Student loan payments are scheduled to resume in October. This restart follows a pause, known as student loan forbearance, that began March 20, 2020, in response to pandemic-related economic challenges.

The current resumption of payments is separate from the cancellation of student loan debt. The Supreme Court recently struck down the student loan debt forgiveness plan, so there will be no additional debt cancellation.

Student loans are an important discussion for the economy as there are approximately 43.4 million borrowers in the U.S. with student loan balances, representing more than 1 in 10 Americans.

Recent data puts the balance of student loans at nearly $1.6 trillion. This outstanding debt has numerous effects on spending, particularly of younger generations, and the broader economy.

Brief History of Student Loans

The first federal student loans were issued in 1958 thanks to the National Defense Education Act. Offerings, and terms have evolved throughout the decades since, with student loans generally accessible to most Americans today.

The Congressional Budget Office calculates that just over the past 30 years, student loan balances increased from about $200 billion to the current $1.6 trillion. The rise in student loans corresponds with:

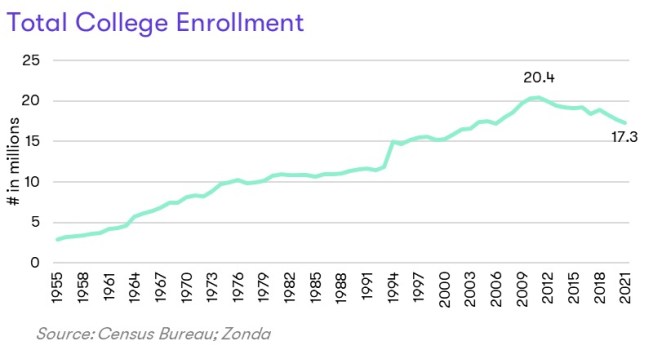

- A rise in college enrollment. College enrollment has increased nearly 20% since the mid-1990s. More students in school resulted in more loans issued.

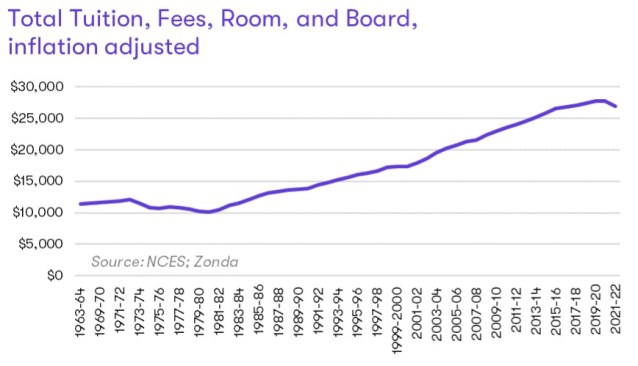

- A rise in costs. Inflation-adjusted college expenses were relatively flat from the 1960s to the end of the 1970s. Starting in the early 1980s, however, there began a steady increase in college expenses. College expenses have grown nearly 70% over the past 30 years.

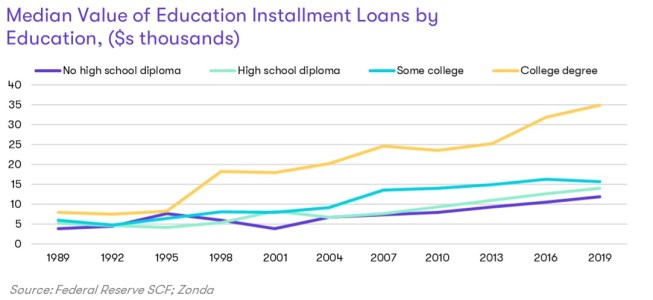

Student loan debt serves as a means to an end. People traditionally take on student loan debt to better their education and enhance their earning potential. Data from the Bureau of Labor Statistics backs this up, with doctoral degrees garnering the highest salaries and those with less than a high school diploma earning the least.

In fact, those that are the highest earners also tend to have the highest student loan balances.

