Call the back-half of 2019 a crossroads. It’s where builders’ recent surge of guarded optimism smacks up against a perfectly logical uneasy sense that all things–even low-boil, half-good housing recoveries–must pass.

The June-through-December and beyond big picture assessment among leaders in the single-family for-sale business we’ve been talking with, listening to, and reading transcripts of, is pretty simple. Detecting or understanding what comes next is–when it comes down to reality–impossible. You believe either that momentum has rebooted and is likely to run for another good stretch, or that the current bounce might be but a fleeting preface to truly tougher times to come. Of course, the field is wide open to SWAG: scientific wild-ass guessing. The action item, however, is crystal clear up and down the accountability chain, and it’s really one little word.

Win.

It’s an antidote to uncertainty, a fix–at least temporarily–for a cyclical deceleration, and a way to clear a path of less competitive resistance, fueling even more accelerated growth once what almost everybody expects is inevitable but almost nobody knows when–a downturn–occurs.

And no division president alive would deny it’s a rush to see evidence one’s team has gained share among his or her flags in any given sub-market. When things are tough all over, being better than the rest has its definite benefits.

The backdrop, everyone knows, is a still-massively under-served market. New construction’s slogging pace creates greater pent-up fundamental household demand by the day, especially at the hard-to-deliver lower price tiers. The U.S. economy’s chugging along by nearly every meaningful measure–jobs, corporate profitability, and consumer spending, and even signs of some household income growth. And, that’s not to mention underlying demographics, an engine that hasn’t even kicked in to high gear.

All that said, being 11 years into an eight- to 10-year typical cyclical recovery cycle adds both height and thickness to a growing wall of worry. This is especially true with the wild gyrations and high-anxiety of global trade relations, signs of economic weakness abroad, mounting political risk, and at least one recent jobs report that–while not worrisome in isolation–disappointed enough to at least get our attention.

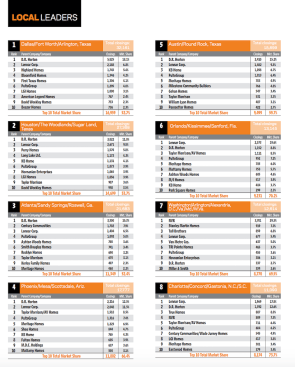

So, with the thought that getting up in the morning and winning–selling more than the ones down the street, snagging that off-market land opportunity, securing visibility, quality, and mutually beneficial terms with your trades as well as strong high-volume price considerations among materials and product partners, vendors, and members of the channel, etc.–is a non-negotiable, let’s unpack a few related gems from our recently released 2019 Local Leaders special data analysis, assembled with a big assist from our sibling teammates at Metrostudy.

Local Leaders, after all, is all about the top 10 builders–by unit volume sold in the 12 calendar year months of 2018–and the percentage share they collectively command of the nation’s 50 most-active new-for-sale housing markets.

Net, net, while smaller home building firms in these arenas may retain an edge when it comes to giving home buying customers a personalized, concierge-style experience in their “journey” to a purchase and beyond, that’s going to have to offset some otherwise daunting disadvantages.

It’s instructive to look at the 2018 Local Leaders data because it illustrates a strategic power play in motion–that started playing out at an intensified level about the time that D.R. Horton acquired Forestar and Lennar acquired CalAtlantic. Both of those deals, and the market pivot that followed them starting in mid-2017, will likely continue to reshape the top market home building landscape, accelerate consolidation, and change the rules of engagement for anybody competing in these top 50 markets.

We’re referring to what analysts, experts, and investment pros have begun calling “deep local scale,” and it speaks to locking up greater market share control in concentrated geographical arenas, with several equally motivating opportunities for advantage, which we’ll review for background.

- Access to land: Local operational concentration literally puts boots on the ground, allowing land acquisition strategists to nurture relationships with current, prospective, and not-even-thinking-about-it-yet land sellers, locking down the lots without entering bidding wars for them. What’s more, having the purse-power to green-light a land deal, offer take-down visibility at a cadence and on terms land sellers like, and partner with development resources to throw into the mix further add clout to those with a bigger, local, concentrated presence.

- Labor: The assumption being a greater likelihood of securer, smoother, more predictable, and more financially manageable deals with skilled trades, thanks to the increased visibility and transparency skilled workers would have to steady, reliable, terms all of which are a by-product of local market clout and share of the market.

- Materials and products procurement: Concentrated scale means volume discount opportunities, greater logistical efficiency opportunity, straightforward installation support, and other benefits of bulk pull through the local channel infrastructure.

- Construction management: supervisors can save on windshield time and manage both efficiency and right-the-first-time quality in their operations with systems, processes, disciplines, and local accountability that’s hard to match when a division is an “outpost” versus a deeply embedded, “excellence center” producing ever more predictable performance.

