The recent run-up in hedge fund equity positions in the biggest public home builders is making more than a few executives uncomfortable. The most benign of explanations is that with stock prices dropping, investing in home builders has become a bit of a cheap-chic buy for hedge funds. However, their reputation as flying fast and loose have more than a few keen eyes on heightened alert.

A UBS Securities industry report dated June 12, states that home builder stocks have, as a group, fallen 47 percent from a July 2005 high. However, the firm’s analysts remain confident that “the long-term prognosis for the public home builder is positive,” shoring up arguments that current undervaluations could make for solid investments in the future.

Still, hedge fund managers’ notorious evasiveness typically masks their investment motives. If you’re in senior management at a target company, it’s nerve-wracking to see huge blocks of stock move into their control.

Boyce Watkins, a professor of finance at Syracuse University, explains, “Having a fund manager buy up shares is nice because they provide capital—but they are scary characters. They are demanding. They are very critical. They can be incredibly unpredictable. And they are institutional investors, so they have a lot of power.”

Ask Beazer Homes USA CEO Ian Mc-Carthy just how hard they can tug on the strings at corporate. In October, Mc-Carthy received a letter from Jeffrey Gendell, the hedge fund manager for Tontine Partners, insisting on an immediate and significant share repurchase initiative “above the nominal share buyback initiative the company currently [had] in effect.” As of second quarter 2006 numbers, year-to-date buybacks totaled 2.02 million shares, worth $133.2 million.

True to hedge fund manger form, Gendell declined an interview with BIG BUILDER.

Susan Berliner, an analyst with Bear Stearns, says the missive was typical of Gendell. “Jeff Gendell looks for companies that can affect share repurchases,” she says.

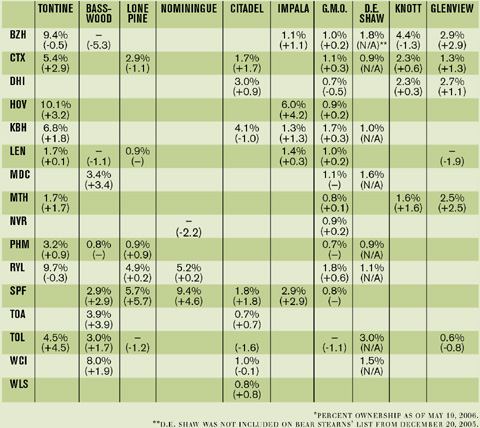

Stock buybacks essentially serve a function similar to dividends: They distribute money to shareholders so they don’t take a major hit on their investments. For an entity such as Tontine, which has significant ownership in companies such as Beazer, Centex Corp., Hovnanian Enterprises, KB Home, and The Ryland Group, that puts a lot of money back in its pockets. (See “Top Hedge Fund Equity Positions” below.)

But will they take the money and run? With hedge fund history thick with unpredictability, it’s tough to see what the writing is on the wall. Watkins explains, “If we’re partners and I’m in it for the long term and you’re in it for the short term, we have different strategies [for growth]—that’s why hedge fund investments can be stressful, [you don’t know what they’re doing.]”

Although the numbers aren’t in for June yet, Berliner says so far, “it doesn’t look like the pace has accelerated” in terms of hedge funds boosting their equity position in the big publics. She attributes the previous month’s “massive” ownership ramp up in companies, such as Hovnanian and Standard Pacific Corp., as pure value plays. “[Hedge funds] believe it just got too cheap and there’s growth potential there,” she says.