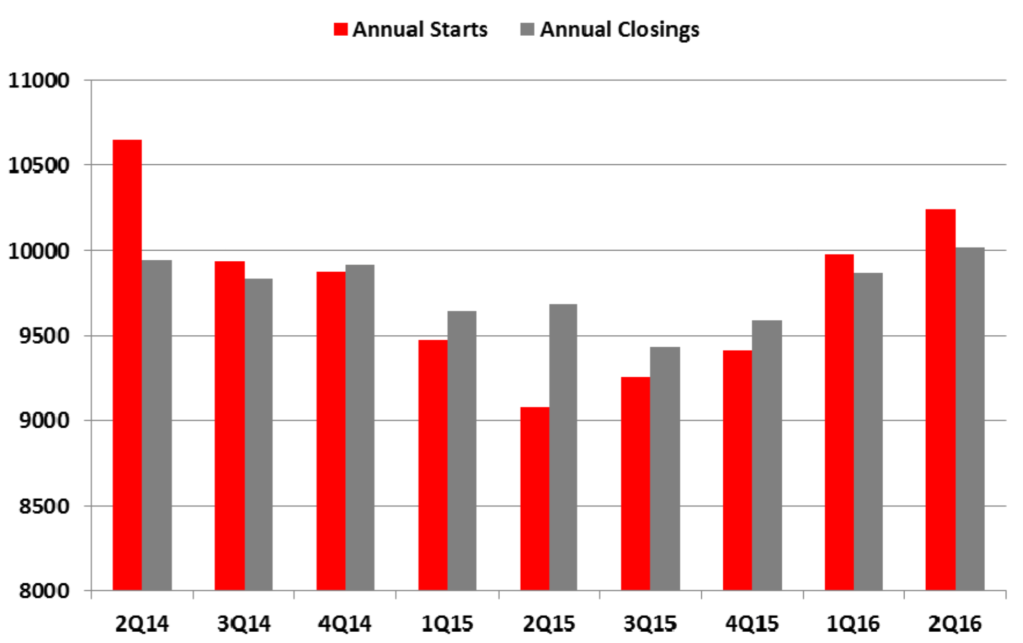

Metrostudy’s 2Q16 survey of the Philadelphia region’s housing market shows that there were 2,752 home starts in the quarter, up 15.4% from 1Q16 and up 10.7% year-over-year. Annually, starts numbered 10,245 at the end of 2Q16, an increase of 2.7% from the annual starts pace last quarter and up 12.8% from a year prior. In 2Q16, quarterly closings increased 21.5% quarter-over-quarter and rose 6.3% year-over-year. The annual pace of closings was 10,017, 1.6% higher than 1Q16 and up 3.5% from the same period last year.

The Philadelphia MSA had 1,483 starts for 2Q16, a big 21.7% gain from 1Q16 and 4.6% YoY. Annual starts came in at 5,529, a 1.2% increase from 1Q16 and up 14.5% over 2Q15. Closings for the MSA came in at 1,184, an uptick of 5.2% from last quarter but an 8.1% decrease YoY. Annual closings came in at 5,264 for 2Q16, down 2% from last quarter but up 2% over 2Q15.

“Quarterly starts in 2Q16 continued Philadelphia’s impressive string of year over year increases dating back to 1Q15, while closings were still trying to catch up to the big gains made by starts over the course of the last four quarters,” said Quita Syhapanya, Director of Metrostudy’s Philadelphia market. “In 2Q16, the median closing price for a new home in the Philadelphia region was $345,900, which ticked up by 1% over the first quarter. Year over year change was a slight 0.6% increase compared to the same period last year. The median closing price for a single-family home was $386,200, a 7.2% increase from the prior quarter and up 6.2% from 2Q15.”

Total housing inventory – model homes, under construction units and finished vacant homes – for the Philadelphia region increased 2.2% QoQ. The number of homes under construction increased to 4,135 units compared to the 3,890 units under construction in 1Q16. Finished vacant inventory decreased to 2,635 from the 2,736 in 1Q16. Model home inventory continued to rise, with an additional 15 new models opening up compared to the prior quarter, a 2.5% increase after the 45 that was added in 1Q16.