- Actionable customer data: Deep scale means more opportunity to listen to, speak with, and engage more customers–dreamers, prospects, tire-kickers, motivated buyers, etc.–learn, rinse and repeat. This potent knowledge base, to date under-leveraged as a sales and marketing solution for builders could evolve into their most powerful advantage of all–removing pain and friction from the home buying process.

At a high level, a big reason big builders have been deploying a lot of capital into fulfilling these concentrated manifest destiny geographic strategies is their bet that, by doing so, they can hack away at both operating overheads, like cost of sales, and direct input expenses–wasted time, labor cost, materials, etc.–and wean themselves of dependency on land value appreciation to make money.

This longer-term strategy, let’s remember, also has perqs for a nearer-term future scenario that assumes a cyclical deceleration. It gives builders with locally concentrated clout a wider range of competitive ammunition on price-point options (i.e. incentives, discounts, down-payment assistance programs, options, upgrades, etc.), and, at the same time, a greater opportunity to leverage smoothed volume, cadencing, etc. into margin-protecting operational disciplines. Winning, in other words, turns up the heat on those who are not.

The big players know very well that the business is pitching (relatively) headlong–whether it’s in the next 24 months or 60 months–into a far more modernized, factory-assembly based infrastructure, and they’re focused on market dominance to avail of that infrastructure when the next recovery cycle kicks into gear.

They know too that they’ll have to invest themselves in those capital intensive initiatives, and they’re going to need to capture some of that investment by reallocating at least some resources they’re already using, which means finding savings, wasting less, and operating at improved levels of performance on any number of levels.

All of these themes show up in the competitive, multi-trench warfare at the sub-market level within housing’s 50 or so most-active new-home selling markets. Every point of market share gain gives a builder that much more latitude on price, and that measure more of leverage on gross margin per unit. Every increase in pull-through of absorptions per community per month yields greater visibility on both the cost and the potential for margin protection.

The Builder 100 top 15 or 20 firms–now an exclusive-membership clique consisting of major publics, the Clayton portfolio of regional power-house operators, and two or three noteworthy independent, multiregional private operators–David Weekley, Ashton Woods, and Shea–figure prominently in and among our Local Leaders rosters, in nearly every one of the top 50 new-home markets. Add in the Japan-enterprise owned portfolio, and you’ve got an even greater representation of the muscle in the top 50.

We’ll get into some immediate, median-term, and longer-term implications in a moment. First 10 nuggets of interest that jump out of the Local Leaders data sets.

- At least one top 15-ranked home builders from the Builder 100 show up in all except two of the top 50 markets–Kansas City and St. Louis.

- Top 15-ranked builders from the Builder 100 dominate three of the top 50 markets, Charlotte, Las Vegas, and Seattle, as eight out of the top 10 builders in these markets are Builder 100 top 15 firms.

- Nine markets of the Top 50 are led by private home building operators: Nashville (Ole South Properties), Indianapolis (Arbor Homes, now a Clayton unit), Boise (CBH Homes), Salt Lake City (Edge Homes), Oklahoma City (Rausch Coleman Homes), Kansas City (Summit Homes, a Clayton unit), Colorado Springs (Elite Properties Group), Cincinnati (Fischer Group), and St. Louis (McBride & Sons).

- D.R. Horton and Lennar both show up in the top 10 rankings in 32 of the Top 50 markets

- Lennar is a Top 10 Local Leader operator in more Top 50 markets than any other builder, 39.

- D.R. Horton is absent from only 14 of the Top 50 markets as a Local Leader.

- Lennar and Horton both command Top 5 market share in more than half of the Top 50 markets

- Pulte ranks as a Local Leader in 31 of the 50 most-active new home markets, while most of the other big publics, NVR, KB Home, Taylor Morrison, Meritage, Century Communities, Toll Brothers, appear as Local Leaders within a typical range of 10 to 15 markets among the 50.

- Japanese firms–Daiwa House, Sekisui House, and Sumitomo Forestry–now own Top 10-ranked home builder operators in 12 of the Top 50, the equivalent of all but three of the major public home building enterprises.

- Clayton, which began acquiring site-build home building firms in 2016, now has operating units that rank among the Local Leaders in 11 of the Top 50 markets.

All of those data points are interesting, and to some, select ones are more meaningful than others.

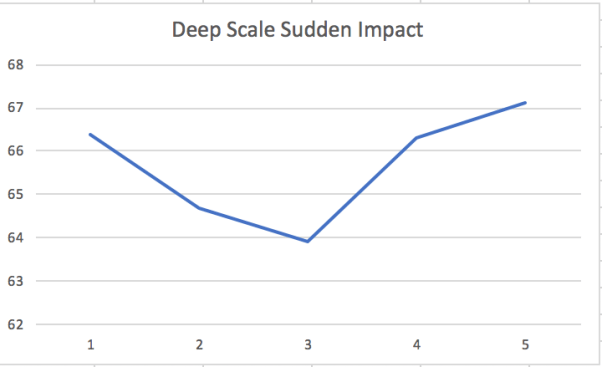

Here, however, is what you need to know about deep local scale. It means winning. Repeatedly, and more and more decisively. The pivot point has come, and you can see it here in this chart.

