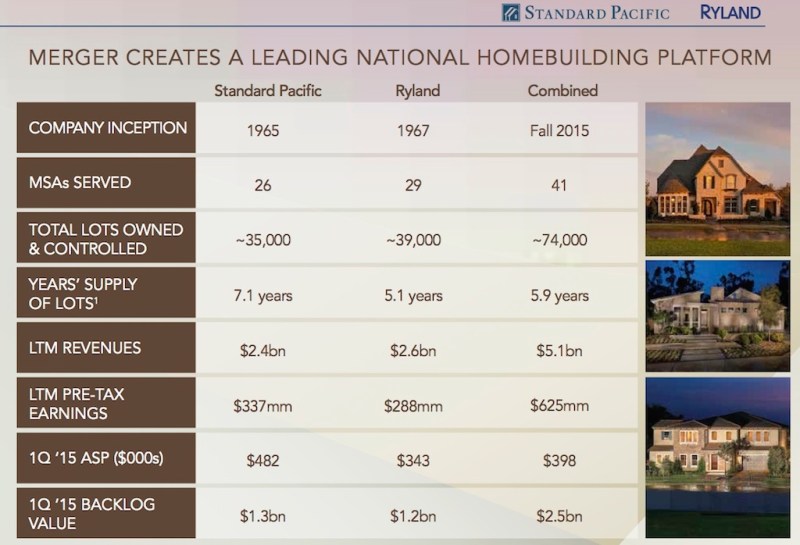

This week’s historic Ryland-Standard Pacific merger created the fourth largest home builder in the industry, with a market cap of roughly $5.2 billion and a footprint that reaches roughly 17 states and 41 MSAs.

And, analysts see a lot of potential in the new, supersized entity.

Raymond James sees a number of benefits to the deal, including facilitating accelerated growth through broader diversification, strengthening of balance sheets (i.e., potential credit rating upgrades), and potential synergies, including operational economies of scale and capital markets opportunities afforded to a larger market capitalization.

“One of the longer-term benefits from the deal will be the increase in the market cap of the combined company above the $5 billion threshold,” Horne wrote. “We note the larger-cap home builders with market caps over $5 billion currently trade at 15%-20% multiple premiums (on projected 2016 earnings) to the smaller-cap homebuilders.”

As with any merger, efficiencies will also drive savings. J.P. Morgan’s Michael Rehaut wrote that the deal will offer $50-$70 million of synergies, including $10 million to $20 million from a reduction in cost of sales, with the balance expected from overhead reduction. About half of those savings, $30 million to $35 million, will be enjoyed by the end of 2015, with the full run rate of synergies to be achieved in 12 to 15 months.

Upfront costs—like $100 million to $150 million of purchase accounting “mark ups” to Ryland’s existing backlog; $50 million to 55 million of transaction costs; and $25 million to $30 million of integration costs—mean there probably won’t be any material earnings accretion until late 2016 or 2017, according to Raymond James.

Maklari feels good about the future prospects for the new entity.

“The conservative nature of both these management teams leaves us feeling comfortable about their continued focus on profitability and driving long term shareholder value,” UBS’s Maklari wrote. “We’d note that Ryland has completed numerous smaller acquisitions as the recovery has taken hold, giving it experience in successfully integrating the operations of two entities.”

While the merger foreshadows more M&A in coming months, [UBS] remains skeptical. Management stated it wants to be “a leader rather than a follower” in the event an industry consolidation wave is at hand – but we are not convinced that a series of M&A dominoes is about to fall,” he wrote

But as BUILDER’s John McManus noted earlier this week, other analysts expect some more M&A coming.