Little more than a week and change remains before the loan limits on mortgages eligible to be purchased by the GSEs or insured by the FHA reset Oct. 1. Despite a clarion call from the NAHB and other industry groups like the NAR to lobby for an extension of the current higher limits, the efforts may be too little too late to avoid a reset in the immediate. In the words of one public home builder CEO during a recent earnings call, an extension is “not hopeless, but it is a long shot.”

Some markets clearly will be more affected by the GSE and FHA loan limit resets than others by virtue of where median home prices fall on the spectrum. But as Big Builder’s John McManus pointed out in a recent blog, maybe a truer estimation of fallout focuses less on specific submarkets or price points and more on the buyer segment

“Most of the focus on the loan limitations has been in the more expensive markets, where doubtless, sales of homes in these markets would be lost.

But a home building executive tells us that the lost sales won’t only be in the expensive cities, since Federal Housing Administration-, Fannie Mae-, and Freddie Mac-backed loans get made on many a move-up and second-time move-up home that has been one of the few bright spots in the new-home business for the past nine months.”

It’s hard to ignore the value of the move-up buyer in today’s new-home economy.

I recently caught up with my colleague Jonathan Smoke, executive director of research for Hanley Wood Market Intelligence (HWMI), on this issue. According to his research, in the year following the federal home buyer tax credit expired, the move-up buyer has been outmuscling the entry-level in terms of share of dollars put toward home purchases.

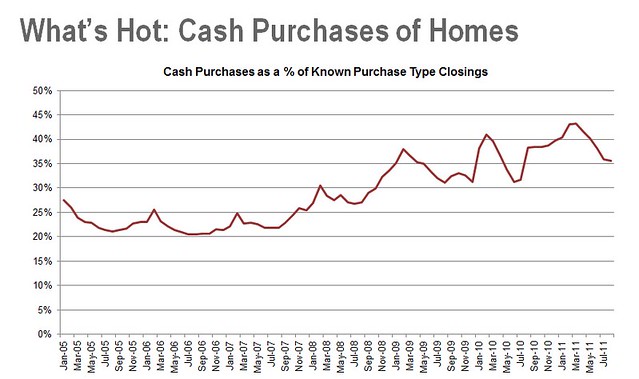

Typically move-up buyers have more cash to put toward a new home. Consequently, it would be expected that, as the move-up buyer segment has strengthened, there’d be an uptick in all-out cash transactions. Smoke said that trend has indeed surfaced; since 2007, cash purchases have grown in share as underwriting standards have tightened.

Typically move-up buyers have more cash to put toward a new home. Consequently, it would be expected that, as the move-up buyer segment has strengthened, there’d be an uptick in all-out cash transactions. Smoke said that trend has indeed surfaced; since 2007, cash purchases have grown in share as underwriting standards have tightened.

However, Smoke said that although all-cash transactions are on the rise, most move-up buyers still rely heavily on financing. Often they are using their cash to pull together larger down payments rather than fund the entire transaction.

However, Smoke said that although all-cash transactions are on the rise, most move-up buyers still rely heavily on financing. Often they are using their cash to pull together larger down payments rather than fund the entire transaction.

Given the surge in cash purchases, it’s arguable that the loan limit resets won’t be that big of a deal. The market functioned before the loan limits were raised, so it’s possible that that libertarian forces will ensure its functioning after the reset. But I’m not entirely convinced.

Let’s just review a few facts about today’s for-sale housing market: (1) today’s home buying market is all about the move-up buyer, (2) move-up buyers still need financing, and (3) the new loan limits are likely to most affect higher-priced markets, most often characterized as move-up markets. Given that combination of truths, is it reasonable to expect the market to move forward without a hiccup post loan limit reset?

To be clear, I hardly anticipate the market to come to a complete standstill on Oct. 1 because of the resets. However, I am guessing that it may take a bit of time for the market to resettle. It’s just hard to ballpark how long that adjustment period may take. I’ve got my fingers crossed for a rather quick and painless correction.

But even as the housing market absorbs the loan limit resets, financing constraints are likely to still be a big hurdle for home sales. Cash certainly has become a top source of buyer financing, but outside of that, the pickings are much slimmer. A number of financial institutions have majorly backed off residential mortgage lending. Bank of America is the most notable as it has cut its share of the mortgage market by more than two-thirds, even 86-ing its partnership with KB Home to provide buyers financing. JPMorgan Chase and Sun Trust also have pulled back on mortgage lending, leaving share up for grabs for players like Wells Fargo, MetLife, and even select builders’ mortgage units. But just how big their appetites are for this kind of lending is uncertain at this point.

It surprised me to see a number of builders’ mortgage units on the list of top financing sources. It’s always seemed that they were considered an ancillary business, a way to pocket a little extra revenue from transaction fees. But now, as financing options have narrowed, they may be a lifeline for builders in the absence of volume.

It surprised me to see a number of builders’ mortgage units on the list of top financing sources. It’s always seemed that they were considered an ancillary business, a way to pocket a little extra revenue from transaction fees. But now, as financing options have narrowed, they may be a lifeline for builders in the absence of volume.

Mortgage financing is clearly in a state of flux. From underwriting standards to loan limit resets, the industry’s major stakeholders are in the process of figuring out who’s in and who’s out of the business. Until that all shakes out, financing will continue to delay and derail home sale transactions, leaving uncertainty as a prevailing market force.