April may be the cruelest month in some people’s book, but it’s when U.S. home building activity kicks into its highest gear for the following 90 days.

Naturally, costs–or rather, rising costs–are a focus, a fanatic one.

Because work in process pace picks up, expenses snowball, and this year, in light of higher stakes all around in bringing price points down, accepting tighter margins, and trying to capture profits back by driving volume through the system, builders need a lot of things to go their way.

A monthly materials cost analysis of Bureau of Labor Statistics producer price trends from the National Association of Home Builders caught track of a seasonal supply-demand fueled uptick in material input costs last week. David Logan, NAHB Director of Tax and Trade Policy Analysis, writes:

Overall, the price of goods used in residential construction increased 0.8% in February (not seasonally adjusted)–the first increase in five months. Softwood lumber (+2.3%) and OSB (+4.3%) offset the large decline in prices paid for gypsum products.

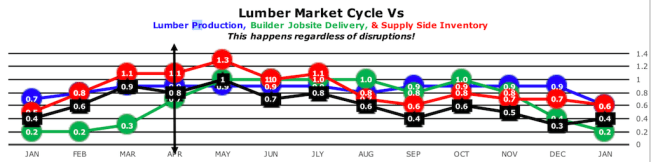

Lumber guru, Matt Layman, waxes eloquent, that a rite of Spring, intensely heavy demand, particularly for softwood framing lumber. His latest Layman’s Lumber Market Briefing, for March 28, notes.

“Builders’ and contractors’ peak demand period is April, May and June. That is a function of the amount of daylight to work with, the most desirable weather conditions and uninterrupted production momentum.

In between the constant mill production and the seasonal surges in building activity, our lumber market is seemingly like a Mexican jumping bean, popping up and down amid wicked volatility. Random as it may seem, the “when” component of price movements is very predictable.

April has constant production, increased jobsite demand, and the supply chain selling and replacing inventory. The largest impact on price movement is just-in-time buyers who respond to sales rather than prepare for increased periods of demand.”

Of course, materials price volatility and a seasonal spike are only the half of what worries builders. It’s the labor costs–thanks to on-going, chronic, undersupply of capacity among skilled slab, foundation, framing, roofing, and rough-in trades–that are the major source of expense anxiety. This kicks up a notch or two as new home communities aiming to court younger, first-time, earlier-career, less-well-financially-established buyers, tend to be farther flung distances from operating hubs, involving more windshield time, and more severe consequences if operations, scheduling, task completion, etc. don’t go like clockwork.

A monthly construction cost report, the IHS Markit PEG Engineering and Construction Cost Index, registered 60.4 this month, a spike upward from February’s reading of 55.3. Here’s the rub on labor costs:

The sub-index for current subcontractor labor costs came in at 59.7, up from 56.3 in February. Labor costs rose in all regions of the United States and stayed flat in both Western and Eastern Canada. “U.S. construction labor markets remain incredibly tight and shortages are widespread – even firms that are willing to raise wages and offer bonuses are having trouble finding experienced workers,” said Emily Crowley, principal economist, Pricing and Purchasing, IHS Markit. “A hollowing-out of the U.S. construction workforce during the great recession means there are fewer mid-career workers available to replace retirees. The recent uptick in oil and gas activity is also creating additional strain on labor markets on the U.S. Gulf Coast.”

Of course, tactical focus on costs and expense management is simply operating a business as needs to happen for any going concern. The real challenge is setting strategic priority around two areas, keeping close customers’ experience, and developing workflow process and technology solutions to seize greater control–albeit in the five-year horizon–of construction labor costs.