Our October collection of new home and building lot demand in Metrostudy’s 36 markets indicates that typical seasonal decline continues in the majority of markets, but inventory in the pipeline appears stable, and the pace of starts continues to climb. Despite the expected seasonal decline, 66% of regional directors recorded a higher score for new-home demand in October 2015 than in October 2014, and only eight markets decreased year over year. Houston, Raleigh-Durham, San Diego, and Southern California were among the eight markets reporting a decrease, a sign that other markets are now catching up in the recovery given that those four markets have been in the top half of our scale for the past year, while other markets have wavered at the mid-point.

Similar to the notion that seasonal slowdown will be a passing storm weathered by spring, the Conference Board’s Consumer Confidence Index fell to 97.6 in October following a reading of 102.6 in September. However, the share of respondents planning to buy a home within six months (which puts us at the start of spring selling season) rose 1.5% month over month to 6.3%—a good sign for the future.

The gains in new-home demand scores year over year are also validated by a rise in residential construction stocks. As of Oct. 30, NVR (NVR), D.R. Horton (DHI), and Lennar (LEN) stocks have risen 35.54%, 28.21%, and 14.40%, respectively. While the winter likely will bring lower demand scores, we predict that year-over-year growth will continue, given that the housing market as a whole is in a much better spot than it was a year ago.

Don’t Call it a Comeback?

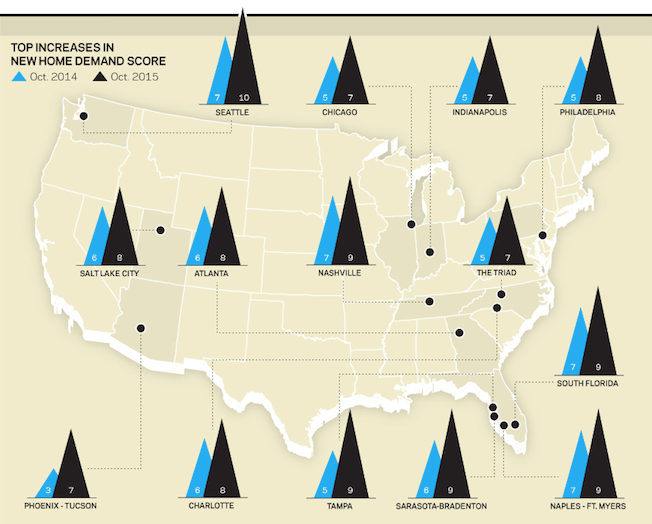

The Phoenix-Tucson market has made the biggest year-over-year gains in our new home demand index, jumping from a score of 3 in October 2014 to a 7 this October. Annual starts have increased 18%, but labor shortages are causing build times to extend from three months to six months (even without bad weather). According to regional director Rachel Cantor, this has been the main cause of an 8% decrease in annual closings, and builders are concerned about hitting their targets.

Builders in the market seem to be preparing for high demand for new homes in the spring, however, and have “loosened up the reins slightly on sales to ensure they’re getting the permits they need,” Cantor says. Some builders are starting to move into the active adult space, and under construction units are at the highest point seen in the past seven years. Phoenix’s performance in spring will be one to watch if labor issues ease.

The Philadelphia market also made a big jump—from 5 to 8—for new-home demand year over year, and starts have increased 5.6% since October 2014. The Philadelphia market primarily is held back due to lot supply constraints, says regional director Quita Syhapanya. “Demand for new homes is strongest in specific submarkets with strong school districts,” he reports. “Most of the best school districts have very minimal available inventory, both in new construction and resale.” Because the primary driver for home buyers in Philly is access to good schools, finished lots in good school districts are a golden ticket for builders. However, months supply of vacant developed lots was down to single digits as of August 2015. Builders in Philadelphia will need to get creative to make the most of available land in those locations if they are able to secure it.

Although Seattle was never in limbo, new-home demand in that region has increased significantly year over year as well, jumping from a score of 7 to 10. “Buildable land and finished lots are a premium these days,” says Seattle regional director Todd Britsch. “Builders are calculating in future appreciation, which has the potential to be very painful for them in the coming two years.

Trouble in Texas

Houston and Dallas-Fort Worth have been markets to beat during the recovery, but commentary from our regional directors indicate that they’re still trying to catch up after a spring selling season riddled with horrible weather. Although starts in Dallas-Fort Worth have surged in the third quarter (and jumped 31.4% year over year), builders’ efforts to catch up are being throttled by labor constraints and have caused build times to stretch to eight to nine months. Labor issues (coupled with dragging lot delivery) point to price hikes, but a 2.6 month supply of existing homes will leave buyers unwilling to wait with few options.

“Based on the prices of lots currently under development, home prices will skyrocket next year,” predicts Dallas-Fort Worth regional director Paige Shipp. “There is concern that buyers will push back or not be able to afford the next generation pricing.”

In Houston, starts are down 10% quarter over quarter, but only 1% year over year. Unlike Dallas-Fort Worth, builders don’t seem to be trying to make up for lost development time during spring, and “lot demand has fallen in spite of historically low inventory levels,” Shipp says. Houston regional director Scott Davis reports that with the projected increase in oil prices in 2017, “Houston faces a return to the supply challenged environment of 2012-2014 by the middle of the year.” This creates a silver lining for buyers who have been blocked out by high home prices due to historically low new-home inventory, in that Davis expects there will be a brief window for buyers to purchase discounted homes as builders try to move the inventory they have off the books.

Despite the strong gains in consumer demand year over year across the board, many builders are scrambling to make up lost time due to weather conditions, labor issues, or lot constraints. Housing is improving, but gearing up for the 2016 spring selling season will be an expensive feat for builders, especially in markets like Houston.