Housing market conditions in the Phoenix MSA have changed rapidly in the latter half of 2022. An affordability crunch along with growing macroeconomic concerns and inflation levels higher than the national average are resulting in quickly deteriorating demand for homes.

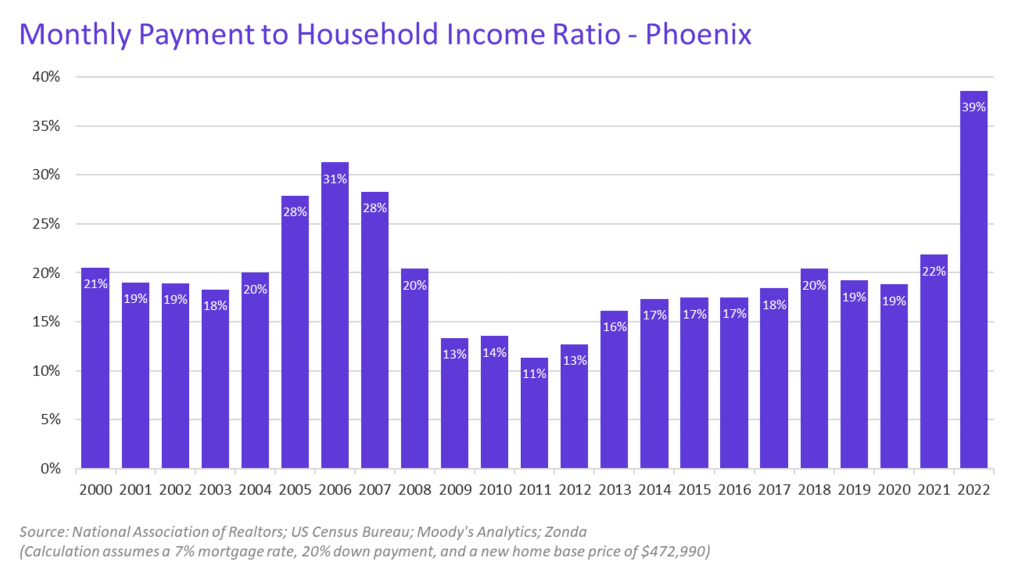

Historically high prices and 7% mortgage interest rates shrank the potential buyer pool considerably and are also making new-home buyers rethink their purchase decisions out of choice or necessity. A quick income-to-payment calculation shows that the typical Phoenix household would need to spend close to 40% of their monthly income on housing, higher than levels seen during the mid-2000s housing boom.

Data from Zonda’s new-home database indicates that monthly net new-home sales contracts have fallen every month since January across the Phoenix MSA. Current new-home sales contract activity is the lowest since at least 2015. The slowdown in net sales contracts can largely be attributed to continued high cancellation rates. According to Zonda, the cancellation rate (gross sales divided by cancellations) has hovered at 50% or higher since late August. Buyers are canceling for a variety of reasons, including qualification issues, economic uncertainty, and fear about how the housing market will progress.

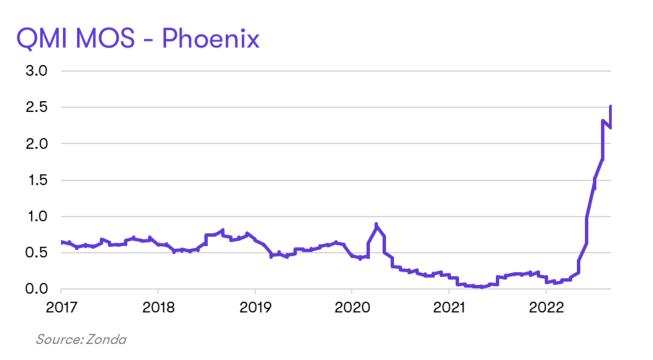

This prolonged period of high cancellations has created an inventory problem for home builders. Zonda data shows a dramatic increase in quick move-in (QMI) inventory homes across Phoenix. After bottoming out below 100 units in mid-2021, there are now over 2,000 QMI inventory homes that builders are holding. Our current calculations indicate there are 2.5-plus months of supply of QMI homes.

The nominal number of inventory homes is less concerning than the rate of change and its implications. Builders are reacting to this sudden glut of inventory homes by putting major emphasis on selling these homes, mostly in the form of higher incentives and discounts.

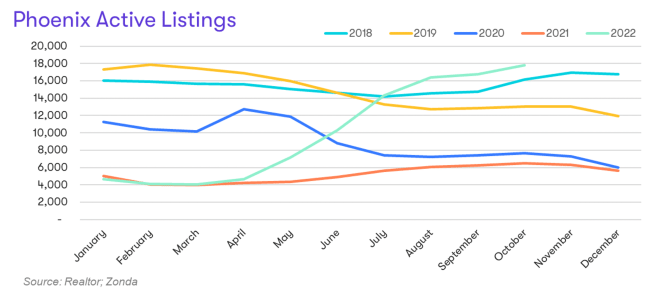

In addition to rising new-home supply, resale supply has risen quickly as well. After reaching historic lows earlier this year, existing supply is now back to 2018 levels. Resell sellers, which include some iBuyers and flippers that are less impacted by the so-called lock-in effect, are also willing to drop list prices and work with buyers to help secure a sale.

This rapid rise in inventory indicates that there will likely be an elevated level of incentives and price cuts in the near-term as builders and existing home sellers do what they need to do to sell homes. We expect prices to continue to retreat as market price discovery continues.

While near-term headwinds are growing increasingly complicated, and we think the market may get worse before it gets better, it is important to remember that the medium- to long-term outlook for Phoenix remains positive. Migration patterns alone create opportunities for the home building industry. Other factors that still make Phoenix an interesting place for the home building community include diversified jobs (with major investments from the semiconductor and electric vehicle industries), relative affordability to other major markets on the West Coast, and low taxes. Once market forces redefine equilibrium in the residential real estate market, we expect a more stabilized market for builders and developers that spend the time understanding what consumers want, where they want to live, how they want to live, and what they are willing to pay for.