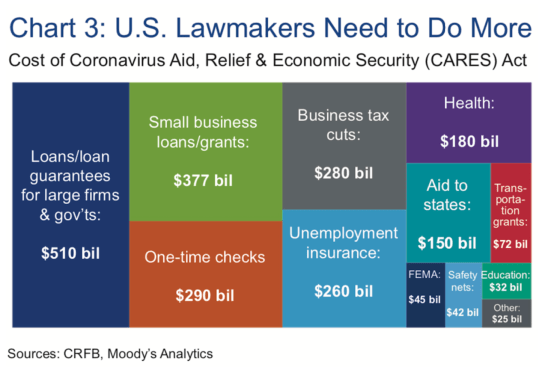

Pile up all of Congress’s trillion-dollar rescue packages, Fed monetary and fiscal stimulus, forbearance, forgiveness, low- and no-interest loans, etc., you want, one question bears down us now that it’s very hard to answer.

Jobs.

Our next live #BuildersAreEssential webinar–Cash Crash Course–featuring Cohn Reznick direcrtor Steve Friedman, is a must-attend if you want ideas, tactics, strategies to help navigate the shocks and turbulence we expect as jobs evaporate, the economy staggers, and the nation looks for ways to regain its footing in the months ahead. Register here.

If the economy was humming–not without a few noteworthy structural challenges–at full employment, and if the housing economy was tracking upward because household wages were making a bit of headway into February, what now? Estimates ranging from a quarter to a third of the U.S. economy are in some form of mandatory lock-down, and speculation as to the magnitude of impact on household spending, wealth, and earnings capacity is early on in a steep learning curve.

Scouts learn a tourniquet to save a life, without perhaps, the loss of a limb. Can the U.S. Treasury, and the 50 states and their representatives, and the hundreds of thousands of cities and their respective elected and appointed officials, and more importantly, can America’s households–who shoulder two-thirds of our economy–do the same?

Jobs are, or is, the question. By official counts (very possibly vast undercounts), 17 million–and counting–are gone in a matter of a few weeks. Will that number double, triple… before this is over?

A related essential issue in question comes packaged as a single term: duration. How much can be done to a) stanch, and b) invert the second-derivative rates of change from deterioration to “green shoots” recovery?

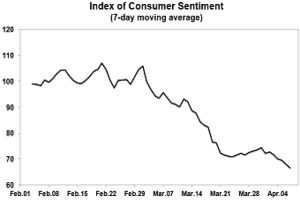

Consumer sentiment, which, most times, we take for granted as a glacially-trending indicator, only begins to tell the story of agonized stress to the GDP’s most important component, households:

Consumer sentiment plunged 18.1 Index-points in early April, the largest monthly decline ever recorded. When combined with last month’s decline, the two-month drop of 30.0 Index-points was 50% larger than the prior record. Of the two Index components, the Current Conditions Index plunged by 31.3 Index-points, nearly twice the prior record decline of 16.6 points set in October 2008. In contrast, the Expectations Index fell by 9.7 points, a substantial decline, but not nearly as steep as the record 16.5 point drop in December of 1980. This suggests that the free-fall in confidence would have been worse were it not for the expectation that the infection and death rates from covid-19 would soon peak and allow the economy to restart. As noted in last week’s special report, anticipating a quick and sustained economic expansion is likely to be a failed expectation, resulting in a renewed and deeper slump in confidence.

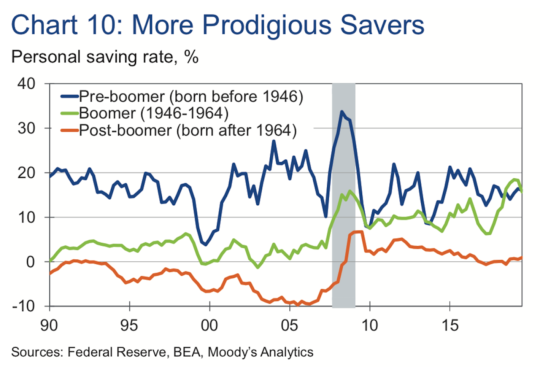

Mark Zandi, chief economist at Moody’s Analytics, observes that consumers are resilient, but that the other-side of the Covid-19 pandemic health crisis may see some profoundly impacted consumer behavior for some time. He writes:

COVID-19 will undoubtedly change how we live and work for a long time to come. Consumers and businesses are likely to be more cautious and save more. The baby boom generation, close to or al- ready in retirement, will have little choice but to save substantially more and spend less. Prior to the virus, this cohort owned more than half of stock wealth, accounting for more than one-fifth of all their as- sets. With stock prices down over 20% from their peak, and prospects that they will not recover the lost ground anytime soon, boomers will need to adjust their expectations and spending. But households of all ages will not forget how quickly jobs vanished and household finances were wrecked. There will surely be some pent-up consumer demand that is unleashed once we are on the other side of the virus, but consumers will be more prodigious savers, just like those who lived through the 1930s’ Great Depression or suffered through the financial crisis.

