KB Home (NYSE: KBH) after market close Tuesday reported net income of $30.0 million and diluted earnings per share of $.31 for its first quarter ended February 28, 2019, compared to a net loss of $71.3 million, or $.82 per diluted share, which included a writedown of tax assets due to the Tax Cuts & Jobs Act, in the same period last year. The results beat analyst expectations for a gain of $0.25 per share.

Among the results, on a year-over-year basis:

- Total revenues decreased 7% to $811.5 million.

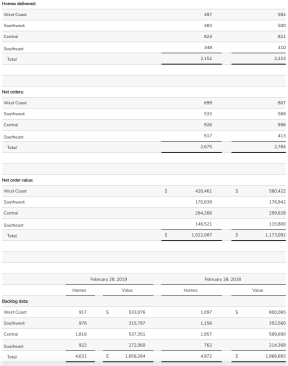

- Deliveries totaled 2,152 homes.

- Average selling price decreased 5% to $370,900, primarily due to a shift in the geographic mix of homes delivered and a lower average selling price in the company’s West Coast region.

- Home building operating income totaled $31.3 million, compared to $44.0 million. Home building operating income margin was 3.9%, down 120 basis points. Excluding inventory-related charges of $3.6 million in the quarter and $5.0 million in the year-earlier quarter, this metric was 4.3%, compared to 5.6%.

- Housing gross profit margin increased to 17.1%, compared to 16.1%.

- Housing gross profit margin excluding inventory-related charges improved 90 basis points to 17.6%. Adjusted housing gross profit margin, a metric that excludes inventory-related charges and the amortization of previously capitalized interest was 21.3%, compared to 21.4%.

- The increase in housing gross profit margin primarily reflected lower amortization of previously capitalized interest and a change in the company’s accounting for certain model complex costs, partly offset by other items.

- The company changed the classification and timing of recognition of certain model complex costs due to its adoption of Accounting Standards Codification Topic 606, “Revenue from Contracts with Customers” (“ASC 606”), effective December 1, 2018. The change in the classification of such costs was from construction and land costs to selling, general and administrative expenses.

- Selling, general and administrative expenses as a percentage of housing revenues were 13.4%, compared to a first quarter record-low ratio of 11.0% in 2018, mainly due to lower housing revenues, the above-mentioned impact of adopting ASC 606, and increased marketing expenses to support new community openings.

- Total pretax income was $34.5 million, compared to $46.0 million.

- The company’s income tax expense and effective tax rate were $4.5 million and approximately 13%, respectively, which reflected the favorable impacts of a $3.3 million reversal of a deferred tax asset valuation allowance and $2.0 million of excess tax benefits from stock-based compensation, partly offset by $.8 million of other items. Without these items, the company’s effective tax rate would have approximated 26%.

- In the 2018 first quarter, the company’s income tax expense of $117.3 million and effective tax rate of approximately 255% reflected the impact of a non-cash charge of $111.2 million due to the Tax Cuts and Jobs Act of 2017 (“TCJA”).

- Excluding this charge, the company’s 2018 first quarter adjusted income tax expense and adjusted effective tax rate were $6.1 million and approximately 13%, respectively. The adjusted income tax expense and adjusted effective tax rate reflected the favorable impacts of $4.0 million of federal energy tax credits the company earned from building energy efficient homes and $2.2 million of excess tax benefits from stock-based compensation. Without these credits and benefits, the company’s adjusted effective tax rate in the 2018 first quarter would have approximated 27%.

- Net orders decreased by 109, or 4%, to 2,675, with net order value declining $151.0 million, or 13%, to $1.02 billion. The decreases were primarily attributable to the company’s West Coast region.

- Company-wide, net orders per community averaged 3.7 per month, compared to 4.2 per month.

- The cancellation rate as a percentage of gross orders was flat at 20%.

- The number of homes in ending backlog totaled 4,631, compared to 4,972.

- Ending backlog value of $1.66 billion decreased 16%, reflecting fewer homes in backlog and the lower average selling price of those homes primarily due to a shift in geographic mix.

- Ending community count grew 13% to 248. Average community count increased 10% to 244.

- The improvement in the company’s ending and average community counts reflected increases in each of its four regions. Ending community count growth ranged from 4% in the company’s Central region to 26% in its Southeast region.

- The company had total liquidity of $978.5 million, including cash and cash equivalents of $511.7 million at quarter’s end.

- Cash and cash equivalents decreased by $62.7 million, primarily reflecting the company’s repayment of all $230.0 million in aggregate principal amount of 1.375% convertible senior notes upon their February 1, 2019 maturity and cash used by operating activities, partly offset by $400.0 million of net proceeds from concurrent public senior notes offerings completed in the quarter.

- Operating activities used net cash of $198.2 million, primarily for investments in inventories.

- There were no cash borrowings outstanding under the company’s unsecured revolving credit facility.

- Inventories increased by $100.9 million, or 3%, to $3.68 billion.

- Investments in land acquisition and development totaled $384.2 million for the 2019 first quarter, and lots owned or controlled increased to 54,744.

- Notes payable increased by $143.3 million to $2.20 billion, reflecting the company’s concurrent public offerings of $300.0 million in aggregate principal amount of 6.875% senior notes due 2027 and an additional $100.0 million in aggregate principal amount of the company’s existing series of 7.625% senior notes due 2023, partly offset by the above-mentioned repayment of convertible senior notes.

- Reflecting the increase in notes payable, the company’s ratio of debt to capital increased 120 basis points to 50.9%. The ratio of net debt to capital rose 270 basis points to 44.3%, but remained within the company’s 2019 target range of 35% to 45% under its Returns-Focused Growth Plan.

- On March 8, 2019, the company optionally redeemed the entire $400.0 million in aggregate principal amount of its 4.75% senior notes, which were scheduled to mature on May 15, 2019.

“We are beginning to see healthy growth in our average community count, which was up 10% in the first quarter,” said Jeffrey Mezger, chairman, president and CEO. “This increase, together with a substantial number of planned openings still to come, positions us to capitalize on demand during the spring selling season. Although the decline in net orders during the 2018 fourth quarter impacted our first-quarter housing revenues, we are encouraged by improving market conditions, which we believe should enable us to generate stronger revenues in the 2019 second half.”