Hear that? It’s the sound of residential investment, development, and construction engines grinding, wheezing, and winding into a late-year, pre-2019 stall. Not exactly what you’d expect amidst a gangbusters economy, strong jobs growth, evidence of upward bound wages, and demographic dynamism that’s only just begun to play out.

Still, builders—and, perhaps more importantly, their investment and lending lifeblood–seem to have begun second-guessing their absolute faith in the fundamentals. Their one remaining lever to stay ahead of and counteract galloping expense- and supply-side forces was their own and home buyers’ access to very cheap capital. That’s now history, and none of the three essentials to most home building models–lots, labor, nor lending–can be gotten cheaply.

Somehow, what was supposed to be the last leg up of the recovery ride is looking more and more like it’s going to be a thrash.

So, November and December 2018 are all about a nearly existential capital allocation quandary. “Should we” or “shouldn’t we” spend money on land? “Where?” Etc.

We are hearing many new-home builders find themselves mired in a rut of malaise. They’re sweating out each shock and series of after-tremors of interest rate increases, each incremental basis-point leap seeming to further dampen buyer enthusiasm.

This malaise has backed its way into home builder sentiment at a high level. Already plagued by ongoing labor capacity constraints’ impact on what they pay to secure start-to-completion predictability, and input cost pressures related to tariffs and escalating materials transport expense, they’re facing genuine demand erosion for the first time in six plus years.

They’ve come sooner to the “fork in the road” than they thought they would, and, what’s more it doesn’t look like they thought it would. You know that spinning symbol you see while you’re waiting for a site to load on your phone? That’s the way this feels, as builders fret the Fed’s next move.

Still, you have to ask, how can they be one bit surprised? At one recent home building, investment, and development conference, a high-level executive was overheard, amid hand-wringing, saying, “we’re really going to have to train our sales people to sell.”

Honestly?

Interest rates were bound to rise, sooner or later, for the past three or four years. It turned out to be later. And now builders are worried about the impact rising rates are exerting on buyers’ monthly payment calculations?

Builders, developers, and their investment partners have had six years to prepare for now, this moment, this inevitable inflection point, from dirt cheap money, to reasonably priced borrowing and investment capital.

And look at where we are. Here’s the simplest way we can think of to illustrate why home builders and investors are hitting the pause button rather than brazenly doubling-down on where there’s a diamond-mine of opportunity to reignite recovery.

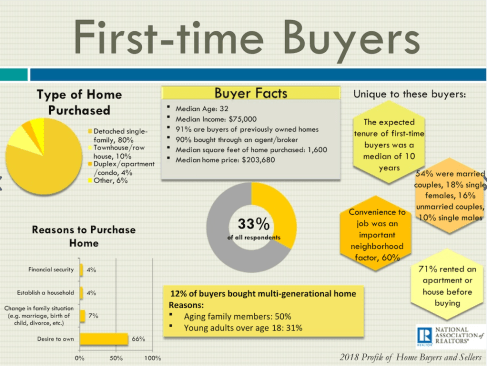

Take a look at evidence Exhibit A. National Association of Realtors latest 2018 Profile of Home Buyers and Sellers cites that first-time buyers–historically representing 40% or more of the home buying universe–have decelerated in their share of the marketplace.

The share of first-time buyers continued a three-year decline, falling 33 percent (34 percent last year). This number has not been 40 percent or higher since the first-time buyers credit ended in 2010.

So, for eight years, market players have been unsuccessful at resuscitating the ability of at least one in 10 would-be buyers to participate in the market. At the suppressed rate of engagement with first-time buyers, the profile of the ones who can price themselves in to turn homeownership aspiration into action look like this, according to NAR. Median age 32, median income $75k, median price paid $200k or so.

New home builders typically would have played an important role in enabling that missing 10% of the universe to kick into gear. But they haven’t to date [and it’s looking more and more as if they may have forfeited their window of opportunity]. Why?

