This is the first installment of a three-part series on how the breakdown in lending standards has forestalled the home building industry’s economic recovery. The stories will focus on how we got to where we are today, how foreclosures and plummeting property values are affecting a new community in Indiana, and the analysts’ best guesses on when the downturn will end.

When 1,300 members of the NAHB made their annual trek to Capitol Hill on June 6, they checked their usual swagger—which came from representing what once was the country’s primary growth engine—at the door. That engine was sputtering and could seize up entirely if foreclosures kept mounting. So the builders’ laundry list of requests for lawmakers included a plea to allow the Federal Housing Administration (FHA) to help troubled borrowers refinance mortgages, many of which are nonconforming loans with escalating interest rates that have put owners behind the financial eight ball.

Builders aren’t just crying wolf, either. The Commerce Department said in March that the number of vacant, privately owned homes had reached its highest peak in the nation’s history. And through the first half of this year, there were, conservatively, at least 500,000 mortgage defaults, including notices of foreclosure, auction sales, or bank repossessions, according to various estimates. So the last thing that builders—already in the throes of a downturn that seems to get worse every month—need right now is a new flood of foreclosed homes cascading onto a market where finding willing buyers has become a snipe hunt.

It might be too late to dam that flood, however, at least in the short run.

Housing Predictor.com projected in early June that, based on its analysis of the largest 100 metropolitan real estate markets, more than 2 million homes would be foreclosed in the following 30 months. In June alone, foreclosure filings nationwide jumped to 164,664, nearly 87 percent over the same month a year ago, according to the tracking agency RealtyTrac. That number translates into one filing for every 704 households. “The housing boom was a house of cards,” observes Alexis McGee, president of Foreclosures.com, which reported a 78 percent increase in defaults and foreclosure notices through the first six months of 2007 versus the same period a year ago.

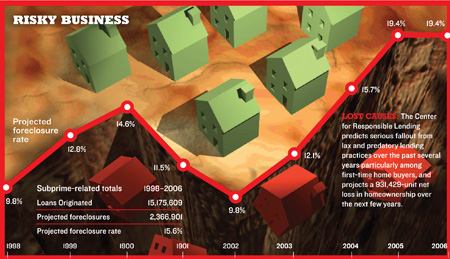

The Center for Responsible Lending, which for years has railed against “the death of common sense and the death of underwriting” in the mortgage lending industry, now warns that 2.4 million homes with subprime mortgages could foreclose by the end of 2008, according to its senior policy counsel Kathleen Keest. “Subprime loans made during 1998–2006 have led or will lead to a net loss of homeownership for almost 1 million families,” the Center reports (see “Risky Business,” below).

The damage is already spilling into the larger banking sectors: UBS shut down its hedge fund arm in May after it lost $124 million on subprime loans, and Bear Stearns had to pledge $3.2 billion—subsequently reduced to $1.6 billion when lenders accepted other collateral—in late June to facilitate the orderly liquidation of a hedge fund that was collapsing under the weight of bad subprime mortgage investments. To stem this impending foreclosure tidal wave, consumer groups and politicians are calling for everything from foreclosure moratoriums and intensified buyer education programs to massive refinancing assistance for families on the brink of losing their homes (see “Helping Hand,” page 112). The National Association of Realtors (NAR) this spring distributed a brochure to assist distressed homeowners, with a message that was both consoling and disturbing: “You’re not alone if you’re having trouble paying your mortgage.”

Some industry groups, such as the Mortgage Bankers Association (MBA), continued to insist through early summer that the foreclosure problem wasn’t expanding significantly into the prime mortgage sector. And even Housing Predictor.com notes that real estate markets this spring were appreciating in 18 states and stabilizing in 10 others.

But what’s no longer in dispute is that sizable numbers of home buyers and investors wound up with mortgages they either couldn’t afford or who predicated their ability to repay on the unrealistic expectation that home values would never stop appreciating. This has been especially evident among borrowers with checkered credit histories who were approved for subprime and alt-A loans—often with minimal or no up-front financial commitment required—which now account for one-quarter of all mortgages outstanding.

“We would expect the builders’ overall exposure to the subprime mortgage market to be greater than disclosed,” wrote Credit Suisse, which should know because it pumped capital into subprime lenders. The company predicted in March that 565,000 foreclosed homes would come back onto the market for sale within the following six months.

Learn more about markets featured in this article: San Diego, CA, Los Angeles, CA.