The thing about deal-making is there are always at least two sides to the story. And in some cases, many, many more.

As 2017 unfolds into what could be a mergers and acquisition juggernaut for home building, with first-quarter deal dollar volume already approaching the cumulative total of all transactions in 2016, there’s a unique convergence of factors influencing the cycle this time around that has industry watchers split on where the trend will go from here. Some see the potential for more deals and sustained prices as things heat up, while others have an eye on higher mortgage rates that could lead to a tougher home selling environment, and thus, muted margins on companies’ bottom lines. Regardless of where it goes from here, few expect the recent activity to stop anytime soon.

“Just based on what we’ve seen so far this year, the deals we’re working on and potential deals we’re evaluating, 2017 will be a busy year,” says Tony McGill, managing director and head of investment banking at Zelman & Associates, a leading New York–based equity research and investment banking firm focused on home builders. Indeed, through mid March, there was already approximately $1.5 billion in home builder merger and acquisition activity, compared with around $2 billion for all of 2016. McGill points to healthier credit markets, generally optimistic sentiment toward housing, home builders’ stock prices finally going in the right direction, and corner office confidence as key catalysts. “There’s just more deal activity,” he says.

The buyers who are currently kicking U.S. home building’s tires are coming from near and far. “We did nine deals in 2005, and almost all of them were from within the U.S.,” says Tony Avila, CEO of San Francisco–based Builder Advisory Group, which brokers home builder M&A deals. “Now, I’ve got buyers from Japan, buyers from China, buyers from Europe, as well as non-home builders coming in. It’s just a much more diverse buyer group this time around.”

Deals, Deals, Deals

Some of the reasons driving the uptick in activity are based on perennial trends—the recovery started in some markets as early as 2010. Other factors have to do with specific, fundamental demographic and capital shifts—millennials are coming in the U.S., and capital is still relatively cheap—both here and abroad.

Just look at the raft of deals that have either been announced or closed in home building through March:

- Feb. 9 Sumitomo Forestry America, a subsidiary of Japan’s fourth–largest domestic builder, takes a 70%, $70 million stake in Salt Lake City–based Edge Homes.

- Feb. 10 Lennar closes its $643 million, all-cash deal to buy Florida-based WCI Communities, originally announced in September.

- Feb. 13 Daiwa House USA, a subsidiary of Japan’s Daiwa House Group, closes deal (first announced in October) to buy 82% of Washington, D.C.–based Stanley Martin Communities for $251 million.

- Feb. 21 California-based CalAtlantic Group and Columbus, Ohio–based M/I Homes buy Minnesota assets from Mattamy Homes, which operates in the U.S. and Canada.

- Feb. 22 Japan’s Sekisui House buys Salt Lake City–based Woodside Homes for $468 million.

- Feb. 24 China’s Puyin Blockchain Group makes $655 million investment in Serene Country Homes to build in Dallas-Fort Worth’s Sendera Ranch Community.

- March 3 Scottsdale, Ariz.–based AV Homes buys Savvy Homes of Raleigh, N.C., for $50 million.

- March 7 Sekisui House acquires 4,000-acre portion of the Nexton Community in Summerville, S.C., from WestRock Land and Development.

While these deals range from big U.S. publics buying smaller domestic players (Lennar-WCI); foreign buyers from Asia coming in to deepen their footprint on American shores (Sekisui, Sumitomo, Daiwa, and Puyin); and even a growth-obsessed top 25 builder buying a smaller upstart (AV-Savvy), all of them have a common axis. Namely, buyers are allocating capital to the markets where they feel they have the best growth prospects relative to their own investment objectives.

Sellers are taking profits for the same reason. They’re either leaving markets where they feel the best days are behind them (Mattamy-CalAtlantic-M/I), or they’re staying and deciding to use other people’s money in place of their own to keep forging ahead (Daiwa-Stanley Martin and Sekisui-Woodside).

Whatever side of the deal fence you’re on, in 2017, the one maxim that applies to everyone is that it’s all relative. And whether you consider this a bumper market for buying home builders—as many do in the usual suspect markets of the Smile Sunbelt—or an exquisite exit opportunity to take hard-fought profits off the table late in the cycle, it depends on the dirt under your feet: literally, where you stand.

