The New Home Company Inc., Aliso Viejo, California (NYSE: NWHM) on Friday reported a net loss of $16.2 million, or $(0.80) per diluted share, for the 2018 fourth quarter ended Dec. 31. The loss included $30.0 million of pretax inventory and joint venture impairment charges. The results compare with net income for the 2017 fourth quarter of $10.5 million, or $0.50 per diluted share. Analysts were expecting a gain of $0.46 per share.

Total revenues for the 2018 fourth quarter were $229.7 million, compared to $324.1 million in the prior year period. The year-over-year decrease in net income was primarily attributable to a $29.1 million increase in inventory and joint venture impairments, a 33% decrease in home sales revenue, a 770 basis point decline in home sales gross margin percentage (270 basis point decline before impairments) and a 150 basis point increase in selling, general and administrative costs as a percentage of home sales revenue. These decreases were partially offset by a tax benefit for the 2018 fourth quarter.

Wholly Owned Projects

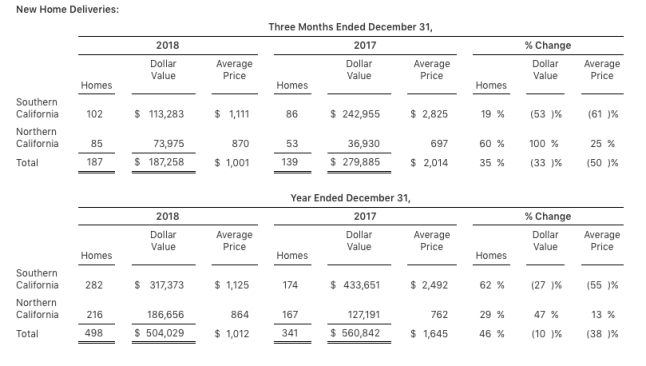

Home sales revenue for the 2018 fourth quarter decreased 33% to $187.3 million, compared to $279.9 million in the prior year period. The decrease in home sales revenue was driven largely by a 50% decline in average selling price to $1.0 million, which was partially offset by a 35% increase in deliveries. Home sales revenue was also negatively impacted by the delayed closing of several homes in backlog that were scheduled to be delivered in the period. The decrease in average selling price was most notable in Southern California where over half of deliveries were from more-affordable communities with base pricing of $750,000 or below. In addition, the 2017 fourth quarter average selling price was heavily influenced by deliveries from two Crystal Cove luxury communities in Newport Coast, CA where average selling prices exceeded $6.0 million.

Gross margin from home sales for the 2018 fourth quarter was 8.1% and included $10.0 million in inventory impairment charges related to two higher-priced communities in Southern California. Home sales gross margin for the 2017 fourth quarter was 15.8% and included inventory impairment charges of $0.9 million. Excluding inventory impairments, home sales gross margin was 13.5% for the 2018 fourth quarter as compared to 16.2% in the prior year period. The 270 basis point decline was primarily due to higher interest costs included in cost of home sales, and to a lesser extent, a product mix shift and slightly higher incentives. Additionally, the 2017 fourth quarter also benefited from an $0.8 million warranty reserve adjustment.

SG&A expense ratio as a percentage of home sales revenue for the 2018 fourth quarter was 9.9% versus 8.4% in the prior year period. The 150 basis point increase in the SG&A rate was primarily due to lower home sales revenue, higher co-broker commissions, and higher sales personnel and advertising costs associated with increased community count. Partially offsetting these year-over-year increases was decreased capitalized selling and marketing cost amortization due to the closeout of higher-end, luxury communities. G&A costs for the 2018 fourth quarter were also lower as compared to the prior year period primarily due to lower compensation-related expenses.

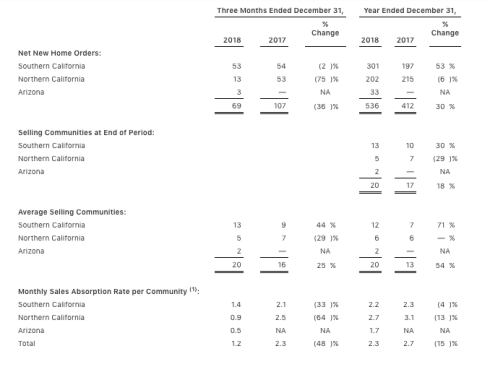

Net new home orders for the 2018 fourth quarter decreased 36% to 69 homes due to a slower monthly sales pace. The monthly sales absorption rate dropped to 1.2 sales per community compared to 2.3 for the year ago period. The company’s active selling community count was up 18% as of the end of the 2018 fourth quarter to 20 communities.

