One of the English language’s tiniest, 2-letter words contains countless multitudes of meanings. As coronavirus calculus courses through the economy at a rate blistering enough to make even a supercomputer smoke, the word is unavoidable.

If.

The word, the ultimate conditional, admits unknowns. It acknowledges uncertainties bigger, more plentiful, and more consequential than math, or scenarios, or even the farther stretches of imagination can map right now. We humans tend to be humbled by its meaning–ever unappreciative of risk it may plainly suggest, ever expectant of reward it may offer.

Right now, as the pathogen shows up in more and more dispersed corners of the globe, the word could turn a 10-year expansion into a one- or two-quarter economic prolapse. In a flash, it could derail, at least temporarily, hiring trends, wages, expectations, and sentiment, as companies await stabilization in their supply chains, leisure travel, consumption, etc., and resume business as usual once COVID-19’s fallout is contained, whenever that may be.

“Admit it,” writes New York Times columnist Farhad Manjoo, “You don’t know what will happen next.”

We can only say, “if, this happens,” or “if this doesn’t happen.”

Meanwhile, that word–if–a very fragile balance between appropriate preparedness and panic, is flexing its outsized muscle across the global markets, isolating on a smaller and smaller segment of investment havens. Is new home construction and development one of them?

On top of all that, it’s late-cycle roulette time for privately-capitalized builders. A dozen or more would-be suitors with deep pockets and an array of enticing scenarios for operators who want to stay in and grow, or get out while the getting’s good.

Against a current backdrop of low cost of debt, high public company stock prices, low unemployment, strong order growth, strong demographics, home price appreciation, and low, low inventory, word on the street in home builder-land to private home builders is this:

“If you’re thinking of possibly selling your relatively strong privately-capitalized home building operation and its land assets in the next few years, now may be the moment not to miss.”

Here’s why.

In home building these days, one word is worth a thousand pictures. That word is Land.

One doesn’t have to stray far for an analogy to picture the dynamics frothing up in the home building mergers and acquisition market right now.

It’s roughly like … well, trying to buy a home right now.

In this analogy, single-market and smallish regional home builders are the home sellers, and big builders–publics, a couple of multi-regional private enterprises, Japan-, China-, and Canada-based global firms, and Clayton Properties Group–are like the buyers.

There’s lots of buyers for every seller, especially the “good” sellers, the good companies who operate–independently of public or foreign-owned capital in our Local Leaders line-up.

Buyers have a machine to feed, cadenced now only by labor capacity constraint, and they’re hell-bent on not only feeding it, but gaining visibility into how they’ll continue to feed it for as long as the current run holds its momentum.

But what’s momentum for public companies whose principals don’t have their names on loans with personal guarantees has begun to feel a bit like motion sickness for those who do.

“We’re looking at 2020 and 2021 as great years for us,” says a privately-held home building company principal in one of the nation’s hottest new-home markets. “It’s when we look at 2022, and we have to start buying lots for that year and the year ahead that things go haywire. We can’t pencil lots at the kinds of prices public builders are paying for land; we can’t assume price appreciation at current levels is going to continue.”

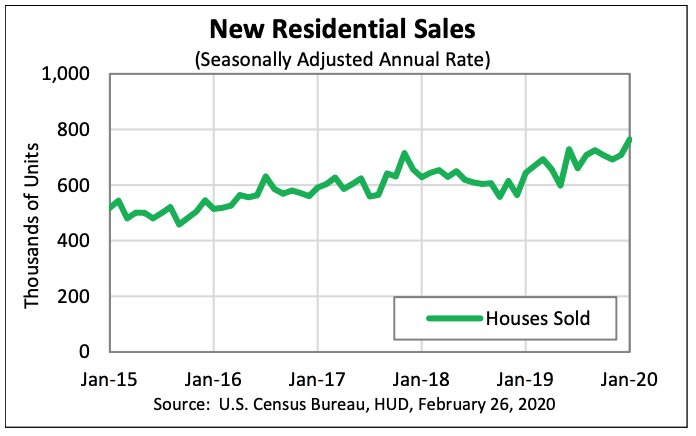

The past 60 days of new home sales and new home pending sales–virtually the trump card motivator for land acquisition urgency–has been record-breaking, supported by pent-up demand, structural demographic trajectories, dirt-cheap mortgage interest rates, the job market, consumer sentiment, etc.

