The early interpretation in news of Lennar strategic executives’ discussions to sell its Rialto Capital unit is that the initiative is a reaction to “headwinds” causing a slow down in sales of new homes around the nation.

Wall Street Journal staffers Craig Karmin, Laura Kusisto, and Dana Mattioli clearly infer a connection between new home dynamics and Lennar’s Rialto positioning here.

Lennar Corp. is in advanced talks to sell its real-estate lending unit, looking to offload the business at a time when the nation’s largest home builder and its peers are struggling alongside a stagnant housing market.

The Miami-based company is in discussions with the private-equity firm Stone Point Capital LLC for the sale of Rialto Capital, according to people familiar with the matter.

While essential facts of the story–that Lennar is in discussions to sell Rialto to Stone Point Capital–may be correct as reported, two important parts of the narrative are glossed over–or actually distorted–in this analysis.

The why. And the why it matters, especially now.

This is important, both to understand what’s going on at Lennar, and what’s going on with the housing market. Conflating Lennar’s disposition of Rialto into a reactive tactic as a sign of deteriorating conditions in the single-family market misstates an important strategic focus, and might equally err on its reading of the housing market, which has entered a choppy, anyone’s-guess period.

Let’s unpack this a bit by looking at tidings that Lennar may find a buyer for its Rialto Capital unit, an item executive chairman Stuart Miller mentioned in his latest quarterly earnings commentary with investment analysts and investors.

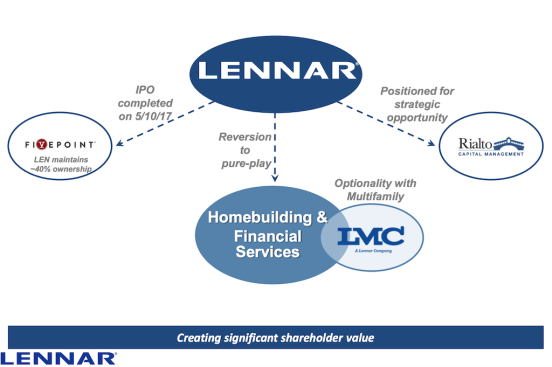

Since at least mid-2017, even before Lennar announced its plan to acquire CalAtlantic last year, the company has clearly telegraphed plans to pivot strategically to a more pure-play home builder, and this plan–which included the spin-off of its Five Point Communities unit via an IPO into a separate public company–meant looking to “harvest value” for its Rialto unit so that it could concentrate on core home building businesses, operations, and investments.

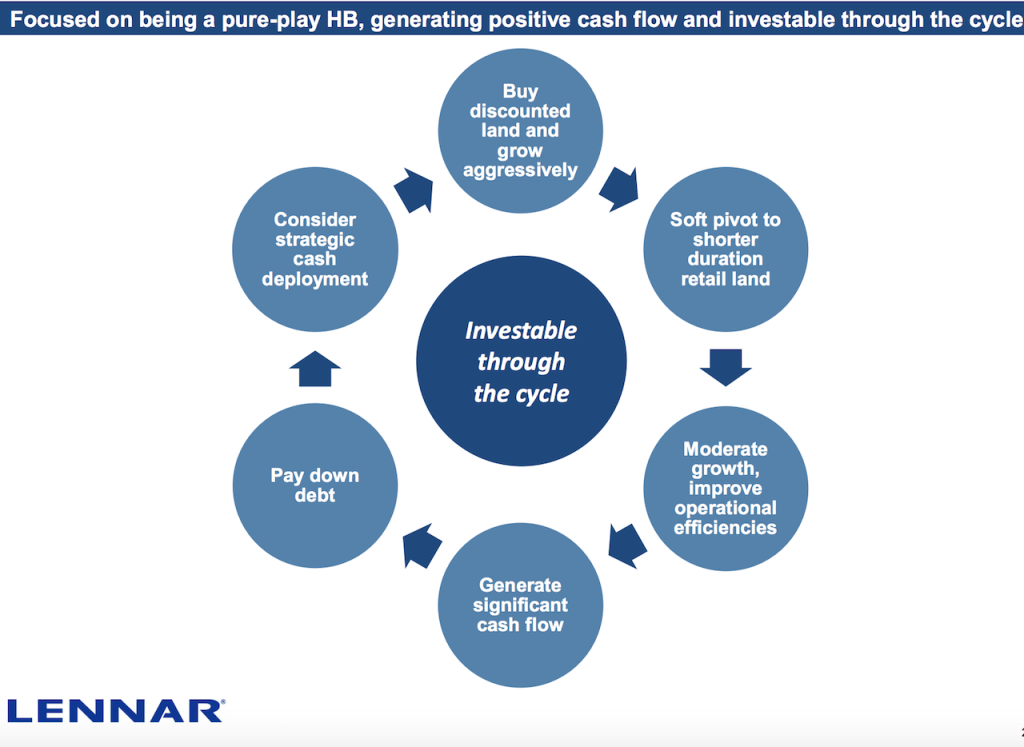

Now, Lennar is one of the best organizations in the home building business at market cycle timing.