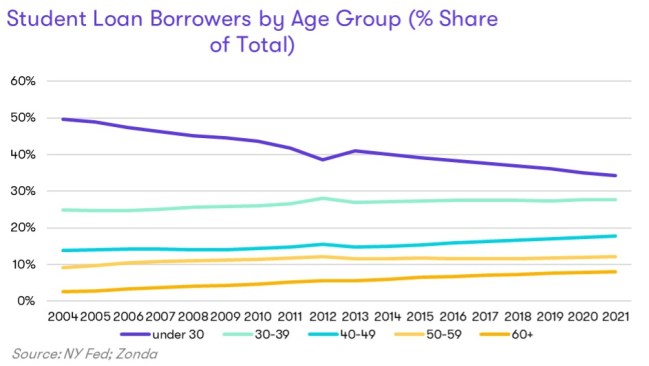

Student loans are concentrated among the two younger generations: Gen Z and millennials (generally those under 40 years old). Those two groups made up roughly 62% of borrowers in 2021 (the latest data available). Those age 60 and older, which would include baby boomers, had only 8% of the outstanding loan balances.

Student Loans and the Housing Market

While, as mentioned, student loans are typically associated with higher earning potential, they are also a monthly debt holders need to pay. Heading into the pandemic, this was troublesome for prospective home buyers who found servicing their debt limited their ability to save for a down payment.

In fact, a 2021 study by the National Association of Realtors showed 50% of those who had bought homes over the previous two years delayed purchasing due to student loans.

This is where the student loan forbearance comes in. As described above, the forbearance went into effect in March 2020. This policy allowed borrowers to not make their student loan payments and prevented interest from accruing on the accounts.

The original plan was to keep the forbearance in place only during the worst of the pandemic economic woes, but the program was extended eight times from 2020 to 2023.

As part of the recent debt ceiling negotiations, the forbearance was finally canceled with payments scheduled to resume 60 days after June 30. The Department of Education announced interest will start accruing beginning Sept. 1, with payments to resume in October.

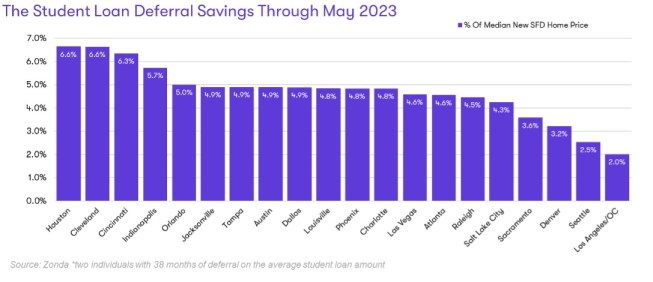

While the payments are set to resume, the forbearance over the past three years was a game changer for some in the housing market. According to the latest Economic Well-being of U.S. Households report from the Federal Reserve, the average monthly payment for student loan borrowers was $200 to $299 per month. If we extrapolate out the high end to a household where two people have the average student loan amount, both retained their employment, and, thus, saved the student loan funds, the savings would be nearly $600 a month. Some people used this money to pay down debts, while others put it toward a down payment on a home.

As seen in the graph below, in more affordable markets in the Midwest and South, the student loan savings would amount to about a 5% to 6% down payment. In expensive areas like Los Angeles/Orange County, the savings were not as substantial given the higher home prices, but they could still put a family within the realm of a low down payment mortgage.

Implications

As mentioned, the student loan forbearance program is set to end later this year. For those that have benefited from the program, the resumption of payments may come as a shock, especially to those that grew accustomed to the extra funds each month.

The anticipated impact on the economy is mixed. The excess money in the economy has likely contributed to today’s elevated levels of inflation. If consumers pull back on spending, this could help ease inflation and take the pressure off the Federal Reserve.

Conversely, consumers represent nearly 70% of U.S. gross domestic product so a change in consumer spending won’t go unnoticed in the broader economy. In fact, a Morning Consult survey of student loan holders found 74% of respondents plan to reduce spending on nonessentials to afford their student loan payments, 69% plan to reduce travel or cut back on unnecessary trips, and 67% plan to find additional work or increase working hours to earn more.

For housing, we should celebrate that many Americans were able to get a head start on saving for a down payment thanks to the forbearance program. As that policy ends, we need to understand that student loan headwinds that turned tailwind since 2020 will again reverse. Navigating affordability has been and will continue to be the primary challenge for the housing market going forward.