Now here we go with the conditional surrounding every sector’s market outlook under the sun.

If coronavirus doesn’t continue to wreak havoc among populations here and abroad, to the point where markets seize up and impact first, second, and third-quarter GDP to the negative, M&A deal flow is setting up to be very active over the next 12 to 18 months.

Maybe as active as it was two or three years ago.

That’s because strategic publics–able to draw on cheap debt and leverage high stock price valuations–are fully back among the buyer set.

The simple fact is, nearly every player needs more land, and for privately-capitalized players whose capital financing often redounds to personally guaranteed loans, investor deals, and their own money, this is where things get painful.

“I have a tough choice,” says the principal mentioned above. “I either take on a great deal more risk by reloading my land supply now at every high prices, and taking out the loans to do that, or I accept that I won’t grow the company as fast as I planned.”

Scarcity of lots beyond 2020 and 2021 is a serious matter. For publics, however, they can go out and buy private companies to add to their lot pipelines in addition to adding the incremental in-year volume.

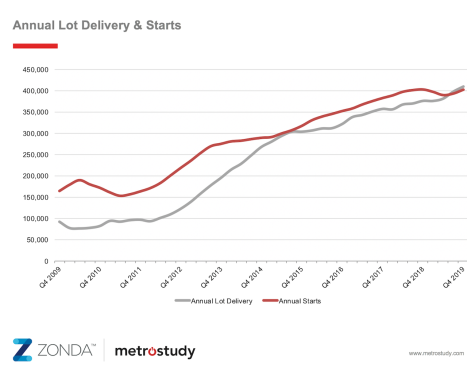

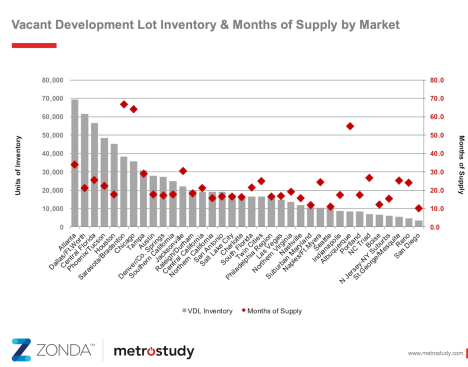

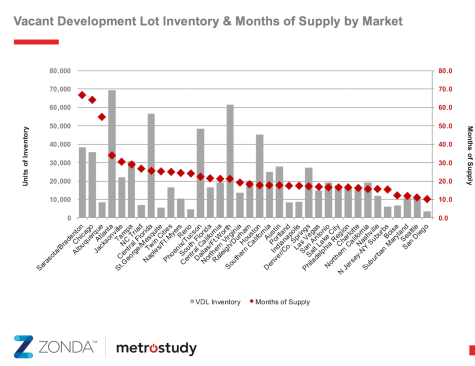

“Although new lot deliveries have more than quadrupled since 2010, it is barely keeping up with the demand and placing limitations on the overall growth in starts.,” says BUILDER sibling Metrostudy senior VP David Brown. “The overall months’ supply of Vacant Developed Lots is hovering in the 22 to 23-month supply range. However, that does not give a complete picture of the tight supply. Lot supply in the ‘A’ locations and most active communities is far more restricted and in many markets less than a 12-month supply.”

It’s common knowledge that raw land–what Metrostudy refers to as Future Lots–is taking more time, more aggravation, and more money to shepherd tracts through planning, entitlement, permitting, and development. So, for private companies, the lot pipeline reload prospect is for a double-whammy of pain: Risk and time-suck.

In most regions, a 20 to 24-month supply of lots is considered to be in equilibrium,” says Brown. Two-thirds of the states are well below this level. The four states that have a supply above this level have it because of legacy lots in far peripheral locations that have not reactivated.”

