Together, housing data and Animal Spirits tell stories.

Data tracks actual trends in say, construction starts, permits, orders, closings, prices. Animal Spirits are phenomena behavioral economists talk about to explain those trends.

One of the originators of the notion of Animal Spirits as an answer to why housing data works as it does is Nobel Prize winning Yale economist Robert Shiller. Thing is, although Dr. Shiller might well explain past housing data and trends by using the term Animal Spirits, he rarely, if ever would apply the phenomenon of Animal Spirits to what has not happened yet.

For instance, this week’s batch of housing data included a big jump up–mostly due to strong activity in the western states–in new home sales for the month of April. Here, National Association of Home Builders economist Michael Neal gives the top line reading from the report:

According to the U.S. Census Bureau and the U.S. Department of Housing and Urban Development, sales of new homes rose by 4.0 percent over the month of March to reach a seasonally adjusted annual rate of 694,000. Year-to-date, covering the first quarter of 2018, the total number of new homes sold is 10.3 percent ahead of its pace over the first three quarters of 2017. The increase in new home sales over the month also reflects a 7.9 percent upward revision in sales over February from an initial estimate of 618,000, illustrating the volatility in the data and subsequent revisions.

So, that’s the data.

Are Animal Spirits–a collective unconscious of people motivated in unison to put down deposits on new houses–playing a role in the upward spike in sales for April?

Explanations for a sudden increase–a big change–stray into an area of speculation where you would not likely see Dr. Shiller venture.

Is the dramatic upward turn–statistical volatility and all–the result of a “pull forward” of demand thanks to a collective psychological fear that interest rates are going to only go higher and that now is the time to buy?

That’s where this analysis, from Wall Street Journal staffer Lev Borodovsky, heads, piecing together actual housing and mortgage application data into a logical pattern that supports his conjecture:

Are homebuyers rushing to get ahead of the rising mortgage rates (chart below)? That would suggest that house purchases are being pulled forward and a housing market slowdown will follow.

Rising rates–and the risk to prospective buyers that interest rate increases will outstrip their monthly payment buying power–may act as a “pull forward” catalyst.

At the same time, a longstanding pattern of constructive job formation, and the demographics–mostly, the delayed movement of young adult millennials into household and family formations–might explain the surge in strength, together with the fact that more new homes are now being offered in the entry-level price points of the market.

Here, new NAHB research from one of the economics team members, Rose Quint, seems to support this idea:

Millennials were the likeliest generation to have plans to buy a home in the next 12 months (19%) while Seniors were the least likely (13%). For a large majority (72%) of Millennials planning a home purchase, this is their first attempt at becoming home owners.

Whether we look at the data and conclude that buyers are being “pulled forward,” or whether they’re actually releasing “pent up” demand is speculation at the moment. Only hindsight can give us insight into how Animal Spirits act on the housing economy.

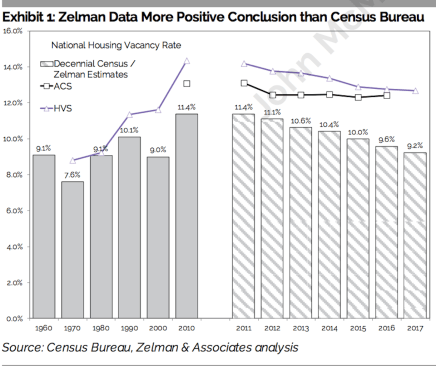

For a solid data analysis on actual demand, the latest issue of The Z Report, from Zelman & Associates, looks at a seldom-acknowledged metric–national occupancy rates–as a telltale indicator of actual demand. For a free trial of The Z Report, click here.

The conclusion of the analysis, and its interpretation by the Zelman team, is this:

According to our analysis, the national vacancy rate ended 2017 at 9.2%, nearly matching the decade end points from 1960 through 2000, which we interpret as a more normal level. In other words, excess housing caused by overbuilding before the recession and weak employment during the recession has been completely absorbed. (See exhibit).

This should mean that new construction supply has returned to mid-cycle levels, essentially matching household formation plus stock lost for demolitions or obsolescence. Unfortunately, that is not the case because supply bottlenecks around labor capacity and land have governed the pace of new construction. More specifically, in 2018, we estimate new residential supply will total roughly 1.25 million, but we believe sustainable demand is closer to 1.55 million.”

That’s demand that data support. No Animal Spirits need to be added to explain a constructive case for continued recovery.