A generation ago, more than half of all homeowners in the U.S. owned their houses outright, with no mortgage payments. Today, that number is less than one-third, and falling.

The culprit has been the propensity of homeowners to refinance their mortgages multiple times, which extends the term of the loan and interest paid on it. And that interest is a killer, even without re-fi’s: For a 30-year, fixed-rate mortgage with 6 percent interest on a $250,000 loan, the owner ends up paying $539,598.47, of which $289,595.47 is interest that accounts for the bulk of the payments in the first 22 years of the loan.

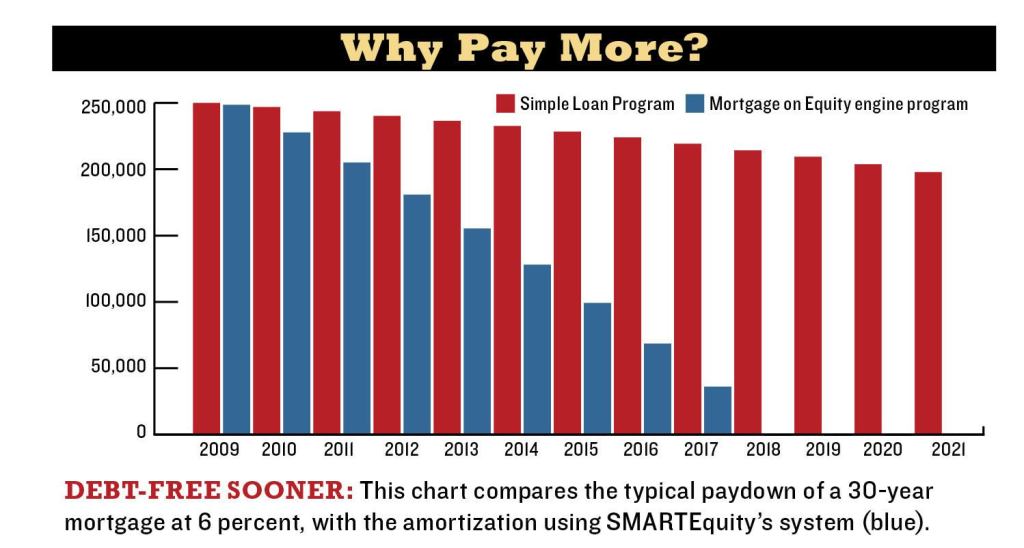

But if an owner were systematically paying down more of the principal in the early years the loan, the term and total amount of the payout could be reduced significantly. That’s the simplified premise behind SMARTEquity, a software program devised by Canadian company ComCorp Communications that is now being offered in the U.S. through a partnership with the Washington, D.C.–based National Organization of American Homeowners (NOAH).

“What we have to do is get people out of this re-fi mindset,” says John Walsh, NOAH’s founder and chairman. Walsh thinks the best way to get homeowners thinking about this is during the buying stage, and NOAH recently started pitching SMARTEquity to builders as a free incentive they could give to buyers, like a granite countertop. “If we could get 1,000 builders to offer this to 50 buyers each, by this time next year this program would be viral.” NOAH’s optimistic goal, he says, is to have 70 percent of all homeowners mortgage-free within 10 years.

Cash flow systems such as SMARTEquity have been popular in Australia and Great Britain for decades. ComCorp Communications, a real estate investment firm based in Ottawa, Ontario, developed SMARTEquity about five years ago, and more than 5,000 Canadian homeowners have used it, says its president and CEO Mark Montserin.

The key to the system is what’s known as a “sweep account.” Here’s how it works: Let’s say a homeowner borrows $250,000 to purchase a house with a 30-year, fixed-rate, 6 percent loan. He establishes a separate line of credit or savings account, from which he draws $2,500 per month and applies that amount to the mortgage principal. By doing so, the total mortgage loan is recalculated and the owner saves himself more than $12,000 in future interest payments. The owner uses the line of credit like a checking account into which he deposits his monthly income and pays bills. The owner is able to zero out this credit line in eight months and pays only $66.52 interest on it.

By repeating this process over the course of the mortgage, the owner would retire his house loan in 16 years and reduce the total interest paid by more than $100,000. The interest on the line of credit, on the other hand, would be under $1,700.

For builders, the “high perceived value” of SMARTEquity as a buyer incentive could lead to more referrals, says Montserin. And builders buying in bulk could lower the software’s $1,600-per-user cost to under $1,000, he says.

When asked why homeowners need the software, Montserin asserts “the short answer is: systems work.” To make his point, he notes that while most overweight people know they should eat less and exercise more, few do without following some kind of regimen. The same is true about mortgage reductions. Only 3 percent of people now actually pay down their principal, “and if you don’t have a system the chances for success are slim to none that you will.”

Learn more about markets featured in this article: Washington, DC.