One consequence of the reduced level of single-family construction since the Great Recession has been an aging of the country’s housing stock. According to NAHB analysis of the most recent edition of the American Housing Survey (2013), the typical owner-occupied home is 37 years old. This represents a significant increase since 1993, when the typical home was 27 years old.

Looking at the underlying distribution, four out of 10 homes in the U.S. were built before 1970. The aging impact is clear: The share of homes that are 35 years or older is 57%, compared with 41% in 1993 and 46% in 2003. Currently, homes six years or younger make up just 2% of the owner-occupied housing stock, compared with 6% in both 1993 and 2003.

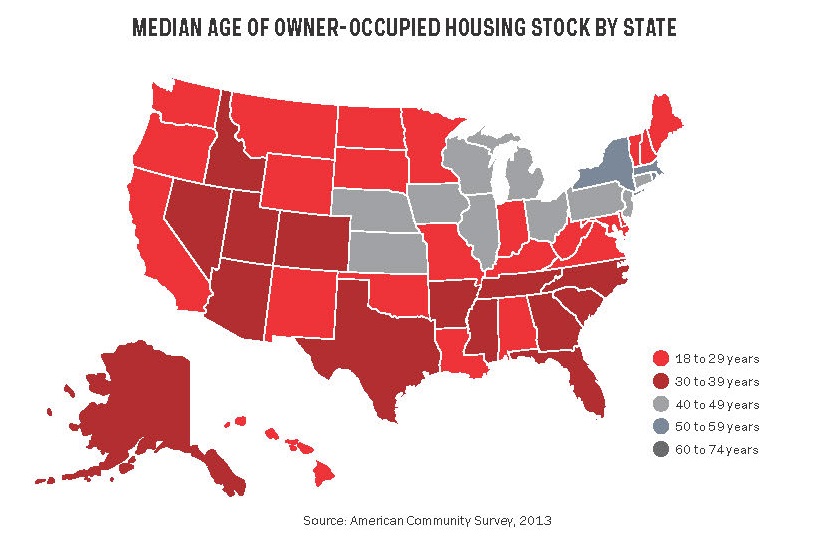

There is significant geographic variation with respect to the age of homes, with clear regional clustering. New York has the oldest homes among states, with a median age of 55 years. Massachusetts has a median age of 52. And the District of Columbia, as a concentrated urban area, has a median age of 74. Younger homes were located in the West and the South, in areas with more robust population growth. The median age of owner-occupied homes in Nevada was just 18, with Arizona at 23.

The aging housing stock means additional demand for home building in the years ahead. Older homes must be replaced. NAHB estimates that tear-down construction housing starts totaled 55,000 in 2015, making up just over 7% of all single-family construction. Older housing also means more remodeling activity as demand rises for improvements like aging in place and energy efficiency. An aging housing stock also offers opportunities for multifamily builders to add density and new housing with amenities in aging markets.

The challenge for businesses and policymakers is that lower income households tend to own the homes most in need of improvement. In 2013, the average income of those who owned homes built after 2010 was more than $110,000, compared with the slightly higher than $81,000 average household income for owners of homes built before 1969.

Connecting the underlying need for residential improvement and construction with spending power and financing is yet another illustration of the importance of ensuring a healthy housing finance system. Whether redevelopment means accessing residential acquisition, development and construction financing for builders, home equity loans for homeowners with tax-deductible interest, or tax-exempt bond and tax credits for multifamily rehabilitation, addressing an aging housing stock in the years ahead will be a significant source of economic growth.