“Combination.” Not “merger.” Not “purchase.” Not “takeout.” His use of the term “combination” sounds neither practiced nor political when it crosses his lips, but rather his most precise way to say what the teaming of two of home building’s Top 5 companies factually represents in his mind. Far be it for the native of the west of Baton Rouge speck of a place called Brusly, La., who put himself through Louisiana State University by working at his dad Richard Sr.’s hunting, fishing, and sporting goods store, to mean something more along the lines of “the old one-two.”

What struck Bill Pulte—who started his eponymous company at age 18 in 1950—about the process re-engineering expert when they met in September 1994 was that the then-29-year-old Dugas was “someone with high integrity, high intelligence, and someone worth keeping an eye on.” Pulte did just that. Dugas “moved quickly through the ranks because he would win discussions by using facts, not just words, to back up his points of view.”

Not debates or arguments, mind you, but discussions. So, when Richard Dugas Jr. uses the word “combination” to describe what may be home building’s most momentous M&A deal ever, it’s clear he means just that.

What he and Pulte Homes have already gotten from the combination is a veritable one-two punch of product position and land position that immediately adds both geographic and price-point opportunity, not to mention a pile of cash, one less fierce competitor, a brand platform, a best practices operating system, and a culture awash in talent.

What he wants pronto from the deal is a faster ramp to profitability for the first time in almost 10 consecutive fiscal quarters, when home building did its cliff dive in late 2006. An all-stock purchase that came with Centex’s $1.7 billion cash trove, plus communities full of the kinds of inventory that was scarce at Pulte—entry-level new homes—gave Pulte both a near and a long-term reason to covet bringing Centex into the stable.

“Short term, this is about profitability,” says Dugas. “It’s about taking the $350 million a year that we outlined publicly and achieving those synergies in rapid order in order to bring the company back to profitability. It’s not a whole lot more difficult to explain than that.” Still, Dugas adds, “Both companies have downsized; yet neither company was profitable on a stand-alone basis. The opportunity on an annualized basis to take that amount of money out—because of what the combination affords us—is the best short term.” Note there he uses the word in context.

CFO Roger Cregg, Pulte’s almighty keeper of the balance sheet, further enlightens Pulte’s bid for an accelerated return to sustainable quarterly profits, which he says, will enable Pulte to “rebuild equity.”

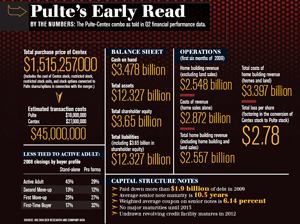

“We’ve got a lot of deferred tax assets that have zero value on the books right today,” says Cregg. “Our ability to get to profitability will untap about $1.3 billion in deferred tax assets—but it also has a $1.3 billion valuation allowance against us—so it’s really zero on the books. If we can demonstrate profitability going forward, we’ll be able to bring that back on book and improve our overall leverage position from where we are today.”

TALKS AND DEALS This particular combination evolves out of a constant continuum of conversations among home building executive management, ranging from relatively indifferent tire-kicking to full-on due diligence.