Now comes the interesting part.

Lennar ceo Stuart Miller and president Rick Beckwit broached the idea of a strategic combination with CalAtlantic’s biggest shareholder MatlinPatter Global Advisors ceo David Matlin in New York on the first day of summer last year.

It would be past the first day of Fall in 2017, after several proposals, a lot of tepid posturing and coy shows of interest from executives and board members of CalAtlantic, before an earnest negotiation began. And it would take most of the month of October–proposals and counterproposals flashing back and forth between the New York offices of Lennar’s Citi representatives and CalAtlantic’s J.P. Morgan bankers–to arrive at a definitive merger agreement on Oct. 29th, that led eventually to yesterday’s closing announcement.

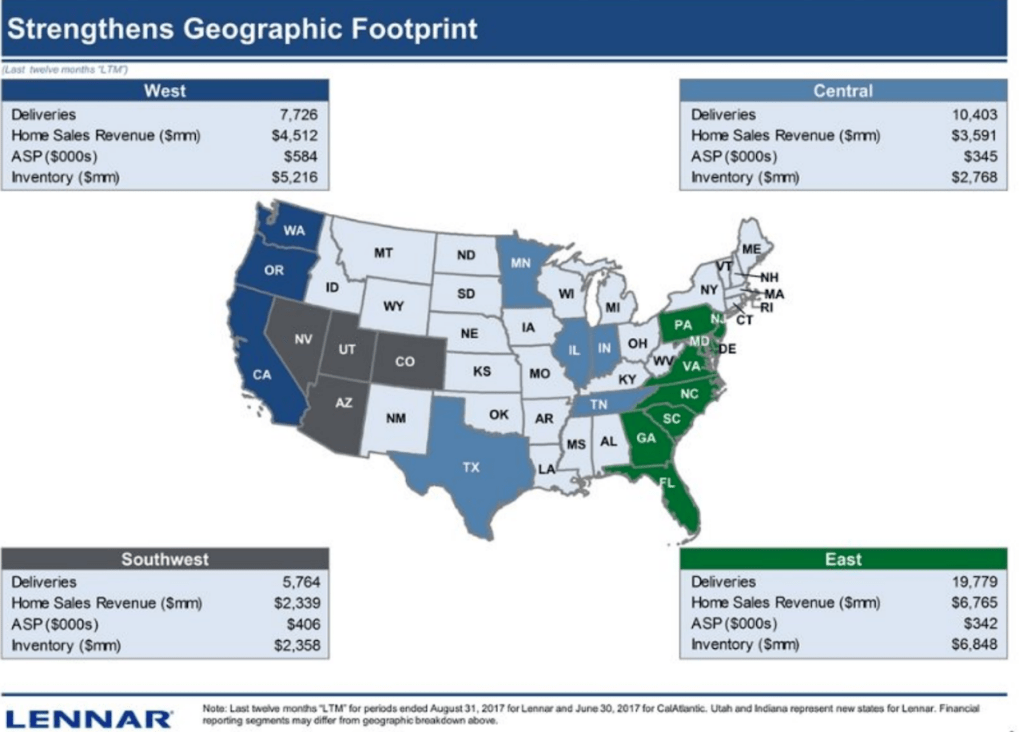

Today, home building officially has a new No. 1 company by sales volume, combining the heft of the No. 2 and the No. 5 ranked U.S. builders as a 43,700-home, $17.2 billion enterprise (in 2016 figures).

Today, many of those who worked to build CalAtlantic’s value–many of whom were Ryland Homes and Standard Pacific team members–face a question mark as to their immediate future. At every level, from the communities to the headquarters offices, it will be Lennar decision-makers who’ll determine whether there’s a place or not in the new combined enterprise, which now controls 250,000 homesites and 1,300 active communities across 21 states.

Given the widening and deepening need for talent at all levels of home building and residential development, the ones who don’t find a place in Lennar’s plans moving forward are likely to have options to work elsewhere in the field.

As reasons for paying $1.16 billion in cash, and Lennar stock valued at $4.9 billion, $3.9 billion in debt, as well as $170 million in merger-related costs, Miller and Beckwit led a team that offered the Lennar board of directors 12 key benefits.

- The merged companies would create a better platform for enhanced shareholder value.

- The Merger is expected to be accretive to Lennar’s earnings per share by approximately $0.04 per share in fiscal year 2018, without taking account of transaction costs, and to be accretive by approximately $0.68 per share to the earnings per share Lennar anticipated generating in fiscal 2019 under a base plan that would have included effects of share repurchases.

