Home prices continued to rise nationally in 2024, compounding the historic affordability challenge that home buyers face amid ongoing mortgage rate volatility. Following rising home prices, both the Federal Housing Finance Agency (FHFA) and Federal Housing Administration (FHA) announced new loan limits for 2025. These higher limits will make it easier for buyers to secure a mortgage and purchase a home.

The changes apply to both conforming and FHA loans. In fact, 98% percent of U.S. counties will see higher conforming and FHA loan limits in 2025, an increase from 84% that received higher limits in 2024.

Conforming and FHA loans differ in loan limits, credit scores, and down payment sizes.

- Conforming loans are conventional loans that “conform” to loan limits established by the FHFA as well as criteria set forth by Fannie Mae and Freddie Mac, which purchase these loans and sell them to investors as mortgage-backed securities. Some of Fannie Mae and Freddie Mac’s criteria include higher credit scores, larger down payments, and lower debt-to-income ratios. While these loans are not backed or insured by a government agency, Fannie Mae and Freddie Mac operate under federal government conservatorship, which provides an implicit guarantee of their obligations. This implicit backing was underscored when the federal government bailed out these agencies during the Great Recession.

- FHA loans are nonconventional loans that are insured by a government agency, the FHA, which protects a lender financially should the borrower default. FHA loans are used by home buyers who struggle to qualify for conventional loans, particularly many first-time buyers, as they require smaller down payments and lower credit scores. These loans are restricted to the purchase of a primary residence only.

According to data from the Mortgage Bankers Association’s Weekly Mortgage Applications Survey for the last week of November, conventional loans comprised 70% of total loan applications, while FHA loans were 16% of loan activity. Note, conventional loans include conforming loans and other types, like jumbo and subprime.

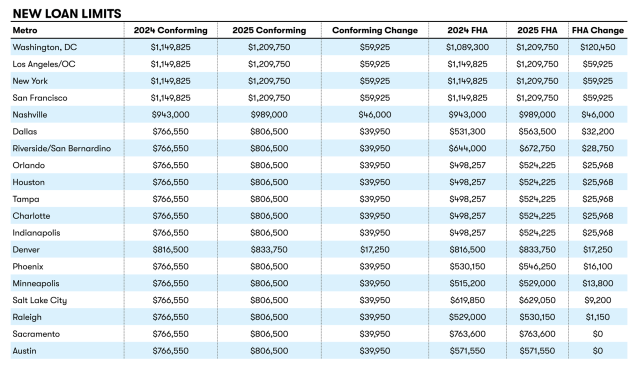

On Nov. 26, the FHFA announced the national baseline conforming loan limit value will be $806,500 in 2025, marking an increase in the floor of 5.2% over 2024 to match the rate of appreciation seen in the national FHFA House Price Index in the 12 months ending third quarter 2024. For high-cost areas, where 115% of the local median home value exceeds the baseline conforming loan limit, the conforming ceiling will be $1,209,750, an all-time high.

The FHA also sets a ceiling and floor each year for its loan limits based on median home prices. The new floor for FHA loans in 2025 has been set at $524,225 and will be applicable in places like Charlotte, North Carolina; Houston; Indianapolis; and Orlando and Tampa, Florida. For 2025, 86% of all counties will receive the minimum limit, in line with 87% in 2024.

Like conforming loans, the revised FHA ceiling of $1,209,750 for 2025 is 5.2% higher than $1,149,825 in 2024. Large coastal markets that have high home prices, like Washington, D.C., Los Angeles/Orange County, New York, and San Francisco are subject to the new ceiling.

Below are the revised FHFA and FHA loan limits for select markets across the country.

Sources: Department of Housing and Urban Development, Zonda

Note: Some counties may have different numbers; data is from most affected county.

The new FHA loan limits will have a larger impact on the new-home market than the updated conforming limits. Subscribers to Zonda’s National Outlook can log in to see the most impacted housing markets.