Interest rates are rising. At this point in the expansion, which is supported by improved GDP growth and a nearly 50-year low for unemployment, the Federal Reserve’s monetary policy committee is raising its target for the federal funds rate (a short-term interest rate) to normalize monetary policy. This is occurring after a long period during which the federal funds rate was effectively zero, an accommodative policy stance intended to stimulate economic growth after the Great Recession.

As the economy transitioned from recovery to expansion, the Fed began a series of eight 25 basis point hikes leading to an upper-end target rate of 2.25% in September 2018, with more to come. The policy intent is to raise interest rates, or the cost of capital, thus preventing the economy from exceeding its potential rate of growth and thereby slowing the onset of inflation. Presently, the Federal Reserve’s target rate for inflation is 2%, as measured by the core PCE measure of inflation (a similar measure to CPI but broader and generally a more accurate and lower metric of inflation).

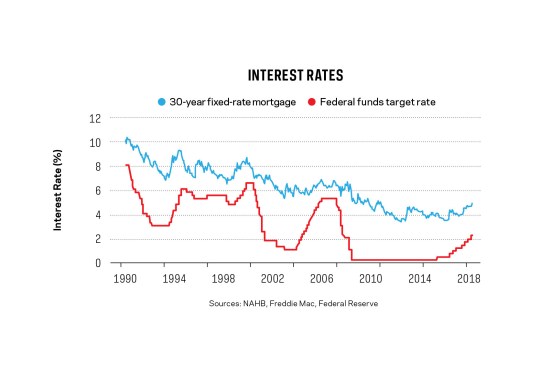

Two questions matter for the housing sector. First, how much higher will the Fed take interest rates? It will continue to raise the funds rate until it reaches the long-run, neutral rate necessary to keep inflation anchored at 2%. Many forecasters believe this rate is near 3.5%. A higher fed funds rate tends to increase mortgage interest rates. NAHB projections indicate that five more hikes would push the 30-year mortgage rate into the mid-5% to 6% range, marking a significant challenge to housing affordability, already weakened due to supply-side construction cost issues.

Second, why 2% inflation? The number is seemingly arbitrary. While inflation of 3% would be worse for savers and investors, it would be helpful for student loan, car loan, and mortgage debt holders. The 2% target was identified in 2003 as a rate of inflation just high enough to give the Fed the ability to lower rates in a recession, without hitting the 0% lower bound.

Ironically, just a few years later the Fed had to reduce the target rate to zero, which at first glance marks the limit of the Fed to lower rates further to stimulate economic growth. But this is not what happened. The Fed developed and deployed other tools, including quantitative easing (bond purchases to lower long-term rates). This is important because if there is nothing economically meaningful about a 2% inflation target, the Fed may be raising rates too quickly now in order to achieve an inflation target that may well be too low. This path would ultimately lead to overly tight monetary conditions and end the current economic cycle early.

The ultimate path for rates may also depend on “r-star,” which is connected to the potential growth rate of the economy. Many economists, including myself, believe the speed limit for economic growth is measurably lower today than it was a few decades ago due to demographics and already-realized changes in technology. A lower r-star would in turn mean that the Fed should keep rates lower on a permanent basis. Unfortunately, recent statements by Fed governors indicate a move away from the r-star approach.

Taken together, these factors emphasize the need for the Fed to move with caution and watch the data in the months ahead. NAHB’s forecast calls for the Fed to stop raising rates in 2019 as the economy slows, thus ending its tightening earlier than many expect.