Source: Metrostudy and BUILDER analysis

Local Leaders builders commanded an average of 67.1% of the share of volume in the Top 50 markets in 2018, within 24 months of the big D.R. Horton and Lennar acquisitions of Forestar and CalAtlantic, rewriting the rules of engagement for critical access to lots, skilled labor, better deals with distributors and other vendors, greater operational efficiency, and pricing optionality.

This latter competitive advantage turns up the heat on in-market rivals as demand gets choppy, randomly spotty, and consumers become more susceptible to being “spooked” by either interest-rate changes, political turmoil, or headline risk.

Why this matters is important here. Personally-guaranteed (recourse) loans, reputations, relationships with customers, staff, partners, investors, and, at the base of it all, trust are all at stake when smaller market players get squeezed into corner on pricing, as heavyweights push volume and pace over margins. Once they commit capital and place it into their land investment, based on an operational model that builds in high-touch customer care and quality management, they’re more or less locked in. Either they sell at that firm price range, or they cut back on their already-razor thin margins to keep repayments to lenders flowing on schedule.

If you take a careful look at the Top 50 market Local Leaders in light of this deep-local-scale pivot, the first thing that jumps out at you has enormous implications for consolidation, mergers and acquisition, and the primacy of home buildings 10 to 15 Builder 100 enterprises.

Of the 500 firms listed among the Top 10 operators in the Top 50 markets, about 20% to 25%–between 100 and 150 firms–of them are independent local or regional home builders–roughly in the low 100s companies. This is the case after removing Clayton, Japan-company owned, Canada-based company-owned, and the top three multiregional private companies, David Weekley, Ashton Woods, and Shea Homes.

This means that–particularly where local companies generate lucrative financial performance in vibrant–but not exorbitant–like Indianapolis, Salt Lake, Provo, Boise, Minneapolis, Kansas City, Richmond, VA, and Virginia Beach, you’ll see big strategic player interest in the 250- to 300-a-year independent operators who’ve got some land pipeline out ahead of them into 2020 and maybe 2021, but not much beyond that.

What’s more, in the the leading 10 to 15 markets, where the economies are steaming along and where home prices haven’t yet reached beyond the means of all save a few high-end households, there tend to be two, or three, or even four strong independent home building operators who represent prime candidates for acquisition discussions.

They know very well who they are, and, they’ve got a tough decision to make during the next six to 12 months.

Do they stand pat and do all it will take to ride through the turbulence of another cyclical downturn, after which big, powerful, deep-pocketed, and option-filled players will have cornered even more of the markets?

Or do they find a potential capital sugar-daddy to smooth them through a rough-go ahead, either exiting altogether, or bargaining for a graceful multiyear rampway to retirement?

There are strategics now who are looking. They’ve either missed on volume and growth guidance and need the incremental deliveries a strong private operator would provide through the back half of 2019, not to mention relationships that represent an opportunity extend the land pipeline another 24 to 36 months with some astute acquisitions. Other strategics, both public and private, are still building out a manifest-destiny footprint with an operational model that appears to work well in new markets. LGI or Century Communities, on the public side, and others, still-growing privates on a mission.

Jacksonville, FL-based Dream Finders, which operates in six markets–Jacksonville, Orlando, FL, Savannah, GA, Austin, TX, Denver, CO and the Washington, DC Metro areas–recently added Bluffton, SC based homebuilder Village Park Homes, to its fast-growing footprint. Toll Brothers, a bit earlier, added a full-plunge into the Atlanta market with its purchase of Sharp Residential, serving from the second-time move-up market to entry-level customer segments, mostly in Atlanta’s hot “11 o’clock-to-2 o’clock” northern suburbs.

And then, of course, Japan-based firms–Daiwa House, Sekisui House, and Sumitomo, to name the most active–are still motivated to reach fully-realized strategic investments in North America as a long-term play in their global roadmap. Expect more action on that front. Too, Clayton may or may not have reached its digestion plateau–where it’s going to work on full integration of its site-build unit portfolio before adding to it. Don’t count out another move or two from the Maryville, Tenn.-based juggernaut.

What’s certain is this. Of those 100 to 150 currently-independent firms ranking in the Top 10 builder rosters among America’s 50 most-active new home markets, odds are pretty strong that many of them are taking calls, or initiating searches that might match up their interests with an acquirer, strategic venture partner, etc.

We’d guess that as the deep local scale grip tightens control of more of each market, a fair number of those independents will be motivated to call it time for a financial event.