TRI Pointe Group, Inc. (NYSE:TPH) on Thursday reported net income of $71,000, or $0.00 per diluted share, for the first quarter of 2019 ended March 31, compared to net income of $42.9 million, or $0.28 per diluted share, for the first quarter of 2018. Analysts were expecting a gain of $0.02 per share.

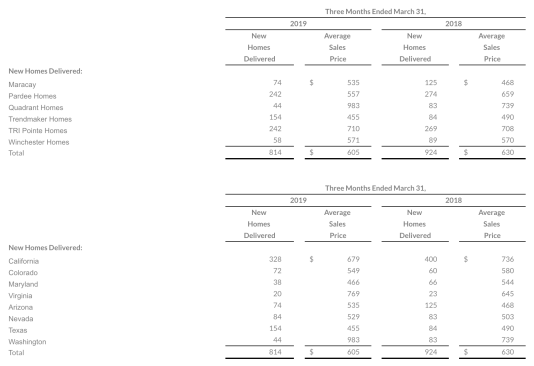

Home sales revenue decreased $89.9 million, or 15%, to $492.7 million for the quarter, compared to $582.6 million for the first quarter of 2018. The decrease was primarily attributable to a 12% decrease in new home deliveries to 814, compared to 924 in the first quarter of 2018, and a 4% decrease in the average sales price of homes delivered to $605,000, compared to $630,000 in the first quarter of 2018.

Home building gross margin percentage for the first quarter of 2019 decreased to 14.4%, compared to 22.7% for the first quarter of 2018. The decrease in home building gross margin was due to a lower mix of deliveries from certain long-dated California communities, which produce gross margins above the company average, as well as $5.2 million of expenses related to lot option abandonments. In addition, gross margins were negatively impacted by increased incentives in the second half of 2018 on inventory homes that delivered in the first quarter of 2019 as well as purchase accounting adjustments related to the acquisition of a Dallas–Fort Worth-based home builder in the fourth quarter of 2018. Excluding interest and impairments and lot option abandonments in cost of home sales, adjusted home building gross margin percentage was 18.4% for the first quarter of 2019, compared to 25.2% for the first quarter of 2018.

Sales and marketing and general and administrative (“SG&A”) expense for the first quarter of 2019 increased to 15.7% of home sales revenue as compared to 12.9% for the first quarter of 2018, primarily the result of lower operating leverage on the fixed components of SG&A as a result of the 15% decrease in home sales revenue and higher overhead costs as a result of expansion efforts into the Carolinas, Sacramento and Dallas–Fort Worth markets.

Other income increased $6.1 million to $6.2 million for the first quarter of 2019 as compared to $171,000 for the first quarter of 2018. The increase was largely due to the $6.0 million reduction of our income tax liability to Weyerhaeuser company. During the three months ended March 31, 2019, the company amended the existing tax sharing agreement with Weyerhaeuser, pursuant to which the parties agreed, among other things, that the company had no further obligation to remit payment to Weyerhaeuser in connection with any potential utilization of certain deductions or losses with respect to federal and state taxes.

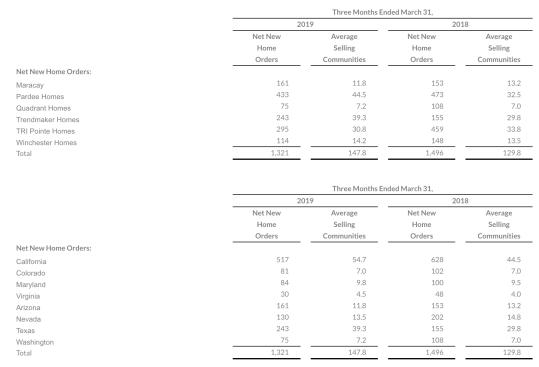

New home orders decreased 12% to 1,321 homes for the first quarter of 2019, as compared to 1,496 homes for the same period in 2018. Average selling communities increased 14% to 147.8 for the first quarter of 2019 compared to 129.8 for the first quarter of 2018.

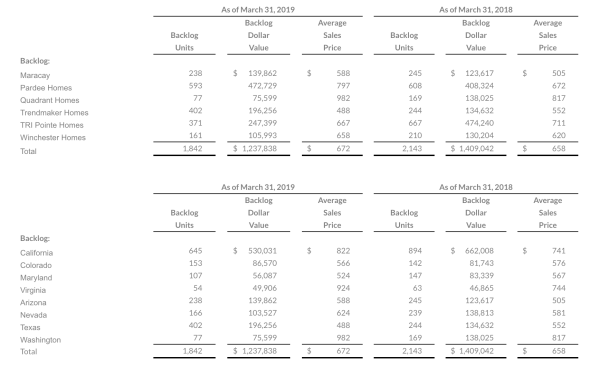

The company’s overall absorption rate per average selling community decreased 21% for the first quarter of 2019 to 8.9 orders (3.0 monthly) compared to 11.5 orders (3.8 monthly) during the first quarter of 2018. The company ended the quarter with 1,842 homes in backlog, representing approximately $1.2 billion. The average sales price of homes in backlog as of March 31, 2019 increased $14,000, or 2%, to $672,000, compared to $658,000 as of March 31, 2018.

“New home demand rebounded nicely in the first quarter of 2019, as buyers responded positively to the decline in interest rates and a more competitive pricing environment,” said TRI Pointe Group Chief Executive Officer Doug Bauer. “TRI Pointe Group averaged 3.0 orders per community per month during the period, which represented a 44% improvement from the fourth quarter of 2018 and exceeded our internal projections. California continues to be an important market for TRI Pointe Group, and we saw encouraging results as we moved through the quarter with orders per community per month of 2.0, 3.5 and 3.9 for January, February and March, respectively. We are optimistic we can sustain this momentum as we head into the latter half of the spring selling season.”

Bauer continued, “We grew our quarter-end community count by 11% as compared to last year, giving us a solid platform from which to grow. The increase in community count was a combination of growth in our existing markets, expansion into new markets and the continued rollout of new projects from our long-dated California assets. We expect to leverage all three avenues for growth going forward as our business evolves.”

“While the decline in interest rates played a key role in sparking demand in the first quarter, we believe the appeal of our premium lifestyle products and the focused efforts of our sales and marketing teams had an equally important impact,” said TRI Pointe Group President and Chief Operating Officer Tom Mitchell. “We strive to build homes and develop communities that create an emotional connection with customers. We continue to emphasize targeted sales and marketing strategies to build on that connection, which improves lead generation and conversation and ultimately customer satisfaction. These efforts have resulted in improved absorption and an enhanced customer experience.”

The company expects to open 10 new communities and close out of 13 communities, which would result in 143 active selling communities as of June 30, 2019. In addition, the company anticipates delivering 53% to 58% of its 1,842 homes in backlog as of March 31, 2019 at an average sales price of $610,000.

The company expects its home building gross margin percentage to be approximately 17% for the second quarter. The company anticipates its SG&A expense as a percentage of homes sales revenue will be in a range of 12.5% to 13.5%. Lastly, the company expects its effective tax rate to be in the range of 25% to 26%.

For the full year, the company reiterates its previous guidance of delivering between 4,600 and 5,000 homes at an average sales price of $610,000 to $620,000. In addition, the company expects home building gross margin percentage to be in the range of 19% to 20% for the full year. The company expects full year SG&A expense as a percentage of homes sales revenue will be in a range of 11% to 12%.

Finally, the company expects its effective tax rate for the full year to be in the range of 25% to 26%.