The New Home Company Inc., Aliso Viejo, California (NYSE: NWHM) on Thursday reported a net loss of $4.6 million, or ($0.23) per diluted share, for its third quarter ended September 30, compared to net income of $2.5 million, or $0.12 per diluted share, for the 2018 third quarter. Analysts were expecting a gain of $0.02 per share.

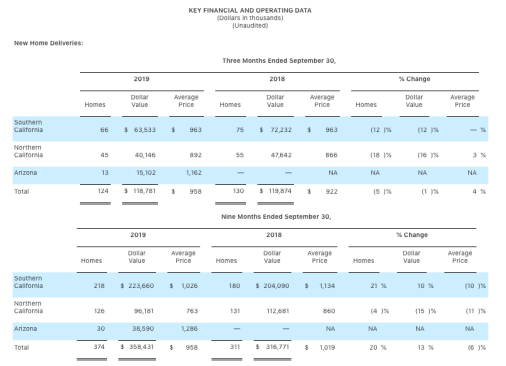

Home sales revenue for the 2019 third quarter was flat with the prior year at $118.8 million compared to $119.9 million in the year ago period. The slight decrease in home sales revenues was driven by 5% fewer deliveries, partially offset by a 4% increase in average selling price to $958,000 from $922,000 a year ago. The higher year-over-year average selling price was impacted by mix, particularly with the addition Arizona deliveries in 2019 where the average selling price exceeded $1 million for the third quarter.

Gross margin from home sales for the 2019 third quarter, which included $1.7 million in inventory impairment charges, was 9.5% as compared to 14.8% for the prior year period. The housing inventory impairment related to one community in Southern California that required more incentives than originally anticipated. Excluding home sales impairments, home sales gross margin was 11.0%* for the 2019 third quarter as compared to 14.8% in the prior year period. The 380 basis point decline was primarily due to higher incentives and interest costs, and a product mix shift. Adjusted homebuilding gross margin, which excludes home sales impairment charges and interest in cost of home sales, was 16.2% for the 2019 third quarter versus 18.4% in the prior year period.

The SG&A expense ratio as a percentage of home sales revenue for the 2019 third quarter was 11.1% as compared to 12.8% in the prior year period. The 170 basis point improvement in the SG&A rate was driven by reduced personnel expenses, more efficient marketing and advertising spend, and lower co-broker commissions as compared to prior year. These decreases were partially offset by a reduction in the amount of G&A expenses allocated to fee building cost of sales due to lower fee building activity and joint venture management fees.

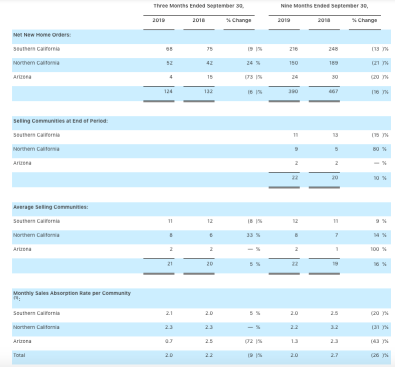

Net new home orders for the 2019 third quarter decreased 6% due to a slower monthly sales absorption rate, slightly offset by an increase in average selling communities. The monthly sales absorption rate was 2.0 for the 2019 third quarter compared to 2.2 for the prior year period. On a combined basis, the California absorption rate was flat as compared to the prior year, while the Arizona division was down largely due to a lack of inventory at the nearly sold-out Belmont community in Gilbert. The company ended the 2019 third quarter with 22 active communities, up from 20 at the end of the 2018 third quarter.

