Adobe Stock/Yuri Gubin

The old joke about the Jacksonville, Florida, housing market is that it resembles a senior citizen driving down the highway at 55 mph in the left lane with the blinker on. In other words, the market was moving, but at a slower pace than other parts of Florida. However, this is no longer the case.

The demographics of the Jacksonville MSA (defined as Baker, Clay, Duval, Nassau, and St. Johns counties) point to continued growth of the market, with the household growth rate estimated at 7.7% over the next five years. Compare this with the national rate of only 2.5%, and it’s easy to see that Jacksonville will be growing both from within the market as well as from in-migration from outside of the area. The population is expected to grow from 1,599,001 in 2021 to 1,724,538 by 2026, a gain of 125,537.

A key ingredient to Jacksonville’s growth is the job market. Jacksonville is fortunate to have a diverse economy, and the key industries include financial services, advanced transportation and logistics, health and biomedical, advanced manufacturing, IT and innovation, and military/defense contracting. It also doesn’t hurt to have a world-class port, which has benefited from infrastructure investment including a deepening of the channel, a new vessel turning basin, and more than $100 million in berth enhancements.

Jacksonville lost 91,700 jobs from December 2019 to April 2020, but since then has recovered 75% of those jobs (through March 2021). This compares favorably with Orlando (34%) and South Florida (55%). The statewide average during this same period was 59%. Moreover, the Florida Department of Economic Opportunity has forecast job growth of 91,000 through 2028, an estimate this author deems conservative.

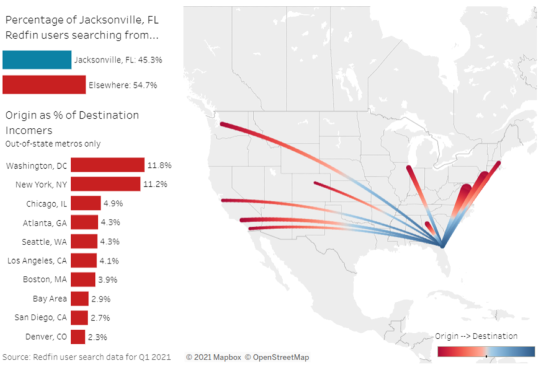

2020 was the year of the Great Migration, as working from home became the norm. The result was that thousands of households decided to move from higher-cost housing markets (coastal) to more affordable markets (non-coastal). Florida also benefited from this, as our markets here are more affordable than our primary in-migration markets from the Northeastern U.S. The Redfin migration map for Jacksonville illustrates that the migration pattern is from not only the Northeast, but Chicago and the West Coast as well. Note that 55% of the housing searches are from outside the area, and we know that these buyers have as much as 30% to 40% more purchasing power than the locals do.

The net effect of this good news to the housing market is that Jacksonville led the state in the annual starts pace, at 20.5% annual growth. The current annual starts pace of 11,131 is 67% of the peak starts pace observed in the fourth quarter of 2005, and it is 145% of the 20-year long-term average annual starts pace. The only major market in Florida that has outperformed Jacksonville in this metric is Sarasota. Jacksonville’s affordability relative to other markets in Florida suggests that those looking to move here will have Jacksonville on their short list.

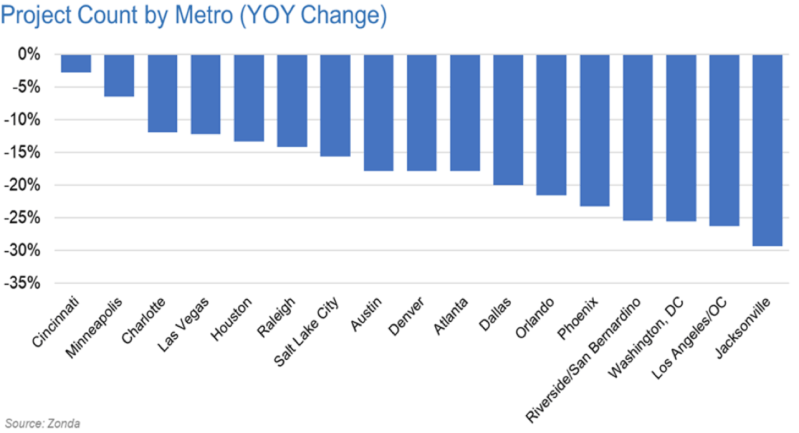

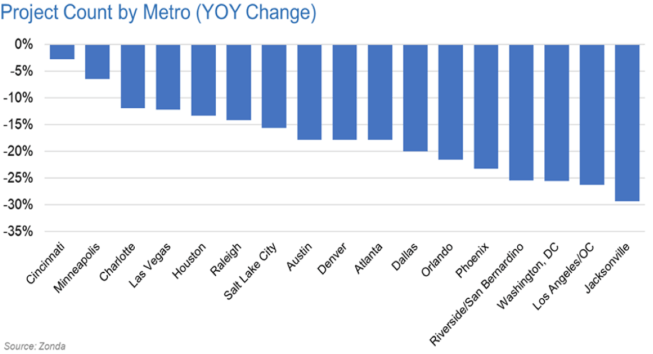

The robust housing activity in Jacksonville has revealed two weaknesses in the market, which is a declining community count and a constraint in vacant developed lots (VDLs). Jacksonville ranked dead last in the year-over-year change in active communities among the major metro areas in the U.S. The goldilocks zone of VDLs for Jacksonville is 24 to 36 months of supply (MOS). St. Johns (20 MOS), Clay (16 MOS), and Duval (14 MOS) all are currently below VDL equilibrium.

The national public home builders, with their strong balance sheets and access to capital, and several pure play developers are snapping up land opportunities as quickly as possible to keep up with demand. Add into the mix single-family build-to-rent developers, who also compete with the for-sale market for land, and it’s no wonder that the land acquisition picture in Jacksonville has gotten more challenging.

Further aggravating the situation is the lengthening entitlement processes in many counties. Paul Michael, vice president of land acquisition for KB Home’s Jacksonville division, notes that “entitlements of new projects didn’t keep pace with market demand, and the entitlement time frame has lengthened.”

Another concern is the recent decision to transfer Army Corps of Engineers permitting to Florida so that the state can manage its own Clean Water Act program. While beneficial to programs such as the Everglades restoration, it remains to be seen whether the state has the bandwidth in the near term to handle all of the new and existing projects that require such permitting.

We believe that builders and developers will find a way to tackle the more complex land acquisition and entitlement issues, as they usually do, and the overall abundance of raw land is still an advantage when compared with other Florida markets.

Also, with hurricane season right around the corner, consider the fact that there’s never been in recorded history a landfall from a Category 3 or higher hurricane in Jacksonville.

What’s the forecast? Sunny as ever.