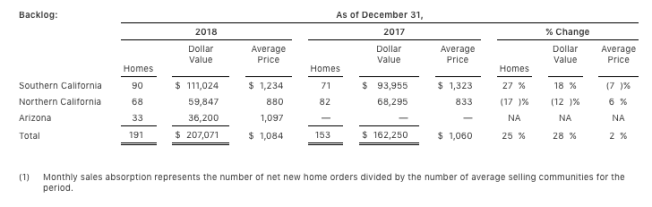

The dollar value of backlog at the end of the 2018 fourth quarter was $207.1 million and totaled 191 homes compared to $162.3 million and 153 homes in the prior year period. The increase in backlog dollar value resulted primarily from the 25% increase in homes in backlog, and to a lesser extent, a 2% higher average selling price.

Fee Building Projects

Fee building revenue for the 2018 fourth quarter was $42.4 million, compared to $44.2 million in the prior year period. Management fees from joint ventures and construction management fees from third parties increased to $1.6 million for the 2018 fourth quarter as compared to $1.2 million for the 2017 fourth quarter.

Unconsolidated Joint Ventures (JVs)

The company’s share of joint venture loss for the 2018 fourth quarter was $19.9 million, down from $0.3 million of income in the prior year period. Included in the company’s loss was a $20.0 million impairment charge related to an investment in a land development joint venture in Northern California. The impairment was primarily the result of lower anticipated land sales revenue as well as a decision to not incorporate a potential home building component within the existing land development joint venture at this time.

Joint venture net loss totaled $28.3 million, compared to net income of $0.6 million in the prior year period. Joint venture home sales revenue for the 2018 fourth quarter totaled $52.8 million, compared to $38.1 million in the prior year period, while joint venture land sales revenue totaled $7.5 million for the 2018 fourth quarter, compared to $1.7 million in the prior year period.

At the end of both the 2018 and 2017 fourth quarters, joint ventures had seven actively selling communities. Net new home orders from joint ventures for the 2018 fourth quarter decreased 32% to 23 homes. The dollar value of homes in backlog from joint ventures at the end of the 2018 fourth quarter was $66.9 million from 76 homes compared to $66.6 million from 80 homes at the end of the 2017 fourth quarter.

For the full year 2018, the company reported a net loss of $14.2 million, or $(0.69) per diluted share. The company’s net income for 2017 was $17.2 million, or $0.82 per diluted share.

Total revenues for the year ended December 31, 2018 were $667.6 million compared to $751.2 million for the prior year. Home building revenue declined to $504.0 million primarily from a 38% decrease in the average selling price of homes due to a strategic shift to more affordably priced homes in 2018, partially offset by a 46% increase in the number of homes delivered during the year. The year-over-year decrease in net income was primarily attributable to a $27.8 million increase in inventory and joint venture impairment charges, a 380 basis point decline in home sales margin (220 basis point decline before impairments*), an 11% decrease in total revenues, and a 180 basis point increase in selling, general and administrative expenses as a percentage of home sales revenue. These items were partially offset by the income tax benefit for 2018.

As of December 31, 2018, the Company had real estate inventories totaling $566.3 million and owned or controlled 2,812 lots through its wholly owned operations (excluding fee building and joint venture lots), of which 1,145 lots, or 41%, were controlled through option contracts. The company ended the 2018 fourth quarter with $42.3 million in cash and cash equivalents and $387.6 million in debt, of which $67.5 million was outstanding under its $200 million revolving credit facility. As of December 31, 2018, the company had a debt-to-capital ratio of 61.8% and a net debt-to-capital ratio of 59.0%.

“In 2018, we took another step forward in implementing our strategy to reach more buyers through more affordably priced communities as evidenced by a 46% increase in deliveries compared to 2017 and a 38% reduction in the average selling price of homes delivered,” said Larry Webb, chairman and CEO. “However, the fourth quarter of 2018 proved to be a challenge as potential buyers in our markets exercised a high degree of caution during what is already a seasonally slow period, which resulted in a slower absorption rate. In addition, we experienced some construction delays at a few communities, most notably at our multifamily condominium community in Playa Vista, which negatively impacted our fourth quarter revenues. While we continue to have confidence in the fundamental drivers of our business and strategy, we acknowledge the operational challenges a slowing housing market poses and have adjusted our outlook accordingly.”

Webb continued, “As a result of this revised outlook, we took impairment charges at two higher-priced communities in Southern California and one land development joint venture in Northern California. We believe these actions were necessary in light of the current demand environment and should allow us to turn through these communities at a more accelerated rate, redeploy capital within our existing or new markets and generate cash flow more quickly.”

Webb concluded. “We continue to be positive about the long-term outlook for our markets and our company, and we are taking steps to right-size our business and fortify our balance sheet. We anticipate that these initiatives will lead to a leaner cost structure, reduce debt leverage over time and improve shareholder returns.”