KB Home, Los Angeles (NYSE:KBH) on Wednesday after market close reported net income of $68.1 million, or $.73 per diluted share, for its fiscal third quarter ended August 31. The gain compared to $87.5 million, or $.87 per diluted share, in the prior year quarter. Analysts were expecting a gain of $0.66 per share.

Among the results:

Three Months Ended August 31, 2019 (comparisons on a year-over-year basis)

- Revenues totaled $1.16 billion, compared to $1.23 billion.

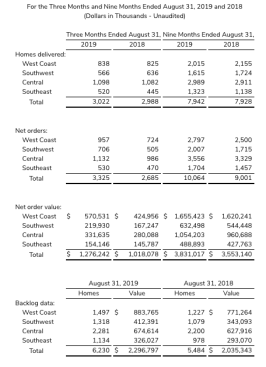

- Homes delivered increased slightly to 3,022.

- Average selling price of $381,400 decreased 7%, mainly due to a community mix shift within the company’s West Coast region.

- Home building operating income was $85.5 million, compared to $105.6 million. Home building operating income margin was 7.4%, down 120 basis points. Excluding inventory-related charges of $5.3 million in the quarter and $8.4 million in the year-earlier quarter, this metric was 7.8%, compared to 9.3%.

- Housing gross profit margin improved 50 basis points to 18.5%. Excluding inventory-related charges, housing gross profit margin increased to 18.9% from 18.7%.

- The improvement in the housing gross profit margin primarily reflected the favorable impacts of lower amortization of previously capitalized interest and the Company’s adoption of a new accounting standard (ASC 606) in fiscal year 2019, which were largely offset by certain West Coast region communities with relatively high average selling prices and margins having closed out in previous quarters, reduced operating leverage due to lower housing revenues and higher expenses supporting community count growth, and pricing pressure on net orders in the 2019 first quarter as a result of weaker market conditions during that period.

- Selling, general and administrative expenses as a percentage of housing revenues were 11.1%, compared to last year’s third quarter record-low ratio of 9.4%, mainly reflecting the Company’s adoption of ASC 606, increased marketing expenses to support new community openings, and reduced operating leverage due to lower housing revenues.

- As a result of its adoption of ASC 606, the company changed the classification and timing of recognition of certain model complex costs. In the quarter, these changes favorably impacted the company’s housing gross profit margin by approximately 70 basis points and negatively impacted its selling, general and administrative expense ratio by approximately 80 basis points.

- Housing gross profit margin improved 50 basis points to 18.5%. Excluding inventory-related charges, housing gross profit margin increased to 18.9% from 18.7%.

- The company’s financial services operations generated pretax income of $6.6 million, up from $5.1 million, mainly due to an increase in income from its mortgage banking joint venture, KBHS Home Loans, LLC (KBHS).

- KBHS originated 72% of the residential mortgage loans the Company’s homebuyers obtained to finance their home purchase, compared to 55%.

- Total pretax income was $91.9 million, compared to $114.7 million.

- The company’s income tax expense and effective tax rate were $23.8 million and approximately 26%, respectively, compared to $27.2 million and approximately 24%.

- Net orders for the quarter grew 24% to 3,325, with net order value increasing 25% to $1.28 billion.

- Both net orders and net order value rose in each of the company’s four regions.

- Company-wide, net orders per community averaged 4.3 per month, compared to 4.1 per month.

- The cancellation rate as a percentage of gross orders for the 2019 third quarter improved to 20% from 26%.

- The company’s ending backlog rose 14% to 6,230 homes. Ending backlog value grew to $2.30 billion, up 13% from $2.04 billion, with increases in all regions.

- Average community count for the quarter increased 18% to 255, while ending community count grew 13% to 254. The improvement in average community count reflected growth in each of the company’s four regions.

- The company had total liquidity of $610.8 million, including cash and cash equivalents of $183.8 million and available capacity under its unsecured revolving credit facility of $427.0 million, with $50.0 million of cash borrowings outstanding.

- The company used cash from earnings and certain other operating items of $237.4 million, together with cash on hand, primarily to fund an increase in inventories of $389.5 million and repay all $230.0 million in aggregate principal amount of its 1.375% convertible senior notes at their maturity. As a result, the company’s cash and cash equivalents decreased by $390.6 million.

- Inventories totaled $3.92 billion, up 9%.

- Investments in land acquisition and development totaled $1.22 billion for the nine months ended August 31, 2019, and lots owned or controlled increased to 56,379.

- Notes payable decreased by $200.1 million to $1.86 billion, primarily reflecting the above-mentioned repayment of convertible senior notes.

- The company’s debt to capital ratio of 45.1% improved 460 basis points from November 30, 2018 and 550 basis points from August 31, 2018. The company’s net debt to capital ratio was 42.6%.

- In July 2019, Moody’s Investor Service upgraded the company’s corporate credit rating to Ba3 from B1 and changed the rating outlook to stable from positive.

- Stockholders’ equity increased to $2.26 billion from $2.09 billion.

- Book value per share grew by $1.58 to $25.59.

“Our net order growth was driven by both significant community count expansion and a higher absorption rate, a key operational metric where we have long been an industry leader,” said Jeffrey Mezger, chairman, president and chief executive officer. “Notably, during the quarter, we achieved a community absorption pace of 4.3 net orders per month, surpassing last year’s robust performance, while at the same time increasing prices in about 90% of our communities.”

Mezger continued, “With year-over-year growth in both revenues and gross profit margin anticipated for our fourth quarter, we are on track for a strong finish to 2019, the third year of our Returns-Focused Growth Plan. As a result of the successful execution of this Plan, we have meaningfully increased our scale and profitability, and generated substantial operating cash flow that we have used to reinvest in our business and reduce our debt, two core components of our Plan. We expect to continue to grow our community count in 2020, and, together with our solid pace and $2.3 billion backlog, we believe we are well positioned for an excellent start to the new year.”