National Association of Home Builders (NAHB) Chief Economist Robert Dietz, Associated Builders and Contractors (ABC) Chief Economist Anirban Basu, and American Institute of Architects (AIA) Chief Economist Kermit Baker delivered a collaborative midyear economic forecast Monday afternoon. The trio provided expert analysis of present and backward-looking economic indicators, and discussed their individual expectations of residential and commercial market performance for the coming year and beyond.

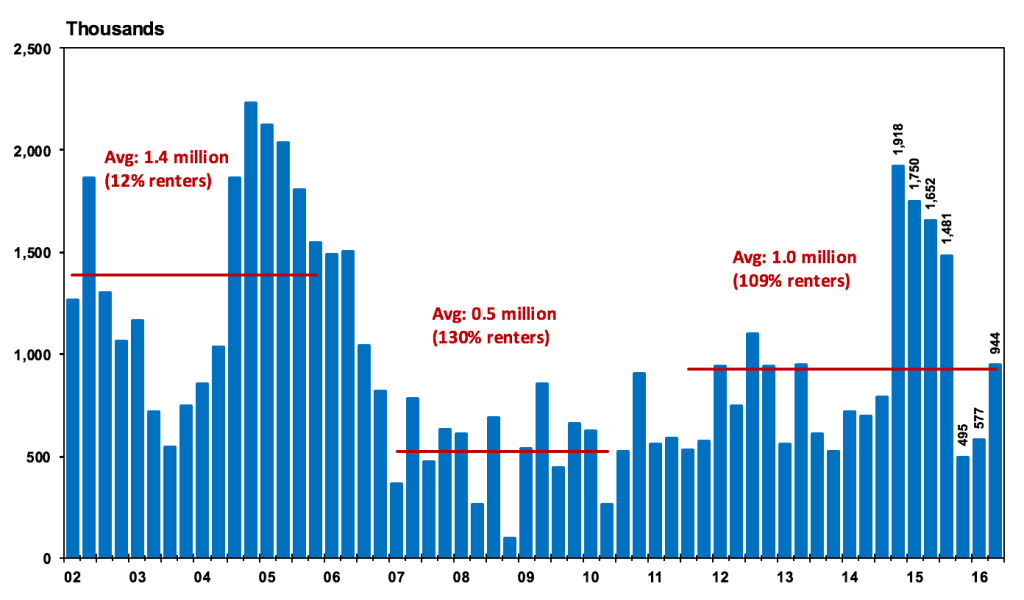

Baker and Dietz both kicked off their presentations by discussing household formation and home-ownership rates. Baker expressed concern about household formation, noting that the national home-ownership rate has fallen to the lowest level in a half century, and that it “looks as if we haven’t quite hit bottom yet.” Household formation is not at historically normal levels but is starting to pick up and is expected to continue as millennials age. However, Baker expressed uncertainty about whether the households formed at that time will be owners or renters.

Dietz noted that a slight recovery in household formation has been seen since the recession, but many of those households are renters. The biggest impediment for younger buyers to purchase homes is the lack of supply of affordable product. Dietz said there is a paradox in the fact that inventory of existing homes is extremely tight while the supply of new homes is growing. There is opportunity for home-building growth, but the lack of both affordable lots and labor is dampening expansion and construction of affordable homes for buyers.

“With affordability decreasing, one of the only ways builders may be able to provide entry-level housing is to build attached, town-home product,” Dietz noted. Townhouse construction is up roughly 30% on a year-over-year basis, indicating that builders are starting to fill the need for attached affordable product, but it’s not nearly enough to meeting demand.

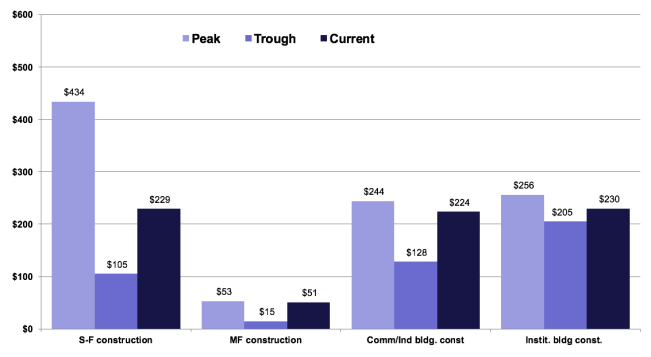

In a highlight of construction spending during peak, trough, and the current period, Baker reported that single-family housing is taking longer than every other sector to recover to peak levels–multifamily is now past-peak levels, and commercial/industrial, and institutional construction are well on the heels of peak levels.

Baker spoke about the state of residential construction briefly during the presentation, focusing primarily on commercial construction. Overall, Baker feels that the single-family housing market has made “healthy gains, but [has a] long, deep hole to dig out of.” [Read more about Baker’s forecast and commentary about nonresidential construction on our sister site ARCHITECT.

Dietz dove deep into the biggest impediments for residential building growth in the future, focusing primarily on the three L’s: labor, lots (the low supply of them), and lending.

The lack of skilled, affordable labor has been plaguing builders across the country for years–and in the first half of 2016. As reported the past three months, construction industry employment continues to shrink. Job openings declined in March, April, and May, and increased in June to 3.0%. However, as the total number of separations continues to outpace the total number of hires, the job openings rate is representative of unfilled positions versus new positions being created and represents a shrinking workforce overall.

