For home builders–while a great deal of national attention focuses on macro data, like the release this week of housing starts and permits activity–what matters most is little numbers.

Single-family starts and permits in 2019 have to comp with a very strong start to 2018, which everyone knows ran out of steam in the back half of the year. Whether February’s starts and permits totals reflect bad winter weather, a level that will be revised upward as more data comes in, or a new normal is open to speculation. None of that really matters to builders.

Instead, little numbers–one permit pulled, one house started, one house sold, one more unit per month per selling community–are, as we speak, the all-important focus that will keep a builder in business this year or not.

Many builders, large and small, have reverted to a razor-thin-margin toolbox–using higher densities, lower square-footages, more standardized features and finishes, and every other value-engineering tactic known to push construction cycles, drive out costs, and try to reflect reduced expenses in lower asking prices–in hopes of sustaining, perhaps, stepping up their sales pace.

All of these tactics come to bear as builders work to meet demand at the lowest price tiers of housing’s cost spectrum–where resales and rentals have failed to meet a growing need among moderate-income households, and where demand has remained clear and strong.

So, it must come as a setback to get word–just as focus on the “little numbers” of entry-level home buyers, the one- or two-more units per community per month, or for smaller builders, that one home for every two months–that the Federal Housing Administration has tightened its loan standards for FHA-backed mortgages at what amounts to a moment-of-truth for builders.

Per Wall Street Journal staffer Ben Eisen:

The Federal Housing Administration told lenders this month it would begin flagging more loans as high risk. Those mortgages, many of which are extended to borrowers with low credit scores and high loan payments relative to their incomes, will now go through a more rigorous manual underwriting process, the FHA said.

FHA-backed borrowers are a critical buyer universe for home builders, especially those builders whose products and communities serve the needs of rising rent refugees, and would-be homeowners who can’t access decent options in an existing home marketplace that offers very little at the low end of the price continuum.

The FHA’s chief risk officer Keith Becker, the WSJ reports, estimates that as many as 40,000 or 50,000 potential borrowers–4% to 5% of FHA-insured mortgages–will be “affected” as the agency tightens lending standards via its Total Mortgage Scorecard to reduce exposure to failed loans.

HousingWire’s Jessica Guerin reports that the rules hit loans with case numbers assigned on or after March 18, ones that could stall or disqualify FHA financing for what’s already in lenders’–and builders’–pipeline.

That, in turn, could impact the little numbers that make all the difference to builders, large and small.

Now, we’re all in favor of FHA course-correction and vigilance when it comes to insuring that its portfolio of insured loans can perform as expected. The WSJ reports:

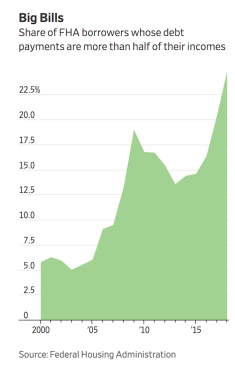

In the previous fiscal year, almost a quarter of FHA-insured mortgages were made to borrowers with a debt-to-income ratio above 50%, having risen sharply in recent years. The average credit score for borrowers fell to 670, the lowest level in a decade. In the FHA’s letter to lenders, it noted a rising concentration of loans with high debt-to-income ratios and low credit scores.

Still, the new Total Mortgage Scorecard algorithm will likely delay or disqualify some percentage of buyers and borrowers who fit higher-risk profiles and yet represent a solid, performing loan. That may not add up to a massive population of new-home buyers at the entry-level, but every little bit helps, or hurts.

Pace meaningfully impacts builders’ own standing and status with respect to their access to construction and operations finance, and their ability to weather shifts as they occur in the real estate cycle. Just as they began to see glimpses of hope that regulatory barriers and policy might further open the “credit box” to support finance for more working households, the FHA’s latest measures will effectively dampen such hopes.