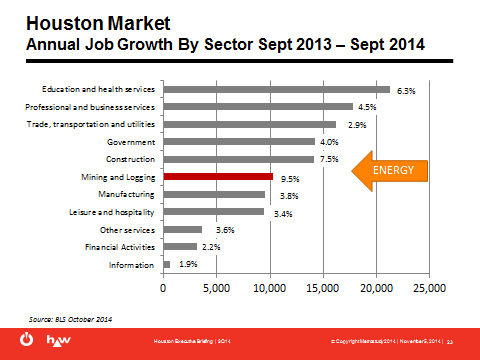

There’s no question that there is a strong correlation between home prices and housing starts in Houston. A significant share of our economy is still based on oil, and energy has been the fastest growing employment sector this year.

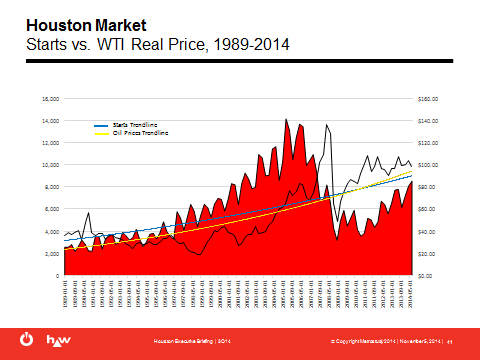

Historically there is a pretty strong correlation between starts and oil prices, looking back to 1980. Take a look:

Oil prices have fallen significantly in the last 90 days, falling to $75, the lowest price since 2011. There is some belief that the price drop may be geopolitical rather than economic as Saudi Arabia may be trying to squeeze its OPEC competitors and Russia, most of whom require oil above $100/bbl to be profitable. Even if true, US oil production is up almost 50% since 2011, and we see evidence of weakened demand from China and India. It’s likely a result of a combination of these factors.

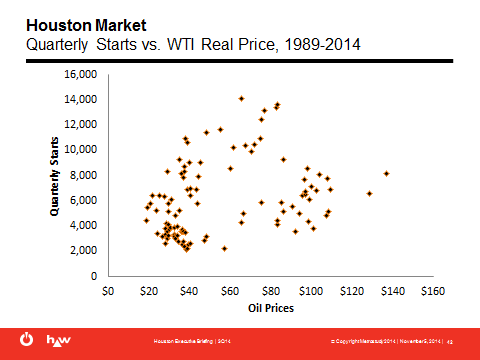

What does this mean for Houston? We’ve plotted quarterly housing starts versus real oil prices from 1980 through Q3 of 2014, below.

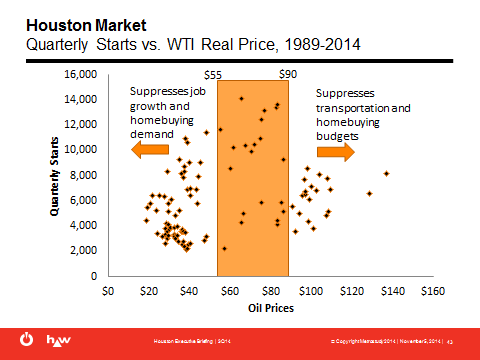

The conclusion we draw is as follows: there is a “sweet spot” between $55 and $90/bbl that produces the highest demand for housing in the Houston market. Above $90 it appears that high energy prices dampen demand for housing because of the squeeze on consumer budgets for housing and, in a market the size of Houston, transportation. Below $55 it appears that demand is lessened because of weaker job growth. The Energy Information Administration’s pricing forecast for oil in 2015 is $91, and Saudi Aramco needs oil at about $93 to be profitable. We expect oil prices to rise slightly to that level through the quarter and remain there on average through the balance of 2015.

What does this mean for Houston? We expect job growth, presently 112,900 (+4.3 percent), to slow and to place pressure on upward prices. The resulting declines may make some newer developments less favorable and place them under financial pressure. Overall, however, the fall in oil prices will be beneficial because:

1. Declining energy employment, particularly in the downstream sector, will relieve pressure on labor shortages for the construction industry, reducing one of our market’s key cost drivers.

2. Lower gas prices will favor development in more remote markets, opening up lower cost sources of land and encouraging development of lots at the lower range of the market; about one third of new home buyers in Houston are in the under $200K price band, a segment increasing difficult to meet.

3. Lower energy prices may assist improving economies in other markets which should help the share of Houston’s economy dependent on national economic performance.

4. Houston’s energy economy includes upstream, midstream and downstream energy. Downstream energy, exploration and production, will likely suffer from extended low energy prices. The two other sectors, midstream (pipelines) and upstream (petrochemical manufacturing) will likely improve as lower prices encourage more consumption nationwide requiring more oil/refined products to be transported (midstream) or manufacturing sees lower costs for feedstock (upstream).

Houston’s economy remains heavily dependent on the energy

industry, both in direct employment and supporting economic activities

indirectly tied to it. It’s important to remember that energy projects

are generally significant, long-term investments that are not very sensitive to

daily or weekly price movements and the long-term worldwide trend for oil

consumption still points upward. In the short to midterm timeframe, the

recent declines in energy costs should actually prove to be a positive factor

in Houston’s housing market, not a negative one.