- The Merger will give Lennar significant concentrated local market share, with a top three market share position in 26 of the 30 fastest growing metropolitan statistical areas, which will enable Lennar to have greater access to land and labor, leading to greater efficiencies and opportunities.

- The Merger will increase the areas where Lennar can become the builder of choice for subcontractors and suppliers, with resulting reductions in cycle times, increases in inventory turns, and better access to skilled labor.

- Acquiring homebuilding operations in markets where we have local market and product knowledge will assist with a smooth integration.

- The Merger is expected to result in approximately $100 million of cost savings in fiscal year 2018 and $365 million per year of cost savings in fiscal year 2019 and subsequent years, as a result of reduced general and administrative costs and reduced homebuilding costs. The ability to achieve these cost savings will result in part from the fact that Lennar and CalAtlantic have compatible product strategies.

- Acquiring existing communities with known absorption rates provides a foundation for growth in land constrained markets.

- The Merger will expand synergies with non-homebuilding aspects of Lennar’s activities, such as residential mortgages and other financial services and technology related partnerships and initiatives.

- Although the Merger will require Lennar to incur or assume a substantial amount of additional debt, cash flow expected to be generated by the combined company is anticipated to enable Lennar by the end of fiscal year 2019 to reduce its indebtedness to the point where the ratio of its debt to total capital and the ratio of its net debt to total capital will be 36.0% and 33.3%, respectively, compared with 40.0% and 37.3%, respectively, which were expected to be the ratios at November 30, 2017 (which was before giving effect to the Merger or indebtedness incurred in anticipation of the Merger).

- Cash flow expected to be generated by the combined company will, in addition to enabling Lennar substantially to reduce its debt, enable Lennar to engage in a stock repurchase program, with a resulting increase in earnings per share.

- Lennar’s management demonstrated following the February 2017 acquisition of WCI Communities, Inc., and has demonstrated after other acquisitions, that applying Lennar’s homebuilding techniques to properties accumulated by other homebuilders can accomplish cost savings and increase gross margins. The combined company is expected to have the type of above average gross margins that have been consistently achieved by Lennar for a number of years.

- Acquiring an existing homebuilding company gives Lennar access to already entitled land that can be developed without the delay involved in obtaining entitlements.

Three striking take-aways jump out at us that may shed light on whether and how even more strategic consolidation might play out, particularly as large enterprises take stock of immediate windfalls from corporate tax rate cuts and look ahead at rising costs of debt.

A couple of these observations have to do with the timing of the deal.

- One, however, illuminates an almost contrarian approach to mergers and acquisitions motivations. Lennar, of course, wanted access to CalAtlantic’s land asset above all. Many acquirers would perform diligence on a target and identify opportunity areas to eliminate expense in the acquired company as a key lever to achieving improved performance post-integration. In Lennar, we see an organization that first identified big cost-savings opportunity in its own system–through applying technology-fueled data and analytics to its marketing and sales workflows, which captured $100 million in expense in Lennar itself–as one of the keys to its integration strategy post-combination. This way, having just taken the plunge in its own enterprise, it can iterate the systems and processes across the new portfolio with greater precision and effectiveness and, at the same time, an immediate savings in costs.

- Second, the Lennar-CalAtlantic footprint gives the new entity deeper scale in more markets, and allows Lennar to leverage its Everything’s Included product streamlining and process to reduce overheads, reduce direct cost variability, and gain margins even as it accelerates its inventory turns and secures local labor crews with more predictable, more geographically efficient work-streams.

- Thirdly, by adding volume and market share in many of the markets and submarkets it had already been operating in, Lennar, can move forward with pilots it plans for vertical integration–namely offsite panel, roof truss, and flooring plants–it has been contemplating–absorbing the upfront investment in such facilities with greater volume of its own unit sales.

The bold absorption of two of the U.S.’s publicly-traded entities into what is now America’s largest home building enterprise begs the question: what will D.R. Horton–which has long prided itself as America’s biggest home builder–do next?

Also, when investors now look at the other top 10 public home building companies, they have to be thinking that there’s at least equal opportunity to take out hundreds of millions of dollars of costs out of almost every one of them to size capacity and overheads to the current market opportunity.

So, now comes the interesting part; not just for Lennar, but for every other public company, which is either an acquirer, an acquisition target, or both.