Home equity loan debt outstanding and borrower utilization rates declined in 2018, and mortgage lenders anticipate mixed activity this year and only modest increases in originations in 2020. This is according to new research released today from the Mortgage Bankers Association’s (MBA) inaugural 2019 Home Equity Lending Study on lending and servicing of open-ended home equity lines of credit (HELOCs) and closed-end home equity loans (HE Loans).

“Many households are not tapping the equity in their homes, despite the significant rise in home equity since the Great Recession, wage growth, and low unemployment,” said Marina Walsh, MBA’s vice president of industry analysis. “Our study found that lenders do not anticipate a significant ramp-up in activity through 2020 because of various challenges, including other viable consumer financing alternatives, pricing pressures and competition, and rising costs. Furthermore, changing borrower sentiment and confusion over tax deductibility appear to have contributed to lackluster lending activity in recent years, as well as muted expectations going forward.”

Added Walsh, “Lenders expect HELOC annual originations to drop 3.8% in 2019, but grow 3.4% in 2020. Annual originations of HE Loans are forecasted to grow by 7.8% in 2019 and 8.4 % in 2020.”

Among the findings from MBA’s Home Equity Lending Report (covering data through December 31, 2018) include:

HELOCs

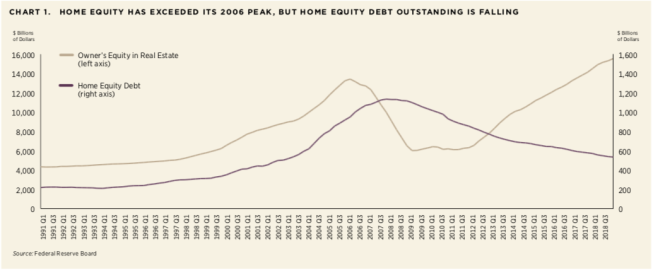

- The debt outstanding for HELOCs dropped 2% from beginning to end-of-year 2018, as borrower utilization rates declined.

- HELOC utilization rates (dollar volume of outstandings compared to maximum credit facility) decreased over the period 2016-2018, when examining the rates across origination vintage year cohorts for 2016, 2017 and 2018. For example, average utilization nine months after origination was 46% for 2016, 45% for 2017, and 43% for 2018.

- For all active accounts irrespective of origination year, the average HELOC utilization was 46% in 2018. The percentage of HELOC accounts with no outstanding balance as of year-end 2018 was 27%.

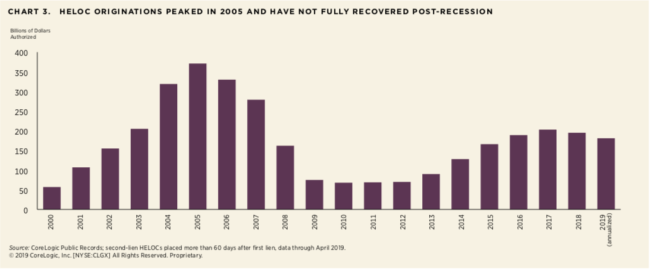

- In 2019, lenders of HELOCs expect annual originations to drop 3.8%, but grow 3.4% in 2020. HELOC debt outstanding on a year-over-year basis are expected to drop 2.9% this year and 2.1% in 2020.

HE Loans

- Home equity loan debt outstanding dropped 5% from the beginning to the end of 2018. As the average portfolio aged – 76% of accounts were over three years old in 2018 – newer, higher-balance originations were not fully replenishing payoffs and amortization.

- Nonetheless, lenders of home equity loans expect annual originations to grow by 7.8% in 2019 and 8.4% in 2020. Home equity loan debt outstanding is expected to increase 2.0% in 2019 and remain flat in 2020.

MBA’s study on Home Equity Lending for open-ended HELOCs and closed-end home equity loans was conducted in the Spring of 2019. MBA collected data from 27 member companies — including large banks, community banks, and independent mortgage companies — representing $64.7 billion in originations volume for 2018, $517.4 billion in maximum credit extended to borrowers as of December 31, 2018, and $249.7 billion in outstanding borrowings as of December 31, 2018.