Spring selling is on, and construction cycles have shifted into high gear in many markets and states, even as winter temperatures and weather grip the nation’s northern third regions.

Demand–providing prices navigate a shifting obstacle course of attainability–is there.

More questions and more nerves about 2018 year-end results and beyond that trace to supply.

At a time many builders are working with suppliers on allocations of materials and products to secure a reliable, sequential order to what shows up at their building sites, prices are in flux. Some categories of materials, such as framing lumber, have been swept into a macro U.S. foreign policy pivot on global trade, spurring the prospect of new import tariffs that would add cost to products coming in from Canada and elsewhere.

The ultimate effects, in absolute dollars, on how those dynamics will impact builders’ costs and what they’ll need to try to pass along to home buyers, are still unknown. What’s known now is that there’s been a sharp, new infusion of volatility, unpredictability, and a queasy sense that things will get worse rather than better when it comes to what builders feel they’ll have to pay for these materials.

The National Association of Home Builders reports that “the tariffs are harming housing affordability, causing extreme price volatility and incentivizing foreign nations to boost lumber exports to the U.S. because of record-high prices.”

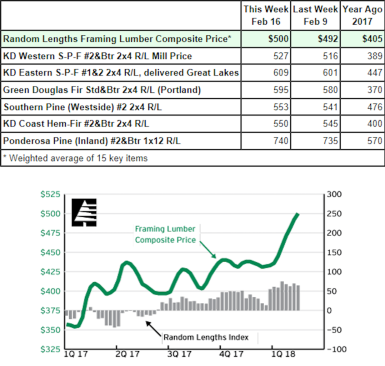

Here, from Random Lengths Lumber Market Report this week, is some commentary on the topic:

Following a measured start to trading, framing lumber sales picked up after midweek, and many key prices continued to forge higher. More price records fell, while many other prices having already far surpassed previous highs moved higher still. … The Random Lengths Framing Lumber Composite Price hit the $500 mark, closing in on its all-time high of $510.

Former ProSales editor Greg Brooks argues here that framing lumber only represents 7% or less as a direct expense factor in the selling price of a home, and wonders “what’s the big deal” if it kicks up a monthly payment by $20 or so?

In isolation, that argument may hold, but reality for builders is that the framing lumber issue is not going on in isolation. Brooks’ analysis self-validates around an attempt to directly correlate lumber price trends and house prices, suffers from “framing bias.” It looks at the trends during too short a time period, and through too narrow a matrix of variables. What his assertion fails to prove is that builders are overstating their worries over where prices–including those for framing lumber–are going.

Suddenly, the economy is showing signs–some of them eerily nuanced and out of clear sight–of an inflationary onslaught. Fact is, for builders–especially when they’re trying to engineer their operations and products to meet lower price tier opportunities against a range of opposing forces–land prices, regulatory fees, and skilled labor capacity challenges–everything counts.

A thousand dollars here, a thousand dollars there, and like the late Illinois Republican Senator Everett Dirksen is quoted as having said, “pretty soon you’re talking real money.”

Everything counts, and if builders are really good at anything–which they are–they’re good at paying attention to lots of details simultaneously, because that’s what it takes to deliver value to a home buyer.

And, if there’s anything lurking behind or underneath cost volatility and unpredictability, it’s reasonable to be wary of further dramatic cost increases coming out of these clouds of uncertainty.

And then there’s labor. Higher Spring starts rates tend to go with iffy weather, which tends to go with stalled start-to-completion cycles, which tends to go with labor bottlenecks, capacity constraints, missed windows of opportunity, and, ultimately, home buying customers who don’t get what they expected when they expected it.

It’s a vicious circle, and no in-year tactic however effective, is going to solve for it.

From our outside vantage point, we think that builders will only begin to solve for their need for predictable, quality, caring skilled craftsmen and women if they apply some of the same level of resources, fanatical focus, and opportunism they put to use in their pursuit of land deals to the challenge of bringing in a next generation of skilled construction producers.

If they do, they’ll look at the following three big, honking challenges of why young people don’t want to go into the building trades in a different way:

- Pay

- Harsh workplace conditions

- Insecure career path

These are realities. But are they fixed in place, or could technology, improved processes, greater productivity, and a clearer sense of mattering impact an evolution from “the way things are” to a way they could be?

If builders focused on people and productivity processes with the same acuity, precision, forward-planning, and investment they bring to their land game, they’d get to 2020 with a whole new outlook on how they’ll deploy resources to generate value in housing.

So, while you’re hoping weather conditions cooperate with your plans to pour all those slabs and get your rough framing stages to plate-level, roof-ready, think past your 2018 delivery goals to where you’ll need to be, with people, in 2020.