This means capital it invests in real estate tends, more times than not, to yield better returns, partly because of how much Lennar pays for each of the lots in its pipeline, and partly because of when it puts that investment in place and when it can turn those lots with a home on them.

Thanks to this skill, it’s Lennar’s tendency to buy land when it’s cheap and harvest returns on inventory turns as the market matures, prices go up, and operating excellence discipline can increase margins on both the land and the value of the vertical construction. In the early part of a recovery cycle, it’s great guns growth, with an amassing of market share and divisional scale, and in the mid-part of the cycle, that slows down a bit, with less lot acquisition, fewer new communities opening, and more discipline on per unit margins and first-time quality.

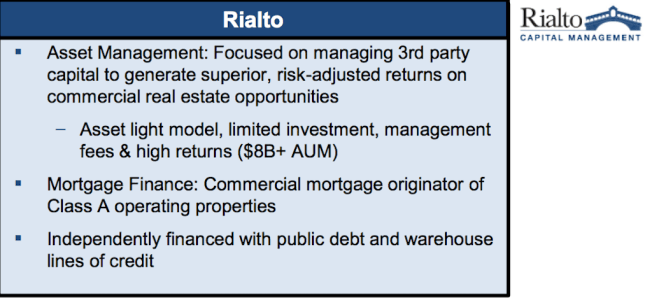

Now Rialto’s purpose as part of the Lennar business empire has been to serve as an asset management investment platform. Rialto identifies and funds investments in portfolios of commercial real estate opportunistically. This is not a core Lennar business in the “pure-play home builder” sense, but one that served, particularly during an earlier era of distressed real estate and bargain-basement pricing, as a high-margin way to use relatively inexpensive capital.

Lennar strategists’ big push in the past few years has been to make the company “investable through the cycle,” which means paring back on calculated risk associated with real estate investments, like Rialto, and doubling down on the ability to “build to value” on vertical construction and community development.

This means it can be more nimble with its capital treasure trove, it can sharpen its operational focus on extracting any expense in the home building process that does not tie directly to home buyer value, and it can re-invest that capital in newly emerging technology and data businesses adjacent to its home building operations, like Ring (now owned by Amazon) and Opendoor.

So, it’s an error to connect the Rialto sale discussions with a single-family market deceleration.

It’s also an error for reporters to “call the cycle” now because they’ve tracked a market softening over the past few months that has occurred in a widening geographical sphere of the U.S. landscape.

Interest rates, materials prices, mortgage interest deduction caps, etc., each or altogether may contribute as factors in the current period of slowdown. Most of the experienced executives we speak to acknowledge the slowdown, but won’t go so far as to predict that it’s signaling the end of the housing rebound. They’re more likely to express belief that fundamental economic momentum, job growth, continued pent-up household formation demand, and family-formation patterns of Millennials will kick the rebound back into gear once people have absorbed and digested the initial price and monthly payment shocks that are cropping up now.

This comes through in the latest issue of The Z Report from the team at Zelman & Associates, which held its annual investor forum for builders and building materials companies last week. The report [free trial link here] notes:

“For homebuilders, we expect market conditions to remain choppy through year end and anticipate that a greater need for incentives could pressure 2019 profit margins when those homes are delivered. With that said, unit growth should reaccelerate next year as demand laps the slower current activity, new communities come online and buyers inevitably adjust to the new rate environment as they have in almost all prior instances of large rate moves. We expect builders at more affordable price points to be best positioned.”

While Lennar does not have the most “affordable price points” in its product and community offerings, it has focused fanatically on data and technology investments that move it closer and closer to its customer, what they want, at the price that works for them, and creating an operating model to build to that value.

That’s “the why” of what’s happening with the Rialto business, and “why it matters” in understanding where Lennar is taking its organization over the next several years.