Net net, private home builder principals face a moment of truth.

- If they want to say on and grow, they’re likely going to need to share equity in their company with a strategic buyer like the Japan-based companies, or like Clayton Properties, or perhaps one of the Canada-based companies.

- If they’re hitting that age-demographic tipping point where another downturn-cycle is uninteresting, they may want a nearer-term exit plan, for which a sale to one of the U.S.-based public company buyers may make the best fit.

- Or, like our principal at the firm in one of the hotter markets right now, the tack may simply to be to run down the current lot count, bank the profits, and try to pounce when land prices decline and distressed deals become available again.

That, of course, is a risk. So, too, is the inverse, which is to go to lenders now and borrow while the pace of demand is strong, and put that capital into more expensive land deals for 2022 and 2023.

Big dilemma. You have to either really believe in your powers of cycle-timing prediction, or be a glutton for punishment to leverage up in this climate.

So, while there are strategics trolling who want both land assets and good local operators with local land relationships, more private firm principals are ready to talk about selling.

Take, for example, Carolinas-based Essex Homes, whose principals closed Tuesday on the sale of the operation and its assets to Daiwa House-owned Stanley-Martin Communities.

“We came to work this morning and arrived at a company that did about 2,000 homes in 2019, and now we’ll do close to 3,000 home this year,” Stanley-Martin president Steve Alloy said Tuesday. “We went from 6 markets to 11 overnight. We’re now in the top 25 of the Builder 100, and our plan–with Daiwa House–is to become a national, top 5 company in every major market in the U.S. This is another step in that process that began three years ago.”

Alloy notes that the grand strategy he’s helping Osaka, Japan-based Daiwa House carry out means finding strong operators like Essex founding-principal Karl Haslinger, whose intent is to stay on and continue to build the business, albeit under the new Stanley-Martin flag. The deal solves for Stanley-Martin’s need for both not just the work-in-process and incremental volume, and an extended lot pipeline in the five new markets, but also, all of the local knowledge and operational practices Haslinger has developed with his team over three-plus decades.

“We’re not sending our people to go to Essex and run it,” says Alloy. “The most important part of this combination for us is that it’s not a cash-out and retire mentality, but a deal that focuses on people at Essex becoming part of an organization that’s a $40 billion global company, one of the largest enterprises in the world, and one where the folks at Essex feel there are strong opportunities to stay and grow with us.”

On the surface of it, it looks like the No. 1 motivator for Haslinger is financial, access to the trove of patient capital that the deal represents, not to mention a windfall in the sales event. However, almost more important to him and his Essex Homes leadership team–virtually all of whom will stay on in roles as regional officers for Stanley-Martin–is the amount of time they recoup.

Principals at most of the private home building companies tend to spend an inordinate amount of time pursuing, managing, and worrying about capital, which tends to displace bandwidth and energies and innovative leadership on the operational home building and customer focus front.

Deals like the Stanley-Martin combination with Essex give that time back to the principal, so that he or she can commit and invest full attention to growing the business.

Simultaneously, the buyer wins on the time front as well.

Christopher Jasinski, a managing partner at JTW Advisors, which advised Essex Homes in the transaction, notes that time-to-entitle raw Future Lots in this marketplace has emerged as a critical motivator for a larger posse of active buyers in today’s home building M&A market.

“You can’t buy raw land from Farmer Joe or Farmer Mary and get it into the finished developed pipeline for at least three years, for the most part these days,” says Jasinski. “This longer entitlement process–I think–is a factor motivating some of the M&A dynamics we’re seeing.”

Jasinski sees U.S.-based public companies kicking it up a notch in their hunt for deeper local scale, an in-year unit volume bump, customer segmentation portfolio tuning toward lower priced product, and, again, access to a finished lot pipeline expansion that can bridge the intensifying gap between the end of 2020 and the end of 2023, which is the soonest many raw lots could be delivered.

“We envision a fair number of those ‘bolt-on’ acquisitions by public companies in need of shoring up their land asset, replacing the land they’re going through at a faster pace right now,” says Jasinski.