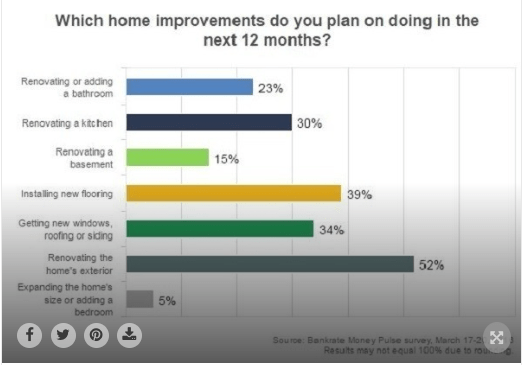

A survey from Bankrate.com released Tuesday reports 36 million homeowners are planning to renovate their homes in the next 12 months. The most mentioned plans in the survey involve work on driveways, decks, patios, pools, landscaping or fencing; next were new flooring, new windows, roofing or siding.

“With more homeowners deciding to make upgrades to their homes this year, it’s a sure sign that they’re generally feeling more secure about the economy and in the housing market as well,” said Mike Cetera, Bankrate.com’s personal loans and credit analyst. “It’s refreshing to see, especially since it wasn’t too long ago that the housing market crashed.”

For homeowners looking to finance their renovations, Cetera suggests visiting Bankrate.com to compare personal loan offers, which can be as low as 5.5% for people with good credit. However, personal loans aren’t the best choices for everyone, so Cetera also recommends homeowners to consider home equity loans and lines of credit, which charge lower interest rates but require homes as collateral. Additionally, people with good credit can qualify for a 0% balance transfer credit card for as long as 21 months.

The homeownership rate is lowest among millennials, but millennials who own homes are more likely to be planning renovations than other age brackets. Surprisingly, homeowners with lower income and less education are just as likely to be planning renovations as those with higher income and more education.

Princeton Survey Research Associates International obtained telephone interviews with a nationally representative sample of 1,000 adults living in the continental United States. Interviews were conducted by landline (500) and cell phone (500, including 293 without a landline phone) in English and Spanish by Princeton Data Source from March 17-20, 2016. Statistical results are weighted to correct known demographic discrepancies. The margin of sampling error for the complete set of weighted data is plus or minus 3.8 percentage points.

Bankrate.com’s report on the survey can be read here.