Will the “best of times”–in economic terms–portend the “worst of times” for housing? Now, with an accelerating economy, astonishingly low unemployment, improving business and consumer confidence, and plenty of stimulus, is this the right moment to start taking chips off the table and shifting into a cautious mode about what’s around the next corner, in 2020 or so?

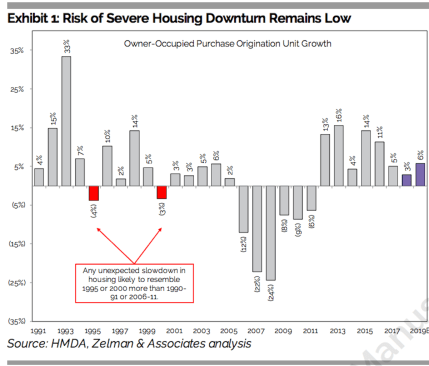

Ivy Zelman, and her team at Zelman & Associates a) make a case for no such over-cautiousness on the part of residential real estate investors, developers, builders, and building materials manufacturers through and including 2020, and b) suggest that, even in a scenario that includes a broader economic downturn within that time period, housing activity would continue to show resilience, with little risk of a severe impact.

Let’s look at a few fresh sources of insight into the backdrop of this conversation, and some of the evidence behind Zelman’s assertion that fundamental forces of demand, as well as ongoing supply-side constraints, will likely limit the damage an economic downturn could inflict on housing’s muted recovery. By the way, if you want to try the Zelman team’s The Z Report on a free-trial basis, click here.

An opportune analysis in today’s Wall Street Journal captures the key measures of mojo currently pumping both optimism and a self-fulfilling virtuous cycle of economic outcomes into today’s macro business environment. WSJ staffer Paul Kiernan reports that, by reliable measures, the economy is motoring along full-steam ahead, and despite a decade-old recovery’s age, shows little sign of losing momentum. Still, Kiernan writes:

Few outside the White House think the U.S. economy will be able to maintain this pace for long, in part because of the country’s aging population. GDP growth has averaged 2.2% during this expansion, with previous bouts of above-trend growth giving way to slower quarters.

It is unlikely to be different this time around, some economists say. “Everyone has growth slowing next year,” St. Louis Fed President James Bullard said in an interview last week, referring to the forecasts of the 15 Federal Reserve officials who meet to discuss monetary policy. “It’s a temporary blip in growth.”

Still, among consumers, confidence is solidly on an upward trajectory, and the outlook, particularly on the jobs and income front, is downright rosy. Gallup editor Frank Newport observes this past week that Americans are quite sanguine about job prospects overall, although a measurably smaller number of people believe now is a moment to find a quality job, versus just any form of employment. Newport writes:

Americans continue to recognize a robust U.S. job market, with 65% saying that it is a good time to find a “quality job,” similar to 67% in May. These are the highest readings in Gallup’s 17-year history of tracking this measure of Americans’ views of the employment situation.

History–not to mention an often-telling flattening yield curve–suggests that every recovery cycle eventually runs out of steam. Still, the strength and geographical and industry-sector reach of the economic lift-off is impressive. National Association of Home Builders senior economist Danushka Nanayakkara-Skillington notes here that some of the strongest growth in employment and payrolls coincides with states with the most new residential building activity. She notes:

Year-over-year, ending in May, 20 states recorded annualized growth above 1.6% in employment, which was the national growth rate. Seventeen states out of the 20 which recorded growth above the national growth rate were in the Western and the Southern (including South Atlantic) regions of the country. Utah posted the highest growth at 3.4%, adding 49,800 workers during this time. Twenty-seven states and the District of Columbia recorded annualized growth between 0.4%-1.5% while Alaska and North Dakota recorded declines in employment.

Basically, the Zelman team’s contention–and an evidence-based outlook for strong growth for a more-than-healthy new single-family housing market through 2020–comes from its tracking of land strategy, investment, and development, which clearly reveals capital already in place, only now ready to start firing on all cylinders.

Here’s a six-point case in point for why Zelman expects not just growth, but accelerating growth for single-family housing activity in the next 30 months.

- a powerful demographic tailwind of aging millennials that should drive demand from apartments into single-family housing

- record low resale inventories, putting more of an onus on builders to satisfy incremental demand from new households

- single-family production currently stands 20-25% below normalized demand

- still-favorable affordability even after a 50-plus basis point increase in mortgage rates since the beginning of the year

- a strong economic backdrop including solid job and wage growth, and

- increasing land investment by homebuilders that should begin to filter through to increasing community count over the next several quarters.

On that last point, the Zelman team expects a rising tide of community count growth by yearend, many of those new communities aimed squarely at the entry-level, first-time buyer market, fueling order activity into 2019 and beyond, with incentives to support pace.

In this case, increased supply will increase demand, and a heretofore muted recovery could begin to a higher-volume housing boom.

Those who are skilled at finding the right lots for the right price in this kind of environment will have an advantage over the mere mortals in the market.