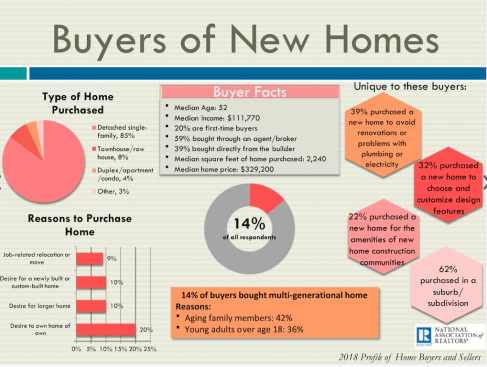

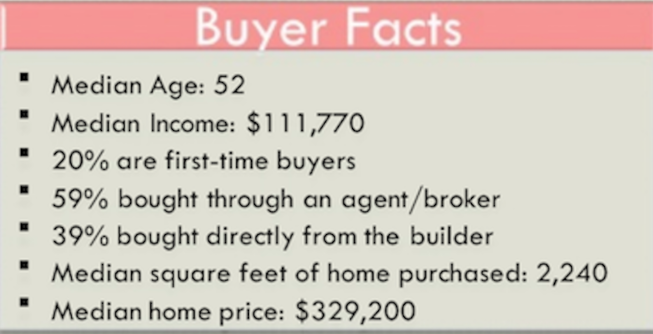

Please consider evidence Exhibit B, the smoking gun. Here’s the NAR profile of new home buyers snapshot of “Buyers of New Homes.” Look at it and ask yourself, “what’s wrong with this picture?”

Zero in more closely at the “Facts” box, and ask yourself, “what’s right about this picture?” Less than 50% is right.

Remember, now, new data tells us that median household income in September 2018 “climbed” to $63,000, per Sentier Research, as reported in New Strategist Press editorial director Cheryl Russell’s Demo Memo.

With that in consideration, you can compare the NAR “first-time buyer” profile with the “new home buyer” profile. Look at one and then the other, and then look again, and you’ll conclude at least the following:

- Too old

- Too rich

- Too big

- Too expensive

This explains why just one of every five new homes sells to a first-time buyer, rather than a norm of one out of every three.

This is why builders are in “spin, and spin, and spin” mode of a website failing to load right now, hesitant to commit more capital investment, with more expensive capital pouring into riskier long-term returns, rather than planning community openings through 2019 that close the gap between their current average prices and what an enormous potential universe of young, working, family-forming, 30-something year-olds would be clamoring for right now.

Alternatives are running out, fast.

Here’s how they look from here.

One, quickly buy into the new-single-family for-rent model that may at least absorb operational costs into a lower-return hedge that would stem the tide on land impairments.

Two, keep up with the Fed phobia, a painful, passive, paralyzing disorder that can compound the negative effect of rising interest rates by further widening the price gap between what first-time buyers can and will pay and what new-home offerings come to market.

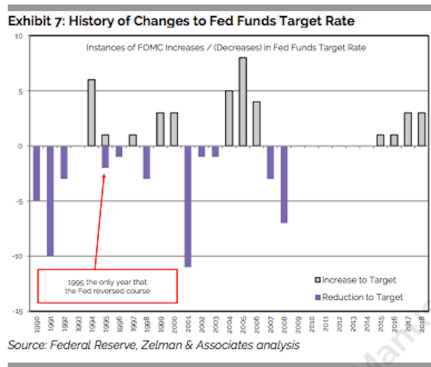

Here’s a perspective, from Zelman & Associates latest twice-monthly compilation of decision-supporting analyses in The Z Report, which may offer comfort or not:

“Next year is setting up for an interesting outcome. History suggests that raising too fast and reversing course is a lower probability scenario. More likely from our perspective would be a balancing act between Fed policy and strength in financial markets and the housing sector, assuming inflation remains under control. If either is too weak, a slower tightening course would likely be pursued, which could ironically stimulate both. Positively, we do not believe that the importance of housing is lost on the Fed.”

Or three, address three hard- but doable opportunity areas that can drive down cost and drive up attainability among the growing universe of young adult households with better and better jobs.

- Productivity: Is there or is there not between 15% and 25% construction cost opportunity gained when home building enters the 21st Century in implementing automation, technology, data, and improved operational modeling?

- Policy: Is there or is there not between 5% and 10% of current local and national regulatory burden–nested in selling prices of new homes–that could be addressed and looked at as an expense opportunity area through new partnership, co-investment, and long-term collaboration models between developers and municipalities?

- And on the driving demand up front, the opportunity is this. Wouldn’t 5% to 10% more of mid-30 year-olds with good jobs, solid households, and brightening prospects make a good bet on America’s part to invest in as future community leaders by giving them more options to enter homeownership, rather than fewer. Couldn’t builders and their investors remove more financial friction from more potential customers?

All in, builders one time or another are going to have to turn frustrations–valid as they may be–that the new construction playing field tilts against them, into actions that will close that yawning gap between what first-time buyers are bringing to the table to participate and what home builders, as market-rate players, can bring to the table for them.

These are not flip-of-a-switch challenges to resolve. Still, if builders don’t. Somebody will.