Consumer spending patterns will also shift, at least for a while. People will not travel as much, at least not to faraway destinations and especially not until the virus is licked. It may also take a while to get people to attend big events and crowded places. Healthcare and housing may become bigger parts of the typical American’s budget. Much more shopping will be done online. This trend was firmly in place pre-virus, but it will now be supercharged as people learn to purchase just about everything online: groceries in particular.

The most significant longer-term casualties of the virus will be lower-income households that had just begun to benefit from the previous record-long economic expansion and tight labor market. Wage growth for those in the bottom of the income distribution had been rising fast- er than for any other income group. With the job market in disarray, and unlikely to return to full employment for years, lower-income house- holds are sure to be left farther behind financially. The income and wealth distribution, which is already highly skewed, will become more so.

Of course, the walking bridge from consumer households to an eventual recovery is small business. Almost half the U.S. workforce–60-million-plus earners–derives livelihoods from businesses with fewer than 500 employees. As with consumer sentiment, confidence, and outlook, small business optimism indices are staggering under a sudden shock to their system, only now beginning to measure their free-fall from grace.

The NFIB Small Business Optimism Index fell 8.1 points in March to 96.4, the largest monthly decline in the survey’s history. Nine of the 10 Index components declined, which is evidence that economic disruptions are escalating on Main Street as small businesses struggle to keep their doors open. The small business sector is anticipating and bracing for continued economic disruptions going forward.

“Small businesses are living through the coronavirus pandemic right now and it’s hard to say what the severity of the disruption will be, but we do know they’re feeling the urgency,” said NFIB Chief Economist William Dunkelberg. “It is vital that these businesses have access to federal funds that are made available through the CARES Act to keep the doors open on Main Street.”

And what are home builder firms, their partners in distribution, trades, and other vendors, for the most part other than small businesses. National Association of Home Builders analysis of its members reflects that 98% of its builder members are from firms with fewer than 100 employees.

NAHB’s builder members reported that they had a median of 5 employees on payroll in 2018. The plurality of builders – 32 percent – had 2 to 4 employees and about a quarter had 5 to 9. The median number of employees on payroll has been 5 since 2015.

In 2018, builder members started a median of 6 housing units, up from 5 in 2017. The plurality of builder members – 21 percent – started 2 or 3 units.

The median dollar volume of business among builder members was $2.7 million in 2018, unchanged from 2017. The median dollar volume of business essentially plateaued between 2008 and 2011, with levels ranging from $0.9 to $1 million dollars, then rose sharply between 2012 ($1.1 million) and 2015 ($2.5 million). It slipped to $2.4 million in 2016, and increased in 2017 and 2018 to reach its highest level since the inception of the Census ($2.7 million).

#buildersareessential, then for two reasons. One, they’re the salt-of-the-earth companies whose wherewithal and viability are a lifeline to a next recovery. Two, they’re small businesses, who’s payrolls and contracted labor absorption, bear an outsized burden right now to restore confidence among consumers right now, which has fallen off a cliff. Thing is, hundreds, thousands of builders’ businesses are at risk of existential solvency, liquidity, cash threats, from both stoppages and delays, and from a yet unknowable scope of collapse in consumer demand.

This is central to our second #buildersareessential webinar. The gushing arterial hemorrhage right now, for society, is in jobs and earnings outlook for people who run and work for small businesses. That’s where cash flow is existentially invisible, where rescue programs are a last resort, and where duration of the economic pause is a matter of life or oblivion.

Here’s what we’re covering Monday, at 5 pm EDT, in our #buildersareessential “Cash Crash Course,” session. Register here, to learn what builders and their partners need to know now about cash tactics in a moment where every dollar is crucial. We turn our focus to the existential threat to business viability and the dire need to access cash – both to deal with pauses, and to offset revenue misses due to disruption, as well as other disconnects in the flow of vital resources to the industry right now.

Steve Friedman, Director, CohnReznick, will be a key presenter. Steve, a nationally known real estate figure whose area of expertise is accounting, finance, policy, and business planning, will help navigate the cash crunch peril builders face as a threat to survival. The webinar will explore:

- What should firms already have done by now?

- How can firms “tear apart” their businesses to understand how to preserve cash now?

- What costs should firms think about ceasing immediately?

- From 40,000 feet, how will access to CARES act programs help and reset a nearer-term survival process?

- What are classic “best practices” for Black Swan-type massive disruptions to business that might be helpful to draw on now?