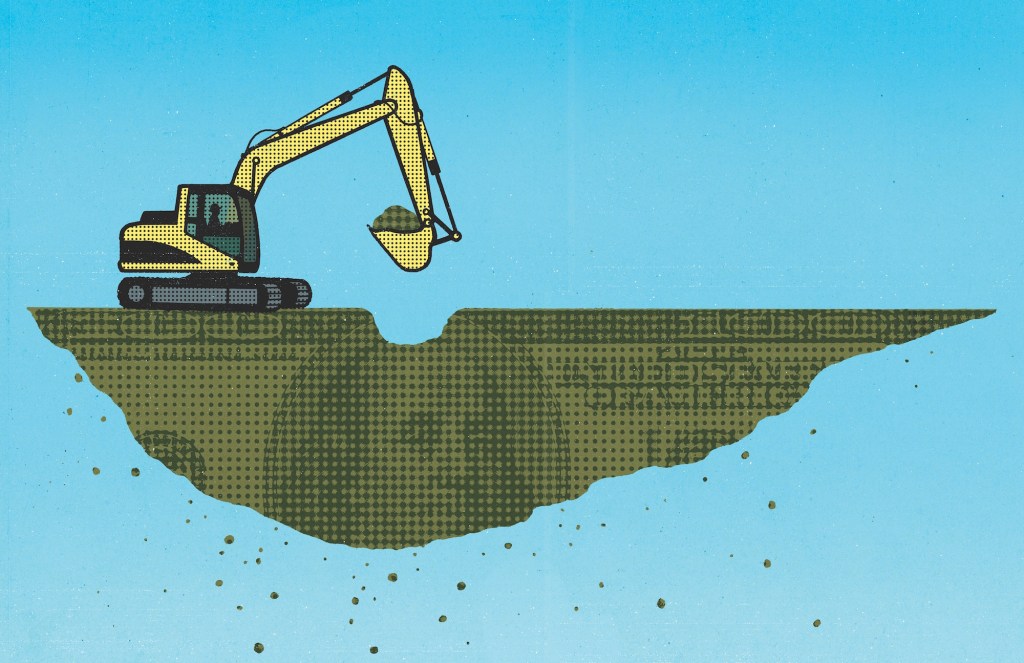

When Hovnanian Enterprises CEO Ara Hovnanian announced on the builder’s March earnings call that the time had come to begin paying down the company’s debt, the analysts on the call were at first puzzled. Only six months earlier, the company had announced a strategy to grow its way out of debt by building and selling more homes, using, of course, debt.

Once the analysts got their arms around the new strategy, they embraced it. The interest on the home builder’s $1.86 billion in total debt has consistently eaten into profits in recent years, and the shift in focus to finally shore up the firm’s balance sheet was viewed as a tacit admission that its 108% debt-to-capitalization ratio was no longer sustainable and that profitability just wouldn’t come any other way.

“They finally found religion and said it’s time to de-lever,” says J.P. Morgan debt analyst Susan Berliner, who notes the average debt-to-cap ratio for the home builders she covers is around 50%. “The only question now is whether they did it in time.”

Hovnanian was not the first to face this reality. Just a quarter earlier, Beazer Homes USA, with a debt-to-cap ratio of approximately 70%, made a similar announcement. And William Lyon Homes, which has a debt-to-cap ratio of 62%, told investors on its first-quarter call that it would take a bifurcated approach, continuing its focus on paying down debt while also seeking to maintain earnings growth. A notable exception among these highly levered builders has been KB Home, which also has a debt-to-cap ratio of 62%. It hasn’t given up on its growth ambitions; instead, it has doubled down on a land-buying spree, allocating

$1.3 billion for developing and purchasing dirt in 2016, if it finds the right opportunities.

One of the biggest reasons for the shift toward paying down debt at three of the four, analysts say, comes from recent changes in the price of money. From a credit perspective, home building is risky business. And with their higher-than-average debt loads, Hovnanian, Beazer, William Lyon, and KB Home all draw junk bond ratings at the riskier end of the spectrum from the three major credit agencies. The market for junk underwent upheaval in 2015 in anticipation of and culminating in the Federal Reserve’s hike in the Federal Funds rate in December.

That move—the first in more than nine years—hardly registered as a blip on Main Street, as mortgage rates barely budged.

“They finally found religion and said it’s time to de-lever. The only question now is whether they did it in time.” —J.P. Morgan Debt Analyst Susan Berliner

But on Wall Street, the quarter-point bump up contributed to a shift already underway in the high-yield bond market, one that signaled a sea change from years of cheap, easy money. Because the benchmark rate had been so low for so long, highly levered concerns had still been able to sell their debt in the fixed income market, since investors couldn’t get much of a return anywhere else.

