Curious to look at the math of how $55 billion in annual building materials expenses roll up and break down in the new-home market, account for a quarter of a home’s price tage, and add up to $105 billion in remodeling materials and products each year?

A new Bank of America Merrill Lynch report–“Who Builds the House”–subjects both the new residential and remodeling market places to a fascinating market “sizing” research exercise, aggregating and averaging data in such a way as to show a model for materials and products input costs. Although America’s thousands of home builders don’t buy, build, or model their businesses on averages, estimates, or aggregates, the analysis of 14 major product and materials component groups is helpful in revealing why all the fuss about price inflation pressures as builders work to subtract costs and offer lower-priced home models.

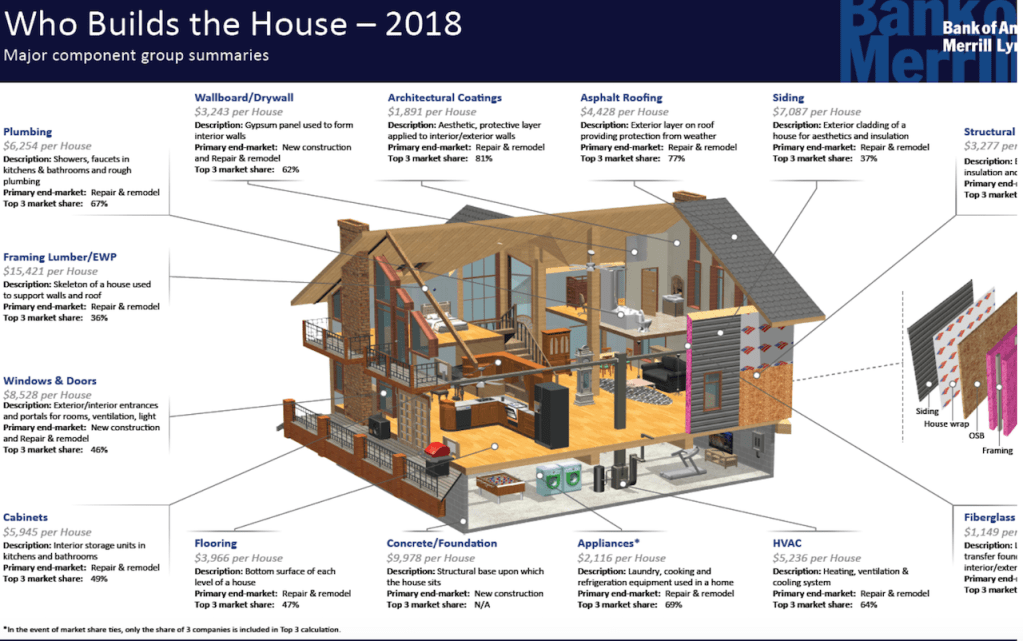

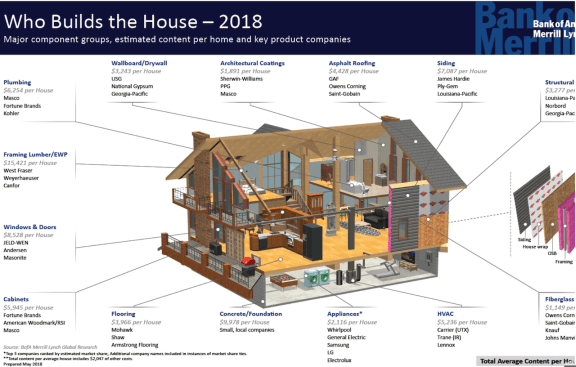

The fascinating snapshot schematic from the report looks like this:

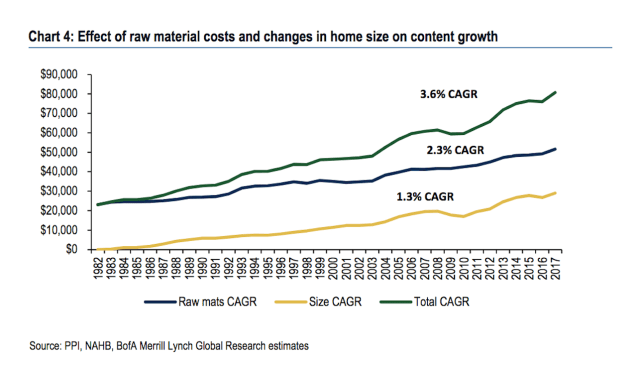

We estimate that the value of content in an average US single-family new home has grown at a compounded annual growth rate (CAGR) of 3.6% from $23,073 in 1982 to $80,566 in 2017. Our $80,566 estimate includes $2,047 of content attributable to an “other” category, which is an aggregate of sundry items outside of the 14 major groups. Materials constitute roughly 25% of the sale price of a new house, with the 2017 median sale price reaching $321,000 according to the US Census Bureau. This foots fairly well with our $80,566 content estimate ($80,566/25% = $322,264).

