The rate of job growth will determine the pace of recovery for a housing market whose prosperity could also depend on how it provides more affordable and sustainable options to the diverse buyer segments likely to drive the industry in the next decade.

That is the familiar refrain that the Joint Center for Housing Studies of Harvard University reiterated on Monday morning at the Ford Foundation in New York City, where it presented “The State of the Nation’s Housing 2010,” its annual analysis of where America’s built environment was, is, and might be headed.

Despite another dismal year in terms of housing production, sales, and financing, the Joint Center continues to see hope in Census Bureau projections for 1.25 million household formations per year, on average, through 2020. That number, the Joint Center asserts, would support average annual housing completions and manufactured home placements of between 1.7 million and 1.9 million units.

The inevitable “but” is the uncertainty about what kinds of housing these future buyers will want or need, as the nation emerges from a traumatic recession that has seen unemployment soar, incomes stagnate, and personal wealth (mostly in the form of home values) plunge. Consequently, “affordability is the most critical challenge facing housing today,” said Nicolas Retsinas, who is stepping down as the Joint Center’s director after 12 years at the helm.

The country is still groggy from a recession during which 8.4 million jobs were lost, 1.2 million of them in residential construction. Some 16 million Americans are now out of work. Between 2007 and 2009, the number of multiple-income households fell by 2.7 million and the number of households with no earners over this same period increased by 2.2 million, or by 20%.

“This is a fragile recovery,” says Eric Belsky, who last week was named to replace Retsinas as the Joint Center’s director. “And the job market is the key here.”

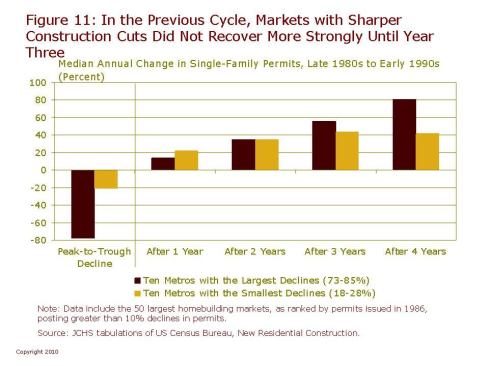

The housing industry is now trying to regain its footing after downsizing to what Belsky called “shellshock” levels. Last year was the first time on record that building permits fell below 900,000, and the first time since 1959 that single-family housing starts dropped below 500,000. Multifamily starts declined to their lowest level on record, existing home prices fell for only the second time in 40 years, and the overall vacancy rate hit a new high, in spite of severe production cuts.

Thank God for first-time buyers, who last year accounted for 36% of all purchases. These buyers enjoyed some affordability gains, as mortgage payments on a median-priced home fell below 20% of the U.S. median household income, the lowest ratio since 1971. The federal tax credit for first-time buyers also stimulated demand among these customers. But Belsky cited the irony that despite the surge in first-time buyers, overall household growth continued to slow. (By how much it’s hard to say, as estimates for the period 2005 to 2009 range from 1 million to 2.8 million.)

“Right now, we’re on a slippery slope,” observed F. Gary Garczynski, chairman of the National Housing Endowment, who was one of three guest speakers the Joint Center invited to comment about its report. Garczynski joked about using a magic eight ball to predict the future and having it read “Ask Again Later,” which is fitting for an industry with many unanswered questions regarding its recovery. How sturdy will housing be, post stimulus? Could economic troubles in Greece or Spain impact America’s housing, especially its access to capital markets for financing? Where will new buyers come from? “Low interest rates don’t mean a thing if you can’t qualify” for a loan, stated Garczynski.

Concerns about financing and affordability pervade the Joint Center’s report at a time when the number of households that spent more than half of their incomes on housing jumped by one-third to 18.6 million in 2008, the latest year for which data are available. Forty million households were spending more than 30% of their incomes on housing, which as the prices of housing plummeted.

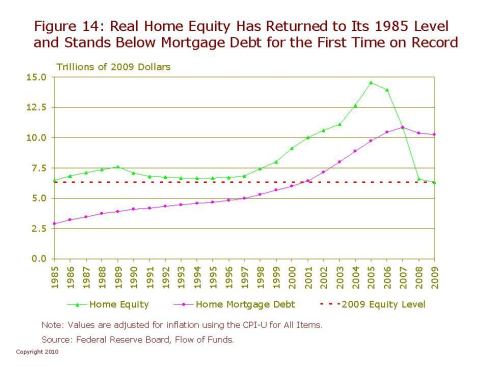

The problem is that incomes aren’t keeping up with either rental or for-sale prices. Incomes in the United States have been stuck in neutral for years, and the recent recession has only exacerbated this trend. Wealth from homeownership, which once served as owners’ nest egg and piggy bank, has dwindled. Real wealth per household slid to $486,600, from $503,500, over the past 10 years, and real home equity, at $6 trillion, hasn’t been this low in 25 years. Meanwhile, household mortgage debt exploded to $10 trillion. (The dollar amounts for equity and debt are essentially reversed from what they were in 2000.)

