A new Pew Research study turned heads last week, and you can understand why. The study looks at household composition, and specifically at the eye-popping increase over the past 34 years in households that host multi-generational family members. The number doubled since 1980, from 28 million to 57 million–or upwards of one in five U.S. households, which is probably one of the most dramatic household demographic shifts since the era of the two-income household.

The Pew analysis, plus day-after reports in the Wall Street Journal by Laura Meckler, here, and Bloomberg/ BusinessWeek by Zara Kessler, here, tie the multigenerational phenomenon to various drivers, both economic and cultural.

We have witnessed Lennar seize an marketing high-road position with its NextGen two-homes-under-one-roof value proposition, essentially taking a double-master-down to its logical strategic endgame. Most home builders now offer floor plans that can adapt to “integrated” cross-generational use, and flexibility in meeting the need to do so occurs virtually at the subdivision level.

The questions we have fall into two general areas, especially since we see community and home design and engineering strategies among production builders and developers veering toward a greater and greater commitment to multigenerational product and marketing development: 1) Is multigenerational going to criss-cross with the married-with-children traditional nuclear household as the primary household type? and 2) What operational characteristic will it take for home builders to gain a competitive edge as households morph increasingly from traditional to unconventional, from scale-able to increasingly targeted, from multi-tiered economically, to less so?

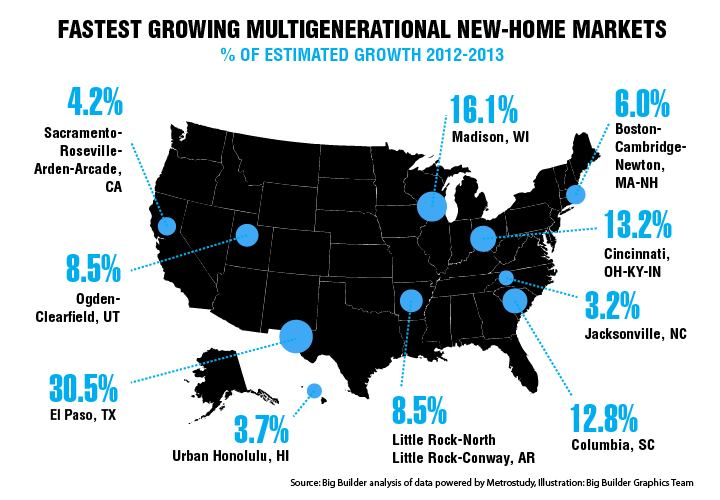

To that end, we set about looking to understand better the geography of multigenerational new-home growth. Here’s a look at a mash-up of data points our own Katie Gloede put together, followed by her explanation of how she solved for what she got.

Here’s how we got our map. For the top 10 growing multi-generational markets, first, we started rankings from the top 100 markets for new-home closings in 2013, powered by Metrostudy Builder Insight. Then, we calculated the percent of new homes sold to three or more adults of all new homes sold with demographic data. Finally, the markets are ranked by the percent growth in closings to households of three or more adults between 2012 and 2013.

There are myriad issues here for home builders and developers.

1. The emergence of “non-traditional” as the new home household composition type of the present and the future

2. The importance of multicultural strategy, research, development, and customer care programming to understand and deliver on the present and future demand universe

3. The economic drivers of multigenerational living, including health finance, student debt, and an anemic jobs recovery

4. Not all multi-gens are created equal, as some are Baby Boomers and their parents and many are Baby Boomers and their children, while a few are Baby Boomers and both

Submarket analysis and diligence, community by community, will need to get smarter and smarter so that a home builder or developer might get out in front of where the opportunities are for multigen new neighborhoods.

And the operational characteristic we see getting highlighted as this phenomenon emerges–even if multigenerational households don’t grow at the same rate over the next three decades as they have in the past three–is nimbleness. The ability to spring assertively and ably to action once a real opportunity pops up is and will be a cost-of-doing-business trait among home builders we continue to hear about and cover.