roughly even with 2018 third quarter closing gross margin (excluding impairments) of 19.2%

- Lot purchase approvals increased by 16% to 2,878 lots in 34 communities

Larry A. Mizel, MDC’s chairman and CEO, stated, “We continued to see solid demand for our homes, as evidenced by our order pace of 2.7 homes per community per month, which was similar to the same quarter a year ago. After steady home price appreciation during the past few years and recent interest rate increases, national new home sales have slowed during the third quarter, relative to the robust increases seen during the past few years. This is an expected part of a housing cycle. However, we believe that our industry still has the potential for continued expansion, given the strength of the underlying fundamentals.”

Mr. Mizel continued, “Our affordable product communities have delivered above average order paces and gross margins over the last several quarters, and we believe that this trend will continue. With our mix shift to more affordable product and our expectation for 10% growth in active community count at the end of 2018, we feel that we are in a great position to take market share and grow our operations.”

The company issued the following guidance for the full year.

- Backlog conversion ratio (home deliveries divided by beginning backlog) for the fourth quarter estimated to be in the 45% to 47% range

- Active subdivision count at 9/30/2018 of 158, up 3% year-over-year and 5% from 12/31/2017

- Targeting a 10% year-over-year increase in active subdivision count by year end (from 151 at 12/31/2017 to at least 166 at 12/31/2018)

- Lots controlled of 25,011 at 9/30/2018, up 32% year-over-year

- Quarterly dividend of $0.30 ($1.20 annualized) declared in October 2018, up 30% year-over-year (after adjusting for 8% stock dividend in December 2017)

- Estimated effective tax rate for the fourth quarter of 2018 between 17% and 19%