At the end of last year, 11.2 million households were underwater, in that their mortgages were higher than the current value of the homes themselves. It’s hardly surprising, then, that short sales and foreclosures accounted for one-third of all existing home sales last year.

And this “overhang” simply got worst in a new year. By the first quarter of 2010, there were 2.1 million loans that had lapsed into the foreclosure process. The Mortgage Bankers Association (MBA) estimated that “seriously delinquent” loans for single-family homes (i.e., those more than 90 days in arrears) ranged from 5.1% of prime-rate fixed-rate mortgages to a whopping 42.5% of subprime adjustable-rate mortgages.

The inevitable consequence of this bad-loan environment has been the virtual disappearance of private capital from a secondary mortgage market that is now being propped up primarily by the Federal Housing Administration (FHA). John Courson, MBA’s president and CEO, said that expectations about the effectiveness of federal government’s Home Affordable Modification Program, or HAMP, to modify troubled mortgages “haven’t matched up with reality.” MBA is seeing some evidence of private-sector loan modifications, as well as a drive by lenders “to work with unemployed owners on forbearance,” he said. Courson also noted that “a big factor” in the financial regulatory reform that Congress is now considering could be the issue of risk retention. “The Senate bill recognizes that there are certain lending instruments [such as 30-year fixed-rate mortgages] that didn’t cause this mess” and therefore should not be subjected to new risk retention requirements.

Courson insisted that this recognition would be crucial for the long-term health of mortgage financing because right now, he stated, “the credit box is tight, and it’s going to get tighter. We can’t do anything until we return liquidity to the market.” As a side note, Courson thought that homeowners who are considering to “strategically default” on their underwater mortgages will eventually realize how that decision will hamper their ability to get back into the housing market.

How the regulatory winds blow is going to have a big impact on how many new buyers come into the housing market in the coming years. As it has stated previously, the Joint Center is resting many of its assumptions about the growth of the housing market on projections for minority and immigrant household formation. Those two demographic groups accounted for nearly three-quarters of net household growth between 2003 and 2009. Minorities made up 35% of all first-time buyers and 20% of repeat buyers in 2007, the latest year for these data, while immigrants accounted for 19% and 12%, respectively.

Minorities are the majority in an increasing number of cities, too. “We’re going to have to rethink who ‘the other’ is in this country,” said Belsky. But relying too heavily on these buyers is risky because their income levels are generally lower than white households, which means that a sizable number of minorities and immigrants are going to be renters before they are owners.

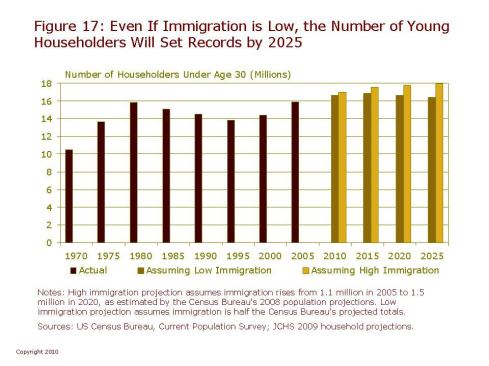

The Joint Center is also banking on significant household growth among the Echo Boom generation, aged 25 to 34, who are now about 81 million strong and could expand to 93 million by 2025. The big question about this generation, though, is just now fervently it is buying into homeownership as being central to their lifestyles. Other research on this group has found it to be conscious about energy efficiency, and more desirous of living closer to work. But echo boomers starting out in the work force at a time when earnings and benefits are being shaved, so their buying power could be limited for a while.

Given the diversity and probable income levels of these buyers and what their housing requirements might be, a dramatic reconsideration of the built environment is in order, said Doug Bibby, president of the National Multi Housing Council. “Our housing policy is badly in need of modernization,” he said. To provide a more balanced mix of housing for the next generation of buyers, he would like to see more compact development, as well as redevelopment and rehabilitation of existing homes, coupled with a rewriting of “hopelessly outdated” zoning and land-use regulations.

At the very least, said Bibby, any policy must appreciate “that there are too few affordable housing units.”

John Caulfield is senior editor for BUILDER magazine.

Learn more about markets featured in this article: New York, NY.