For Alex Kamunya, managing partner at Boston-based private investor KAM Home Buyers, recent activity in the U.S. market is sure to beget more. With Lennar buying WCI, and D.R. Horton announcing its September 2016 acquisition of Wilson Parker, following a standard “growth through acquisition” formula, he sees motivation for other large domestics publics like PulteGroup and NVR to make deals just to keep up.

“I expect them to be looking for third-tier companies as potential targets, and smaller home builders who have capital issues or haven’t fully rebuilt their balance sheets since the crisis,” Kamunya says.

A View From Afar

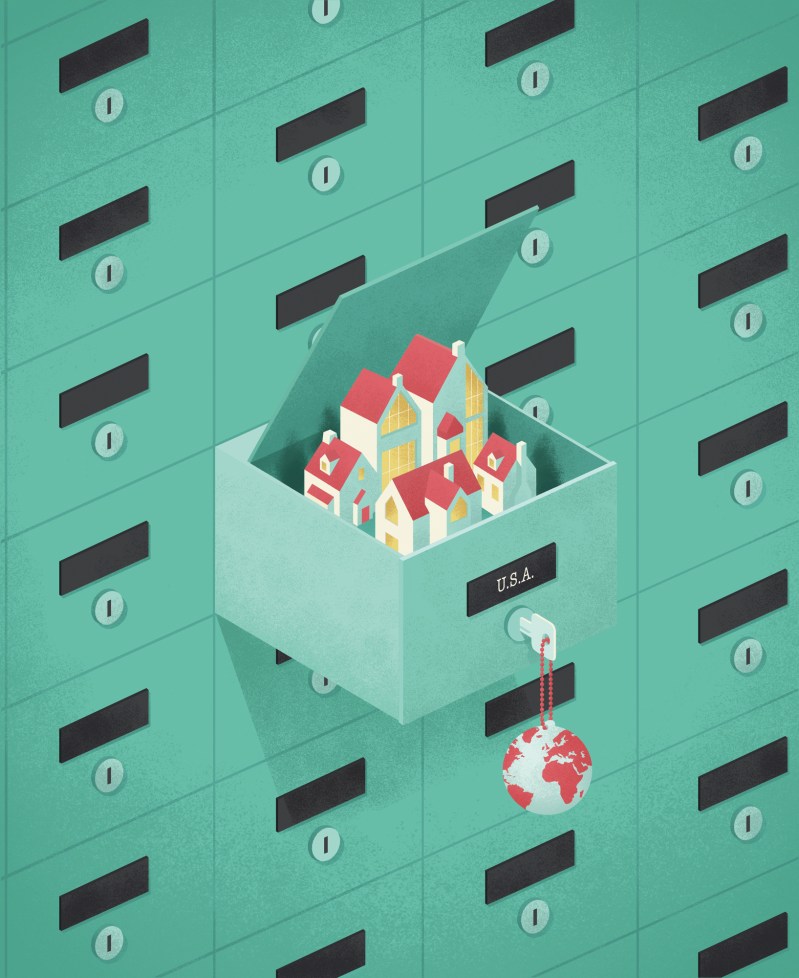

Hands down, the trend within the trend this year has been the home builders from Asia, like Japan’s Sumitomo, Seikisui House, and Daiwa, and China’s Puyin Group, taking down firms and lots in the U.S. For those buyers, how things look in the U.S. right now must be seen through the lens of where things are in their respective countries.

Demographic and GDP growth in Japan has been anemic for decades, with its census tracking an actual population decline for the first time in 2015 of 1 million people—not a trend that’s a friend to home builders. So, too, for China. After 30 years of enforcing its One Child policy, which ended in 2015, its demographics are skewing older, with no bumper crop of millennials to create new demand, as in the United States. This comes at the exact moment many urban areas in China have been overbuilt, and whispers of a bubble on the scale of what happened in the U.S. in 2007 are in the wind.