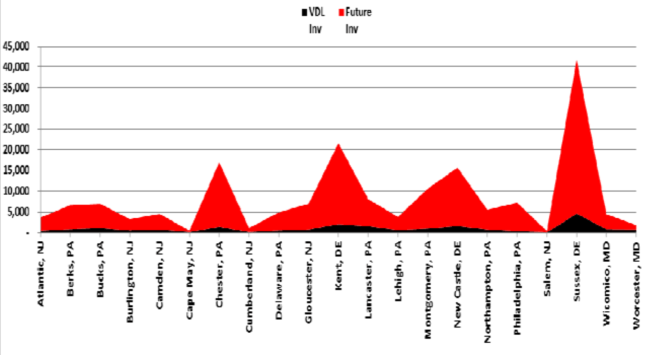

During 2Q16, there were 20,525 Vacant Developed Lots (VDL) in the Philadelphia Region. Finished lots decreased by 3% quarter to quarter. Year over year vacant developed decreased by 0.4%. The region’s vacant developed lot months of supply remains dipped to 24 months from the prior quarter. A healthy market supply level for equilibrium would be between 24 to 30 months. The annual starts rate of 10,245 for a rolling 4 quarters says it will take 24 months to go through the available finished lots. The significant gains in starts it shaved off 1.5 months off of the VDL months of supply.

New annual lot deliveries in the Philadelphia MSA were up 30.2% over this same time last year. Finished lots ended 2Q16 with an annual pace of 5,908 new lots. For the quarter lot deliveries are up 11.5% YoY but declined by 23% QoQ, an expected decrease after 1Q16, when builders put in the most lots in a single quarter.

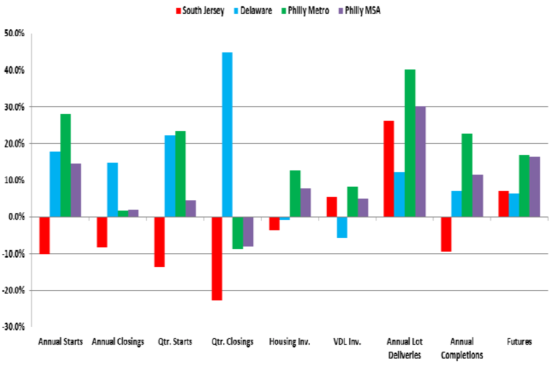

The Philadelphia region can be broken up into three distinct markets: the Philadelphia Metro, South Jersey, and Delaware markets:

- South Jersey saw their quarterly starts increase by 27.3% QoQ with a decrease of 13.7% YoY. After showing a YoY increase in 1Q16, annual starts decline by 10.2% YoY to 1,184 annual starts in 2Q16. Quarterly closings came in at 273, a 16.5% decrease QoQ and a 22.7% decrease YoY.

- Delaware continued to impress with stronger momentum in new home construction for 2Q16. The quarter ended with 1,081 starts, up 8.8% QoQ and 22.3% higher YoY. Closings for the quarter saw a big upward spike of 48% from 1Q16 and a 45% increase YoY. The annual pace of starts is up 5.3% over last quarter and annual closings are up 18% over last quarter. Delaware continues to drive new home construction in the Northeast Region.

- The five-county Philadelphia Metro had annual starts increase by 5.6% QoQ and increase 28.1% YoY, ending 2Q16 at 3,478 new home starts. Annual closings saw a slight QoQ decrease of 2.1% and a small increase of 1.9% YoY to end the quarter at 3,160 closings.

“The Philadelphia region has seen much improvement over the first half of 2016 and, overall, there are clear signs of new home expansion in the region,” said Syhapanya. “There still remains a concern over the market even with many housing indicators trending in a positive direction, but caution is to be expected with uncertainty in the global economy and this being an election year. Millennials are starting to look at the housing market, whether new or resale, and this group will be important for the continued expansion of the housing market.”

For further analysis of the Philadelphia region, contact regional director Quita Syhapanya: [email protected]