National construction industry employment in the residential building sector is up year-over-year, however, a fairly modest 4.3% increase from 690.5 in July 2015, to 719.9 in July 2016 has not eased stress. Dietz noted that in a NAHB survey conducted last year, builders expressed that labor was the top building challenge in 2015 and the top anticipated challenge expected in 2016.

Top States for Job Growth in the Construction, Mining, and Logging Industry: June 2015

1. California: 32.3%

2. Florida: 25.5%

3. Colorado: 13.2%

4. Washington: 12.5%

5. Georgia: 12.2%

5. Iowa: 12.2%

7. Massachusetts: 11.2%

8. Arizona: 11.0%

9. Ohio: 9.9%

10. New York: 8.6%

Jobs in the Construction, Mining, and Logging industry overall have increased most significantly year-over-year in California (32.3%), Florida (25.5%), Colorado (13.2%), and Washington (12.5%). As those states are home to major housing markets like the Bay Area, Tampa, Denver, and Seattle, it’s reasonable to assume that residential housing activity is a contributor to the large gains. Basu noted that two states that suffered mightily during the foreclosure crisis are at the head of the pack, and some of this is due to population growth of millennials in markets like Denver and Seattle.

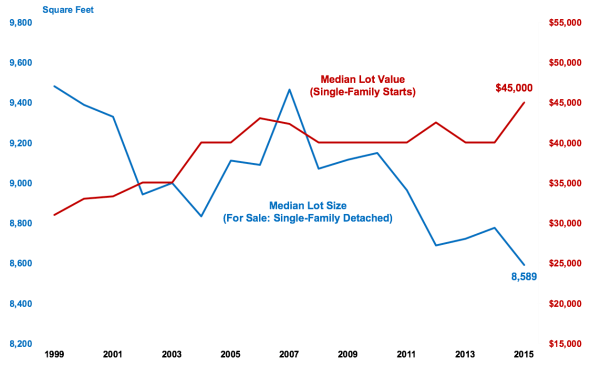

The supply of affordable lots, Dietz’s second L, is also a major impediment for builders. The median size lot for detached single-family homes is getting smaller and smaller, while the median value continues a steep climb. This directly correlates to the low supply of lots in many of housing’s major markets, which is making it nearly impossible for builders to build affordable product and still turn a profit after paying high prices for land to build on.

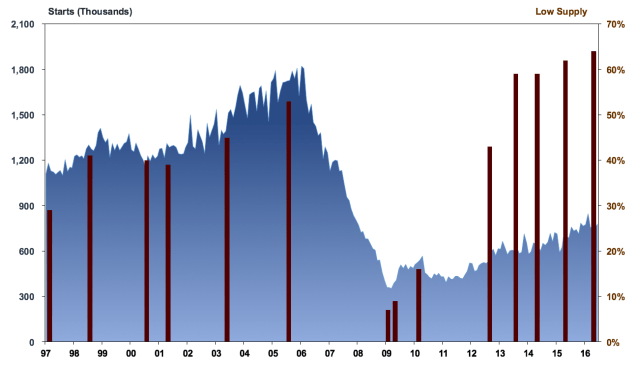

The affordability and supply of lots could be the biggest liability for continued recovery in the residential market. Dietz noted that there has been a 11% growth in in starts during the first half of 2016, but the levels are still well below the normal level of housing starts needed based on population growth and need for new housing. Dietz forecasted continued gradual growth into 2018, but only at levels accounting for 77% of the “normal” rate seen pre-recession.

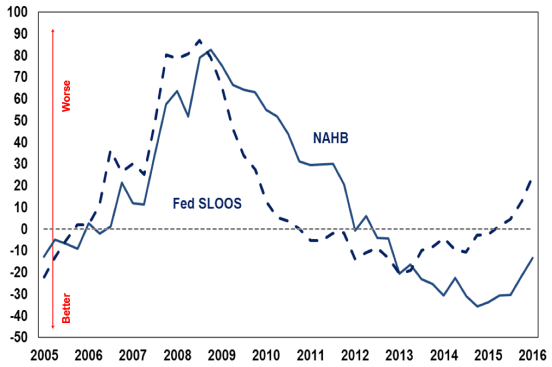

According to Dietz, “the second L (lots) is a function of the third L, lending.” Results of a NAHB survey of builders indicates that lending conditions are currently “easing less,” and that lending conditions are easing more for loans on the construction side, despite the fact that easing is most needed for acquisition, development, and construction (AD&C) loans related to land development. As NAHB’s Eye on Housing blog reported in June, other AD&C loans connected to land development face tighter conditions than loans for residential construction purposes, forcing some builders to gather other sources of capital that may offer less favorable terms. The results of NAHB’s survey are likely skewed negatively due to the fact that builders are in most need of loans for land development that will not impact their overhead negatively.

Dietz also cited regulations and a “lack of action” on the side of the government as a pain point for builders in terms of cycle time and cost of lot development.

While Baker and Dietz both anticipate continued growth and remain optimistic, Basu expressed greater concerns. Despite the fact that demographics are supportive of household formation in the long-run as millennials come-of age, it is Basu’s view that housing activity may be peaking. “With potential over-valuation of homes in Pal Alto and other major markets, any increase in interest rates would mean affordability is completely out the window,” Basu said.

See the full press release about the midyear forecast on the ABC site.