It’s been more than five months since the Consumer Financial Protection Bureau’s TILA-RESPA Integrated Disclosure (TRID) went into effect with the main goal of simplifying the home closing process for consumers. The provisions, known as “Know Before You Owe,” stem from the Dodd-Frank Wall Street Reform and Consumer Protection Act that was signed into law in 2010.

TRID consolidated four existing disclosures into two forms: “A Loan Estimate that must be delivered or placed in the mail no later than the third business day after receiving the consumer’s application, and a Closing Disclosure that must be provided to the consumer at least three business days prior to consummation,” according to the CFPB.

Since there are a lot of moving parts when closing on a home and plenty of new information for industry professionals to learn, we spoke to Tawn Kelley, president of Taylor Morrison’s Home Funding and Mortgage Funding Direct Ventures, and Rod Alba, SVP and Sr. Counsel, Mortgage Markets Division, of the American Bankers Association, to hear their initial impressions on how the regulations are going thus far.

Kelley says she was prepared for a “tremendous undertaking” when the regulations were first announced. So far, she adds, her team has adjusted well, although the first couple weeks it felt like “we were moving in slow motion” when getting a loan closed.

“It did slow initially just to make sure things were done correctly, but we’re not seeing a significant slowdown,” she says. “Even in that first month, Taylor Morrison sold homes in October” and closed on them in the same month.

“It hasn’t been as cataclysmic as many would have wanted you to believe it was going to be,” she adds.

Alba was in favor of simplifying the process since disclosures can be confusing and have massive liabilities for lenders, but after the first few months he’s not certain that’s happening. “We’re not sure that it has actually improved the process visa vie the consumer, it certainly hasn’t improved the process for purposes of clarity in compliance and efficiency,” he says. “In that sense the final regulations have been disappointing.”

The missed opportunities, he adds, originate from the planning process. “[The CFPB] took all of RESPA, then they took all of TILA, they put one pack on top of the other pack and then they slapped a cover sheet on it and they called that simplification,” Alba says. “They actually managed to add a page to the voluminous disclosures we had before.”

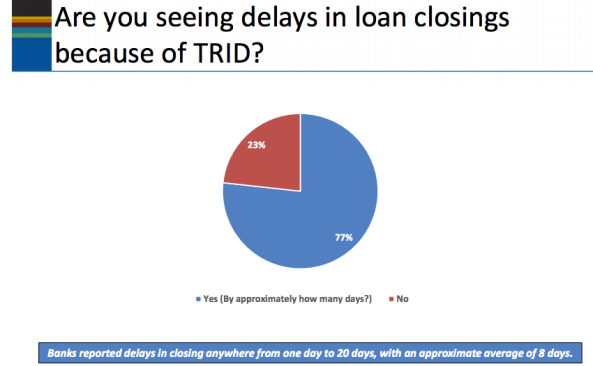

The ABA put out a survey earlier this month with 548 bankers participating. When asked if TRID has caused delays in loan closings, 77% of respondents said “yes.” “As we anticipated, our bankers are struggling to comply in part because the systems being provided by vendors are incomplete or inaccurate,” said Bob Davis, ABA executive vice president, mortgage markets, financial management and public policy, in a release. “The causes of many of these systems problems are ambiguities in the TRID rule that require resolution.”

The American Bankers Association surveyed 548 bankers about TRID. More than three-quarters said the new regulations delayed loan closings.

Two-third responded that they’ve increased their legal/regulatory costs, while 75% said they’ve eliminated products, including construction and home equity loans. “Construction lending has become extremely complex, so there are various products that don’t fit the mold,” Alba notes.

From a builder perspective, Kelley says, the biggest change is a heightened sense of processes and procedures. The new regulations can present a problem when unforeseen things occur, she adds, like bad weather, untimely inspections, or a buyer’s previous home not being able to close as scheduled.

But it’s not all bad, she says. “There are also opportunities that you can sell a home and be able to close on the transaction very quickly if the consumer, and the lender, and the builder are all able to coordinate…in a very short period of time,” she says.

On Wednesday, Ellie Mae, which provides loan software to the mortgage industry, released its latest Origination Insight Report. The highlight: Time to close all loans decreased to 46 days, the shortest time-to-close since May 2015 – five months before the new regulations went into effect.

“For the first time since October 2015, we’re seeing a substantial decrease in days to close from 50 days in January to 46 days in February,” said Jonathan Corr, president and CEO of Ellie Mae, in a release. “This could be due to lenders becoming more familiar with the new loan estimate and closing disclosure forms and business process around Know Before You Owe.”

Both Kelley and Alba say that as industry professionals become more accustomed to TRID, the process will get faster. “Once we get to know the regulations better, once the CFPB clarifies certain areas that are still extremely hazy, and once we can create new flows…I think we’ll be able to improve on the speed,” Alba says. “Whether it’s ever going to come back to where it used to be, I don’t know.”