“The emergence of Asian buyers looking at the U.S. right now has as much to do with where they’re coming from as it does with where they’re going,” says Ron Robichaud, managing partner of Boston-based home builder M&A consultancy Robichaud Financial Services. “The U.S. has always been the world’s safe haven.”

And more are sure to come. For Michael P. Kahn, managing partner at Palm Coast, Fla.–based Michael P. Kahn & Associates, which has arranged more than $6 billion in home builder M&A deals since 1988, Chinese buyers are beginning to emerge in ways that match their Japanese counterparts.

“We’re representing two of the top 10 home builders in China and Hong Kong right now, and we’ve talked to a third group that’s already setting themselves up in the United States,” says Kahn, who in March was working on three M&A deals spanning Huntsville, Ala., Pittsburgh, and Raleigh.

Lower Cost of Capital, Longer Time Frames

Given the lower cost of capital those Japanese and Chinese buyers enjoy, they could make stiff competition for U.S. public home builders looking to grow through acquisition in 2017, too. As Barclays home builder analyst Michael Dahl has noted, Daiwa House and Sumitomo bonds trade at yields 200 to 500 basis points lower than their U.S. counterparts.

“Domestic home builders just have a higher cost of capital,” says Builder Advisory Group’s Avila. “That’s going to be a challenge, and make it harder for them to compete with foreign buyers. But they’ll also still be able to get deals done because a lot of them will be relationship-based.”

Andrea DeSantis

Asian buyers are also approaching the market from a different perspective, and with different expectations that could make them attractive to a certain breed of small public or private U.S. home builders who want to sell now. Namely, these companies like to start out with a majority investment—such as the Sumitomo-Edge and Daiwa-Stanley Martin deals—rather than come in for an all-out acquisition. Under those structures, they like to keep current management teams in place, but those teams shouldn’t be beholden to the same pressures from Wall Street analysts as major U.S. publics.

“When you talk to a Chinese or a Japanese buyer and you ask them what their five-year plan is, they ask if you’d like to hear their 40-year plan,” says Kahn. “Their thinking is very different compared to ours. They’re not so consumed with having to present substantial profits within the next three years. They’re much more interested in the long term.”

That means builders like Steven Alloy at Stanley Martin will likely stay on, with a significant cash infusion, while being able to put less of their own cash at risk. That’s a departure from the typical domestic buying model, where the big U.S. publics go after established privates largely to get their land and lots or to establish a market position in a given metro, and “accrete” the executives who started the company.

Working For the Man

But while that may be attractive to some builders in the prime of their careers looking for a cash infusion to expand, it also can be tricky to pull off.

“When the publics do an acquisition, nine times out of 10, the guy who’s selling is supposed to stay on for two or three years,” says Daniel B. Green, principal at Greenwich, Conn.–based private equity group Wheelock Street Capital. “Most of them don’t last more than 12 months.”

The reason why has to do with the type of people home building attracts.

“You’ve got to remember, home builders are the consummate entrepreneurs,” says Robichaud. “They literally built it from the ground up. It’s not in their DNA to be working for a large company where all the sudden somebody is calling you from corporate.”

But for Asian buyers, keeping those executives in place will be critical to achieving success in their new markets. “They want the sellers to have some skin in the game,” Kahn says. “Making sure management stays in place and creating a succession team is very important to them. Because they have expertise building homes. They just don’t have it in the United States.”

At the same time, Asian buyers will need what every U.S. home builder needs when it buys into a new market. “In addition to home building expertise in the United States, they need home building expertise in that specific market,” says Robichaud. “When you look at it big picture, all the large public home builders do is allocate capital to their subsidiaries. It’s the local talent that makes it happen.”

The View From Over Here

But while positive demographics, continued healthy demand, and an annual shortage of nearly 200,000 units a year make U.S. home building an attractive target for the right acquirers right now, some sellers are lacing up the other shoe.

“For us, it’s harder to make the numbers work,” says Green, the private equity investor at Wheelock Street Capital. “This late in the cycle, with prices going for what they are now, we don’t see it as much of a buying opportunity. Our strategy would be more to prune and sell.”