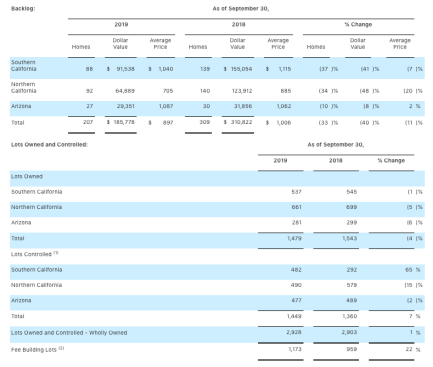

The dollar value of the company’s wholly owned backlog at the end of the 2019 third quarter was $185.8 million and totaled 207 homes compared to $310.8 million and 309 homes for the prior year period. The decrease in backlog units and dollar value was driven primarily by a lower beginning backlog coupled with a higher backlog conversion rate for the 2019 third quarter. The backlog conversion rate was 60% for the 2019 third quarter as compared to 42% in the year ago period. The increase in the 2019 conversion rate resulted from the company’s move to more affordably priced product, which generally has quicker build cycles, as well as the company’s success in selling and delivering a higher number of spec homes. The decline in backlog dollar value was also impacted, to a lesser extent, by an 11% decrease in average selling price as the company continues its transition to more affordable product.

During the 2019 third quarter, the company sold two land parcels in Northern California. The land sales generated $24.6 million in revenue for the 2019 third quarter compared to no land sale revenue for the 2018 third quarter. In connection with these land sales, the company recorded a $1.5 million loss. In addition, the company sold a third parcel of land in Northern California in October of 2019 for which it recorded a $1.9 million impairment charge in the 2019 third quarter. Proceeds from this third land sale totaled $16.6 million.

Fee building revenue for the 2019 third quarter was $22.3 million, compared to $39.2 million in the prior year period. The decrease in fee revenues was largely due to less construction activity in Irvine, California. Additionally, management fees from joint ventures and construction management fees from third parties, which are included in fee building revenue, decreased to $1.0 million for the 2019 third quarter as compared to $1.7 million for the 2018 third quarter. The lower fee building revenue and decrease in management fees, offset partially by a reduction in allocated G&A expenses, resulted in a fee building gross margin of $0.6 million for the 2019 third quarter versus $1.1 million in the prior year period.

The company’s share of joint venture loss for the 2019 third quarter was $63,000 as compared to $34,000 in income for the prior year period. At the end of 2019 and 2018 third quarters, the joint ventures had four and seven actively selling communities, respectively.

As of September 30, 2019, the company had real estate inventories totaling $506.3 million and owned or controlled 2,928 lots through its wholly owned operations (excluding fee building and joint venture lots), of which 1,449 lots, or 49% were controlled through option contracts. The company generated $39.7 million in operating cash flows during the 2019 third quarter and ended the quarter with $40.9 million in cash and cash equivalents and $327.4 million in debt, of which $18.0 million was outstanding under its $130 million revolving credit facility. At September 30, 2019, the company had a debt-to-capital ratio of 58.2% and a net debt-to-capital ratio of 54.9%.

“During the third quarter, we continued to make progress in our efforts to generate cash flow, deleverage our balance sheet and improve our SG&A efficiency,” said Larry Webb, executive chairman. “Cash flow from operations during the quarter totaled $39.7 million and contributed to a $48.0 million repayment of debt, resulting in a net debt-to-capital ratio of 54.9%, a 280 basis point improvement from the second quarter of 2019. Additionally, our SG&A ratio decreased 170 basis points from the prior year quarter thanks to lower selling and marketing expenses and a more streamlined cost structure.”

Webb continued, “We expect to make further improvements to our liquidity and debt leverage ratios in the fourth quarter, thanks in part to a $16.6 million land transaction that closed earlier this week. In addition, we anticipate our home building gross margins will start to improve on a sequential basis. With our leverage ratios trending lower and our gross margins trending higher, we feel we are in a position to enter 2020 with momentum.”

Leonard Miller, president and CEO, said “Home sales revenue for the 2019 third quarter of $118.8 million was essentially flat with the 2018 third quarter. However, for the 2019 year-to-date period, home sales revenue and home deliveries were up 13% and 20%, respectively, over the comparable 2018 period. The company’s 2019 third quarter monthly sales absorption rate was 2.0, driven primarily by our more affordable communities which had a monthly sales absorption rate of 3.3 during the third quarter. We continue to see the benefits of transitioning to lower price points, and this more affordable product represents the majority of the lots in our pipeline for upcoming community openings.”