Further, the report sizes market share for the building products and materials supplier leaders in each of its 14 separate component categories, essentially diagramming market leaders in each part of the a home’s construction. All in, the report notes that the top three players in each of the 14 products and materials components of a home, own 60% or more of the market, and that consolidation continues.

We estimate an overall opportunity for building products content (excluding labor) in the US new single-family home construction market of roughly $55bn. We derive our $55bn estimate by multiplying the residential new construction exposure of each component group by its total addressable market and aggregating the results. This approach is backstopped by multiplying our estimated dollar content per home of $80,566 by 2017 new home sales of 614K and by 2017 single family starts of 851K, which implies a residential new construction market range of $49bn-$69bn.

Again, nobody builds to an average or aggregate, so for different geographical markets, different square footages, different customer segment specs, different national and local deals and installation nodes, these figures can become far from precise when it comes to applying them to specific projects.

Here’s the way the analysis takes on the trajectory of building materials and product input expense as a historical trend:

Based on 18 distinct producer price indices (including “other” category), we estimate that the raw material content in an average single-family home increased from roughly $23,073 in 1982 (base year, index=100) to $51,523 in 2017, representing a CAGR of approximately 2.3%. In addition, the average square footage of floor area in a new single-family home increased at a 1.3% CAGR from 1,710 to 2,674 over the same period. Given that 1982 was the base year for this analysis, the size impact rose from $0/home in 1982 to $29,044/home in 2017. For consistency, we employ the same size factor (current year average square footage/1982 average square footage) for each component group. The sum of the raw material and square footage inputs equate to our total content per home estimate in each year. Therefore, we estimate that total content in an average single-family home increased from $23,073 in 1982 to $80,566 in 2017.

Still, where the report goes beyond these benchmarks and drills into trends driving costs and pricing for each of the 14 component groups, the analysis becomes both rigorous and predictive.

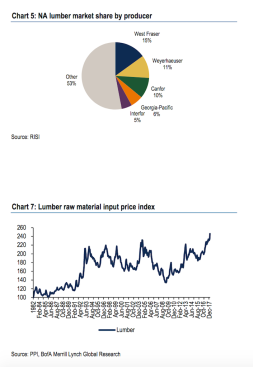

For instance, here’s how the Bank of America Merrill Lynch analysis looks at the framing lumber component, estimated at an average of $15,421 per new home.

Pricing for lumber has trended higher since US producers filed a trade case against Canadian producers in Nov. 2016, which culminated in combined antidumping and countervailing duties of 20.23% being applied to Canadian softwood lumber exports to the US. Coupled with growth in housing, this helped tighten the market as imports from Canada declined (to 14 billion board feet in 2017 from around 16 billion board feet in 2016) and more than offset the 1 billion board feet of new supply that entered the market. As for EWP, pricing tends to follow lumber and OSB prices which are rising. While this will likely drive higher costs for EWP producers, it could also provide support for increased EWP pricing given solid supply/demand.

As the new home unit growth recovery continues through 2018 and into 2019, it’s more and more evident that upward pressure on prices of materials, land, and labor–each hitting home builders’ investment and operations structures at different time periods–are a risk to making money in the business, especially for smaller companies that pay more for capital.

National Association of Home Builders economist David Logan notes here that the latest Producer Price Index data from the Bureau of Labor Statistics indicate builders are paying 4% more on construction input costs now than a year earlier.

Oriented strand board (OSB) led price increases, up 7.1% since March (not seasonally adjusted). The indexes for ready-mix concrete (+0.6%), gypsum products (+0.1%), and the aggregate index for goods inputs to residential construction (+0.9%) also edged higher. Softwood lumber prices fell 1.9% month-over-month, according to the report.

The 0.9% increase in prices paid for residential construction inputs (goods) was the fourth consecutive monthly increase. The index has risen 3.9% over the first four months of 2018 and sits 6.2% higher than it did in April 2017.

Looking from the outside in at the data, many conclude that 2018 will be a good year for builders, and lead into another good year in 2019.

Many of those builders, on the inside looking out, might reply: “Define good.”