That’s a huge contrast to the positives bullish buyers see in this market, but you’ve also got to consider where folks of Green’s ilk are coming from. Namely, after housing crashed in 2007, leading to the Great Recession, many private equity investors were able to swoop in and buy home building interests for pennies on the dollar. But given the investment objectives of these types of funds, which often use a five- to seven-year time horizon for their investments, now is the time to exit.

Green, who’s been on the selling side of deals in Atlanta, Dallas, and Colorado for the past two years while still making purchases in other areas and asset classes, says he’s been balancing his portfolio to match the point in the cycle as he sees it.

“We don’t really get into the nuances of each market, as much as we look at the macroeconomic drivers,” Green says. “So instead of being market driven, it’s really more of a portfolio management strategy for us.”

As the Wheel Turns

Still, while that’s a prudent and logical caveat, the smart money tends to pay attention to what the people who were early to market say when they look in the rearview mirror. And right now, the private equity funds that jumped into home building’s debacle just as the dark days dawned are heading for the exits.

“Private equity has figured out that if you go beyond five years in home building, you get great total return, but your internal rate of return starts to take a hit,” says Kahn. “They also usually make promises to their investors in terms of a time horizon, and they have to live within those boundaries. So if they promise to get their money back in seven years, they might have to start getting out by year four or five—which for many of them is right now.”

Rate Watch

Other factors are playing into sellers’ decisions now, too. A rising interest rate environment—unseen in the U.S. for almost a decade—will likely put pressure on home builders in a way that isn’t reflected in the rosy outlook on the buy side of the equation.

“Rate increases hurt the long-term growth prospects of the industry,” says Michael Beaver, director at financial and operational consulting firm Conway MacKenzie. “You’re definitely seeing that the home builder market has rebounded and could be starting to mature.”

That could put pressure on the bottom line, too.

“I think that as interest rates go up, on the profit and loss side of the business, builders are going to struggle with the financing to qualify their buyers,” Green says. “I think that’s more of a concern than the cost of capital in these transactions. Because eventually, if they have to lower their prices due to the fact that people can’t afford their product anymore, that’s going to compress their margins.”

That may be why the deals that have happened, such as Sekisui-Woodside, which priced at approximately 1.2 times book value, have been coming in at amounts that are a little more compressed than they may have been just a short time ago. Lennar struck its deal with WCI in late 2016 for about 1.3 times book—even with the raft of buyer activity.

“I think what you’re going to find is a lot of entrepreneurs’ expectations were higher two years ago, when they heard about all these trades going at 1.7 and 1.8,” Green says. “Now, the buyers are saying they can’t do that, because it’s too dilutive and their land is too expensive. So sellers will need to adjust their expectations to where you still might get 1.7 on the high side, but the low end of the spectrum will be closer to 1.1. Even then, buyers will need to find the special sauce in each deal to make it work.”

He adds that the projections for current deals have been penciling out in more muted terms. “That big escalator that you put on every deal a couple years ago? You may need to trim that down, or keep it flat and see what it looks like,” Green says.

Some observers, such as Avila, see interest rates as less of an impediment than conventional wisdom would suggest, largely due to the flattening of the yield curve between long- and short-term bonds. “With a relatively flat yield curve, mortgage rates at the end of the year may not necessarily be much different than where they are today,” Avila says.

But from Robichaud’s perspective, rates could be the X factor that hasn’t gotten its proper due to this point in the cycle.

“There are some guys out there who still remember double-digit mortgages,” Robichaud says. “But there’s also an entire generation of home builders right now who have never operated in a volatile interest rate environment. Just think about what an 8% mortgage rate would do to the industry right now.”

For that reason, Robichaud looks at the current M&A climate with reserved optimism.

“I’ve been through a lot of cycles, and this one’s playing out very nicely,” he says. “We’re very excited about the foreign buyers coming in, but we’ve been through this before. People forget this is a cyclical industry, and for some strange reason, they all start drinking the same Kool-Aid. Their pens get a lot more ink in them, and they start writing bigger checks than they can justify.”

With 2017 just a quarter over, more checks certainly are being written, though so far, the numbers on them still seem prudent. How big they’ll get before the ink runs out—and few think that will happen anytime soon—is still anybody’s guess.