U.S. Senate lawmakers, back in Washington after Thanksgiving holidays, are working on the double to fast-track a major tax code overhaul through to a vote on the floor this week. The aim is to take a passed Senate bill to conference–a committee of both Senators and House members–for reconciliation of its bill with legislation voted on two weeks ago in the House.

As is widely reported, the current Senate version of tax reform may need revisions–both in its cost implications and in whom it’s benefits impact–to successfully navigate push-back from Senators who could deter its passage. Word is, if the Senate passes an amended bill by just a vote or two, its compromises may be so stretched to the limit that it may simply hand the bill over to the House with a “take it or leave it” message.

The two bills differ, and that is not only a reflection of the composition of different branches of Congress. Each bill is laden with intent, not just to rewrite tax code and cut taxes, but in most cases, to ensure future financial political support and re-election of voting members. It’s deliberate. Included in each measure are negotiating chits.

The conference committee–should the Senate cobble enough votes to pass its bill–will have its work cut out for it identifying where each bill contains a veiled negotiable item, one that can be horse-traded without costing too much support.

An area that’s causing a lot of anxiety among residential developers is the proposed elimination of corporate deductibility of private activity bonds in the House measure. These bonds are a critical “front end” incentive, practically essential to the development of most tax credit backed affordable housing in the United States, and the elimination of deductibility would materially harm the progress of at least some new affordable developments into the stage where a complex stack of financing funds further development, construction, and term lending for operations.

Few have noted, however, that PAB deductibility doesn’t affect affordable housing development alone. It’s a linchpin to many market-rate masterplanned communities and other market-rate developments, where special use tax districts are created by municipalities to create infrastructure–roads, water and sewer systems, bridges, etc.–necessary to grow, allowing further residential building to occur.

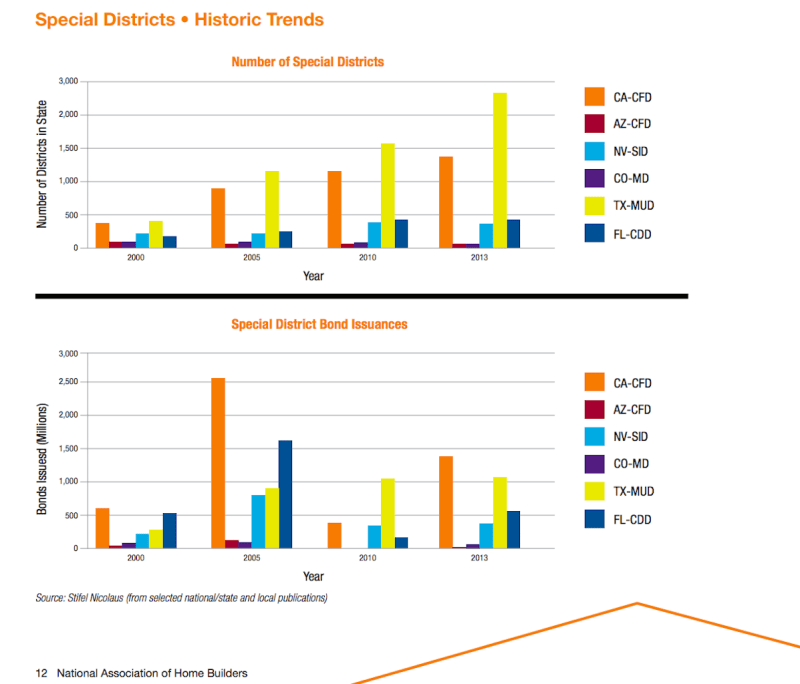

The National Association of Home Builders notes that special district financing involves the issuance of tax-exempt bonds to finance public improvements within a specified geographical area, or distrit… The bonds are repaid from the special taxes, assessments, and/or an ad valorem property tax imposed on the land within the district. The bonds are typically underwritten in private offerings managed by underwriting firms who specialize in this type of land-secured financing.

Source: National Association of Home Builders

Various state statutes and local ordinances provide authorization for Special District financing. The nomenclature for Special District varies according to location, but some of the more common Special District names include metropolitan districts (“Metro District”), municipal utility districts (“MUD”), public improvement districts (“PID”), special improvement districts (“SID”), special assessment districts (“SAD”), community facility districts (“CFD”), improvement districts (“ID”), community development districts (“CDD”), and tax increment financing districts (“TIF”).

The thought among at least some pro-housing lobbyists is that the elimination of PAB deductibility may be a House negotiating chit, to get Senate members in conference to compromise on a stance the House may regard as non-negotiable.

If PAB deductibility is eliminated in a tax reform law that surfaces out of Congress and lands on the President’s desk for his approval, builders may be looking at material risk to impact fee estimates, as that may be municipalities’ only recourse to fund public infrastructure necessary to support more residential building.