When builders think about major universities, the conversation often centers on rentals and student housing. That lens misses a broader point. The largest universities in the country are also powerful drivers of for-sale housing demand, not because they create sudden surges in activity, but because they provide a steady, long-term foundation for buyers across multiple price points.

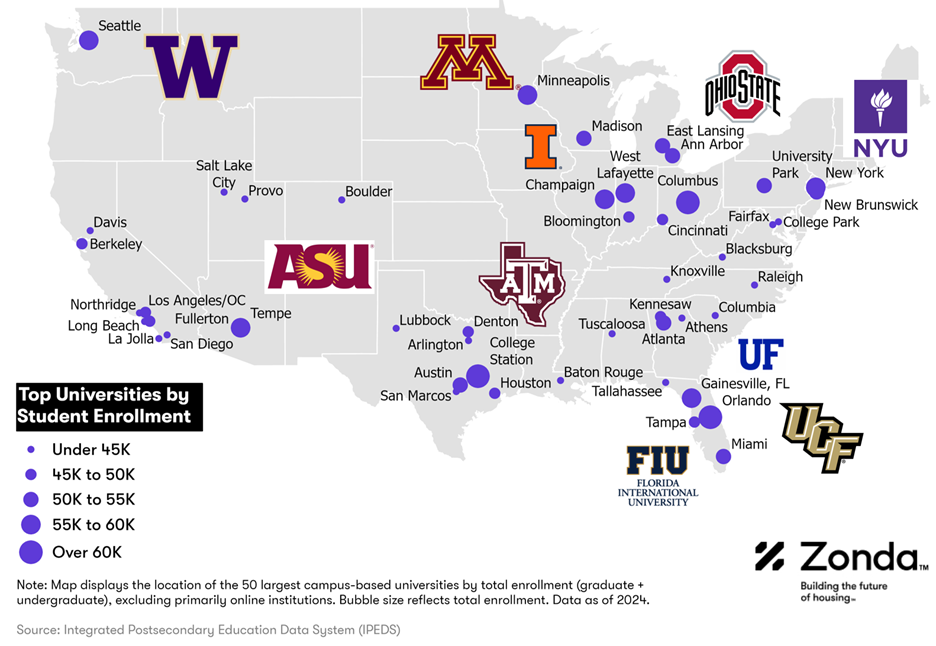

At the most basic level, scale matters. The map below highlights just how large many of these institutions have become. Universities such as Ohio State in Columbus, the University of Central Florida in Orlando, Texas A and M in College Station, and Arizona State in Phoenix each enroll more than 50,000 students. Schools of that size function less like traditional campuses and more like small cities. They support extensive employment bases that extend well beyond the classroom.

That employment base is where the for-sale story starts. These universities employ thousands of faculty, administrators, healthcare workers, and researchers, many of whom build long-term roots in the market. In Columbus, Orlando, and Phoenix, this translates into a consistent pool of buyers seeking entry-level and move-up housing within commuting distance of campus. The demand may not spike the way it does in more cyclical job-driven markets, but it rarely falls off meaningfully either.

The influence becomes more pronounced in markets where the university is tied closely to a broader economic ecosystem. In Austin, the University of Texas sits alongside a growing technology sector, helping retain graduates and supporting demand that extends into higher price points. In Seattle, the University of Washington anchors a similar dynamic, feeding into a deep pool of highly educated workers who transition into homeownership. In both cases, the university is not acting alone, but it is playing a central role in shaping the buyer pipeline.

That pipeline is critical and often underappreciated. Large enrollment universities continuously produce future homeowners. This is especially true of educated young adults who already have ties to the area. When those graduates find local employment, they are far more likely to remain in the market and eventually purchase a home. Over time, this creates a self-reinforcing cycle that strengthens demand.

Geography also works in favor of builders. While student demand clusters near campus, ownership demand tends to spread outward. Faculty and staff often look to nearby suburbs or secondary neighborhoods where they can find larger homes, better school districts, and more long-term stability. This creates a ripple effect that supports sales activity across a wider portion of the metro.

Another layer of support comes from the mix of incomes associated with major universities. Large research institutions attract federal funding, private investment, and affiliated employers, which in turn bring higher wage jobs into the area. That income diversity supports demand across a broader set of price tiers, from entry-level homes to more expensive move-up products. Builders operating in these markets often benefit from a deeper and more balanced buyer pool than they would find in similarly sized metros without a university anchor.

The biggest impact, however, is stability. Universities are long-term institutions that are unlikely to relocate and tend to expand over time. That consistency helps anchor housing demand even when other parts of the local economy soften, and in a housing market where volatility has become more common, that kind of demand foundation is increasingly important.

The insights in this article were taken from more in-depth research reports published in Zonda’s National Outlook.