For much of the past decade, growth in new-home size felt like a given. Rising incomes, accessible financing, and strong move-up demand pushed square footage steadily higher. Today, the national data tells a shifting story.

After peaking just before the pandemic, average new-home size, defined as the weighted average of detached and attached new-home closings, has been generally trending lower, signaling a broader recalibration across the industry.

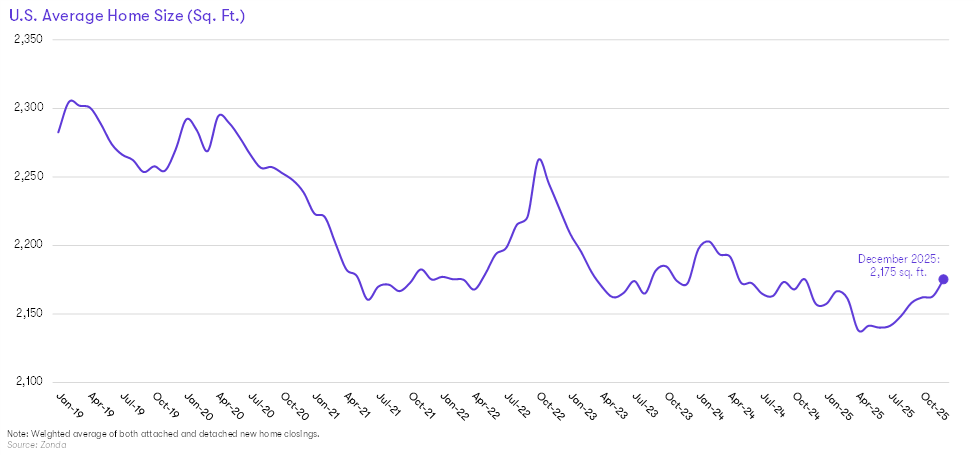

Recent Trends

If we look back to 2019, average new-home size reached its recent high point in February of that year, topping out at roughly 2,300 square feet. From there, sizes began trending lower as affordability pressures started reshaping buyer behavior and builder strategy alike. Even before mortgage rates surged, builders were thinking about attainability and experimenting with more space‑efficient product.

The pandemic temporarily disrupted that trajectory. As remote work took hold and households reassessed how they used space, demand for larger homes surged. However, because new-home data reflects planning decisions made well before closings occur, the impact showed up with a lag. That demand spike became most visible in mid‑2022, when homes conceived early in the pandemic cycle began delivering. Average size briefly expanded, peaking again late that year.

That rebound, however, proved short‑lived. By late 2022 and into 2023, the market environment shifted sharply. Rising mortgage rates, elevated home prices, and broader cost pressures weighed heavily on affordability. At the same time, builders were navigating higher material costs, persistent labor challenges, and a far more rate‑sensitive buyer pool. The result was a renewed emphasis on recalibration with square footage once again trending downward.

By the end of 2025, average new-home size had fallen to about 2,175 square feet. While that represents a modest year‑over‑year change and actually grew throughout 2025 given the healthy move-up and higher-end demand, it marks a meaningful decline from the pre‑pandemic peak.

Strategic Implications

“In the current environment, builders are juggling the healthy demand at the higher price points with the affordability concerns of the wider population,” said Ali Wolf, chief economist for Zonda and NewHomeSource. “Across the different buyer groups, efficiency has become a competitive advantage, though. Buyers are placing greater value on layouts that maximize usability, flexibility, and perceived space rather than raw square footage.”

By focusing on livability, builders can better balance square footage and pricing with demand. In a market where affordability remains the defining constraint for many buyers, the ability to deliver well-designed, right-sized homes is becoming a key differentiator.

The insights in this article were taken from more in‑depth research reports published in Zonda’s National Outlook.