“It was an unnatural environment, where we saw a tremendous amount of issuance in the below-investment-grade universe. There was a lot of money chasing down the credit curve, so you had more competitive pricing for higher-yielding, riskier names,” says James Gellert, CEO of quantitative ratings firm Rapid Ratings, which tracks 45,000 companies globally, as well as the broader market, to determine risk of default. “What you’re seeing now is a contraction in the availability of funds for higher risk companies.”

Or, as Berliner puts it, “Back in the fall, the whole high-yield market effectively shut down.”

What that means is that while home builders with good credit had been able to borrow money at about 4% interest, highly levered companies had to pay more—around 8%. But they could still borrow. Now, if those same kinds of companies want to take on more debt today, or refinance what they already have, they have to pony up 12% to 15%, if they can find willing investors—no sure thing.

Larry Sorsby, Hovnanian’s CFO, summed it up on the company’s conference call: “At least as of right now, the high-yield market is not allowing us to refinance.”

Adds Berliner, “They really didn’t have a choice.”

Now, Hovnanian plans to pay its debt by selling inventory it already owns, using land banking strategies, exiting the Minneapolis and Raleigh, N.C., markets, and winding down operations in Tampa, Fla., and the San Francisco Bay Area. Those moves, according to Sorsby, will help Hovnanian become a “cash machine” by selling houses on land it already owns and help it pay off its debt sooner, rather than later. The company didn’t immediately respond to a request for further comment.

Depending on how things shake out going forward, that may prove to be a prudent strategy. According to Gellert, the same conditions that allowed highly levered home builders to keep borrowing in the high-yield market for the last several years allowed companies of all stripes to raise debt across myriad industries.

“If you take all the outstanding fixed-income issuance in the global capital markets today, we have twice as much debt now as we did in 2007,” Gellert says. “We saw more and more companies issuing debt, because rates were so low. Some companies hadn’t ever seen those kinds of rates, so they kicked the can down the road. And that’s a perfectly viable corporate finance strategy, especially for lower credit quality issues.”

The only problem is, all of that debt is eventually going to come due. Gellert estimates $195 billion of corporate debt is set to expire in 2020, a 50% jump from how much was originally set to mature in 2016.

“You’re going to see companies that could refinance in the last five years not be able to refinance in the next five,” Gellert says. “We’re going to see a much higher default environment, more bankruptcy, and more forced acquisitions—a lot of stuff hitting the fan.”

Others who focus specifically on home building aren’t as bleak.

“We expect the housing recovery to continue at a slow but steady pace for a number of years. But we’re convinced that deleveraging while the housing market is still improving will create value for shareholders as the risk premium associated with owning our stock diminishes.” — Beazer CEO Allan Merrill

“I wouldn’t want to be so dire,” says Michael Dahl, a home building analyst who covers KB Home for Credit Suisse. “The catalyst for something like that would have to be much broader, in terms of truly not having access to credit. KB Home certainly is not in that position.”

While Gellert wasn’t referring to home builders specifically, if that kind of lending environment were to materialize, it would impact the broader debt landscape, builders included. And it would likely wreak havoc on those looking to refinance the debt currently on their books.

The debt-dumping journey Hovnanian embarked on in March is the same path Beazer has been on since the end of its 2015 fiscal year. On its fiscal 4Q 2015 call last November, CEO Allan Merrill told investors that the company had “decided to complement our growth ambitions with steps to reduce our leverage over the next couple years … to reduce both our cash interest paid and our ratio of debt to EBITDA.”

Dan Page

At the same time, he went out of his way to stress that the move didn’t reflect a bearish view on the housing market. “This decision should not be interpreted as pessimism about the shape of the housing recovery. In fact, the opposite,” Merrill said. “We expect the housing recovery to continue at a slow but steady pace for a number of years. But we’re convinced that deleveraging while the housing market is still improving will create value for shareholders as the risk premium associated with owning our stock diminishes.”

A Beazer spokesman referred BUILDER to the transcript of the company’s conference call when contacted for comment.

Beazer has followed through on its promise to bring debt down, paying off $25.9 million in 4Q 2015, $23 million in 1Q 2016, and an additional $5 million at the beginning of 2Q 2016. And, it says it will now pay off $100 million in fiscal 2016, up from its original pledge of $50 million. It was the type of talk—and action—that makes debt analysts in the current environment swoon.

“Beazer has been a top-10 home builder,” Berliner says. “Over the last few years, they’ve actually tried to grow into their capital structure. But then they took it a step further a couple of quarters ago and said they didn’t just want to grow into it, but de-lever it, too. So they are very laser focused on de-levering, which is exactly what they should be doing. We like that a lot.”

