Adobe Stock/Gajus

Interest rates are rising. Due to growing concerns over a tight labor market, improved economic growth prospects, and rising inflation expectations, the Federal Reserve has raised the federal funds rate twice in 2018 thus far, with more hikes expected to come. This increase in short-term interest rates has modestly increased long-term rates. The average rate on a 30-year fixed rate mortgage stood at 4.5% as of the first week of July. NAHB expects rates to continue to rise into 2020, with the 30-year rate rising above 5%.

Rising interest rates are a concern in the housing sector. Higher rates increase the cost of builder and developer debt financing, as well as raise the cost of buying a home with a mortgage. However, with respect to housing affordability, it’s important to remember that the primary reason interest rates are higher is that the economy is performing well.

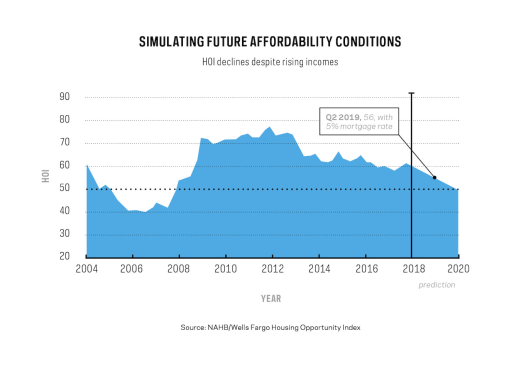

What impact will rising rates have on housing affordability given current trends? To find out, I used the quarterly NAHB/Wells Fargo Housing Opportunity Index (HOI), which calculates the percent of new and existing home sales that would be affordable under standard underwriting conditions given current interest rates for a family with typical household income.

Over the past decade and a half, the HOI peaked at 78 at the start of 2012. In other words, due to home price declines and reductions in interest rates, 78% of new and existing home sales during that time were affordable to a typical family. Due to recent gains in home prices and the current run up in interest rates, the index has fallen to 62 as of the start of 2018.

To simulate what will happen in the near-term, I used local price and income data in the HOI and projected those values according to recent trends. In markets where prices and incomes are rising, I used the current local rates of changes as forecast values. I also used the NAHB forecast for interest rates. The result is that, on net, housing affordability conditions will continue to trend lower, reaching a level of 50 near the end of 2020, a level last seen in 2007.

NAHB’s forecast model suggests single–family construction will continue to expand despite this change in conditions. The top reason for this expectation is the fact that there is such a large degree of underbuilding in single-family markets, with just over 900,000 single-family starts expected this year, compared with the 1.2 million we believe the market could absorb.

For policymakers and community leaders concerned about affordability declining due to macroeconomic conditions, there’s no better time to try to reduce regulatory costs associated with home construction. Ultimately, additional supply will help reduce the cost of the American dream.