After Beazer announced it would put its financial house back in order, Standard & Poor’s in March upgraded the builder’s CCC credit rating for unsecured debt to CCC+. While that didn’t lift Beazer out of junk status, it was a positive for the company. In fact, Beazer was able to take out a new, secured loan for $140 million in March to help it pay off older debt.

Matt Zaist, CEO of William Lyon Homes, says 2016 has always been a de-levering year in his mind, ever since the company bought Polygon Northwest in 2014 to increase its footprint in the Seattle and Portland, Ore., markets. That deal was a large contributing factor to driving William Lyon’s debt-to-cap ratio above 60%, and the company has said it wants to drive that number toward 50% in 2016 by building on land it already owns. While Zaist said volatility in the capital markets as well as the slower-than-expected recovery were certainly factors to watch, neither spurred the company to focus on paying down its debt now.

Dan Page

“I might feel differently if I had maturities coming due this year, next year, or the year after that,” Zaist says. “A big piece of our overall reduction in leverage as a percentage of debt should come from the capitalization side of the equation. We can still grow without growing debt by increasing our top line, and that should help move the needle significantly.”

KB, instead of focusing on debt, had pledged to buy $1.5 billion of land in fiscal 2016, or about 50% more land this year than last, according to Berliner.

It took that number down to $1.3 billion on its 1Q call, noting that the figure is its overall “capacity” for land, but that it will actually buy land only if it sees the right opportunities. Yet its debt-to-cap ratio actually crept up sequentially, to 62% in the quarter. While it did reiterate its long-term goals for paying down debt, it didn’t explicitly talk about a corporate strategy for honing in on the issue, even when asked by analysts.

“Over the last year, we kind of maintained the leverage that we had experienced in 2015 at the end of the quarter,” said Jeff Kaminski, KB Home’s CFO. “Our targets remain intact. We talked about over time [wanting leverage to] be in that 40% to 50% range on a net basis.”

Dan Page

Instead, KB launched a share repurchase program, announced in January when its stock traded around $10. It snapped up 8.4 million of its own shares in the first quarter for about $86 million, according to analyst Jade J. Rahmani at Keefe, Bruyette & Woods. Since then, unlike other highly levered home builders, its stock has rallied and jumped above $14 after it beat 1Q earnings estimates.

The move appears to have given KB’s stock a boost in the short term, and the company still has the option to buy back another 1.6 million shares. But the longer-term issue of debt continues to hang over the company.

“They left the window open to potentially repay debt, which we would look favorably on,” Rahmani says. “But they kind of talked around the issue, rather than addressing it head on.”

On the company’s call, CEO Jeff Mezger said the following: “We have a balanced approach to prioritizing our use of capital in order to support our growth, strengthen our balance sheet, and improve shareholder value.”

When asked to comment for this article, a company spokesperson said, “KB Home has been successfully executing its growth strategy, and we are positioned for more growth in 2016 and beyond. Since 2011, KB Home’s total revenues have increased 230% to over $3 billion in 2015, and we generated free cash flow of $200 million last year. Our leverage targets remain intact, at a net basis of 40% to 50%.”

Dan Page

Yet, given the current environment and the lackadaisical nature of the recovery, Rahmani says he’d rather see KB join its highly levered peers and focus on paying down debt now. “They’ve definitely been in growth mode, and the view for the last several years in the housing market has been that there will be an acceleration of that growth,” Rahmani says. “But to this point, it hasn’t happened. It’s been disappointing. So now, with the spread widening in the fixed-income market, it seems like the capital markets are flashing warning signs. You really don’t want to see management teams get on the conference calls in the middle of this and say they’re going to keep buying land.”

In fact, that’s how the highly levered home builders got that way in the first place. “Builders got caught up in the enthusiasm of the housing bubble back in the mid-2000s, and most of them bought too much land, or they paid too much for it, or a little bit of both. And some took longer than others to recognize it,” says Alex Barron, senior research analyst at the Housing Research Center.

When the recovery came, those who had worked through their balance sheets during the bad times were able to take advantage when things got better. Those who hadn’t, couldn’t.

“Since the recovery, the difference was that the guys who became profitable sooner started doing land deals in 2009 to 2011, when things were still cheap,” Barron explains. “But the builders we’re talking about here took a little longer to feel confident and didn’t start buying land again until 2012, 2013, and 2014. By then, prices were already a little higher.”

Barron says the decision to pay down debt now, rather than chase more growth, makes sense given market conditions. “What you wouldn’t want to do is miss out on a boom. But we haven’t seen a boom. So I think missing out on single-digit growth is no big deal. I’d rather fix my balance sheet.”