The big fish in the home building industry have been feasting on the little fish in the industry, and even on each other, for years. And a similar feeding frenzy has also been taking place in the industries that manufacture, distribute, and install building products in the homes the big fish build.

Instead, expect it to pick up again as the market nears bottom and to accelerate when it turns back up.

The Drive To Consolidate

Big builders sit atop of both the housing food and supply chains. Industry consolidation is being driven by the quest for market share, capital access, land control, and economies of scale. And it’s being fuelled by the large public builders’ newfound ability to raise long-term corporate debt at attractive rates and reinvest their enormous free cash flows at rates of return far above their cost of capital. Big builders seized on a powerful model this past decade: Allow local control, align generous compensation with corporate objectives, and bring to bear corporate support including deep pools of capital to once capital constrained smaller entities.

That all of this accelerated during an unprecedented boom in the housing market is not an accident. Big builders were spinning off a lot of cash, the cost of borrowing reached new lows, and the exigencies of tying down land to meet growing demands drove them to pick up land quickly by acquiring companies that had it. Sellers, meanwhile, sensed an opportunity to cash out on their equity and, if they chose, stay on and tap the deep capital pools and rich compensation plans the large builders had to offer.

Indeed, an argument can be made that the companies bought were worth more to the buyers than the sellers, because buyers were buying not just home building operations but regional diversification and the ability to achieve economies of scale in purchasing and production. In addition, when a smaller company runs out of financing headroom, it is worth more as part of a large company with deep pockets. Matches were made out of economic logic if not heaven.

Consolidation is a fact of life in a fragmented industry like home building where capital is increasingly king because of land acquisition, development, and construction costs. While custom builders can rely on the financing their customers provide, other builders cannot. Even though competitive pressures may not immediately drive smaller builders to sell, their more limited access to capital, the inherently greater risks of operating in a single market, and the desire of many family-owned businesses to cash out on all or some of their business equity, creates buying opportunities for acquisitive companies.

The Results Of Consolidation

A steady diet of acquisitions has allowed the big fish to grow, diversify risk, and gain ever expanding competitive advantages over the thousands of smaller companies that remain in the water. An interesting by-product of all this acquisition activity and the scale it has permitted large builders to achieve is more discipline and stronger balance sheet strength. To preserve their cost of capital and debt raising advantages, big builders are managing their businesses in more prudent ways than in the past, maintaining healthy cash balances and limiting leverage.

More of an intentional by-product, large builders are now regionally diversified, better able to withstand sharp regional downturns and control land and positioned to squeeze efficiencies from the supply chain. Although they are by no means fully insulated from the vagaries of market conditions, they are more likely to have the cash, financing capacity, and flexibility to gain share coming out of market downturns.

Supply Chain Consolidation

Meanwhile, consolidation in the supply chain is being driven by the same set of forces. Many industries in the building products sectors (such as windows and doors) and in the building materials sector (such as aggregates) remain fragmented, creating roll-up opportunities. Companies achieving scale in these industries gain economies that place competitive pressure on smaller producers. Even where this is not the case, large companies may perceive synergies from mergers and acquisitions by eliminating general and administrative expenses and costly competition or overcapacity in contested market areas.

But the drive to consolidate in the supply chain has an added spin.

Consolidation among the builders at end of the food chain is placing pressure on suppliers and distributors to achieve the national coverage and deliver the efficiencies and lower prices that large home builders increasingly have the clout to demand.

Delivering efficiencies and earning decent margins under price pressure is no small feat, especially for distributors. The material demands of a home are enormous. Hundreds of products and thousands of SKUs are required in every home and, in the stick-built world, must be delivered to thousands of scattered sites. To drive meaningful change, builders, distributors, and manufacturers must team up to eliminate costs and waste in the system. And this takes not only scale and focus, but also heavy investments in information, engineering, and construction management technology and services.

Both manufacturers and distributors are scrambling to make themselves relevant to big builders that demand a national footprint, turnkey services, and partners with deep pockets with whom to share construction defect and other building-related liabilities.

The distribution and turnkey construction businesses are still remarkably fragmented but recently less so with the spate of acquisitions by Stock and BMHC and the merger of Strober and Langoa that formed Pro-Build. Even the 800-pound gorilla, The Home Depot, has put its toe in the water, most noticeably with the acquisition of Williams Brothers.

When, Not If

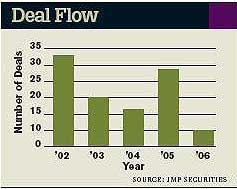

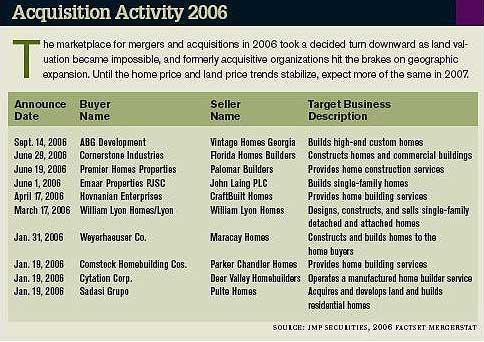

So the question is not if more consolidation will continue, but when and at what multiples. Current market conditions cast doubt on the timing and pace of consolidation in 2007. When the market is booming, companies are usually more willing to sell because they can name their price. When markets soften as much as they have recently, buyers adjust the prices they are willing to pay downward, and sellers who are not in a hurry to sell consider whether the timing is right to sell. But down markets also produce more distressed sellers–an eager buyer’s best bet. The downturn is hitting some regionally undiversified builders especially hard. When cash flows turn negative or credit gets crunched, the only escape hatch is a sale. Better to get the residual value of a failing operation than hand it over to banks all too willing to liquidate assets at cents on the dollar.

Under conditions like we face today, acquisitions tend to slow down, though they don’t grind to a halt. Both buyers and sellers need time to figure out what bets they want to place on the market’s direction. Buyers need to reassess the prices they are willing to pay, and sellers need to ratchet down the prices they are willing to accept. Because sellers do not relish the prospect of selling their companies for less than what they think their companies are worth, prices for well-run operations are sticky downwards. Meanwhile, because buyers smell blood in the water, they tend to circle longer around their prey, figuring they may be able to get a better price by patiently waiting–even the big fish may be weary of making significant investments in choppy waters. But when they perceive that the bottom of the market has arrived, many will strike.

Now financial buyers are circling the prey, too. Global liquidity is creating opportunities. Private equity funds are flush with cash and looking for places to deploy it. Hedge funds have lenders all too willing to provide them with the debt to do leveraged buyouts. Some headline private-to-private deals got done last year. More will likely follow, and it is feasible that a large public builder may get taken private.

In the short run, larger builders will likely lose market share as they aggressively move to clear out inventory and adjust to a market without speculators. But expect them to come out swinging and gain share when they can see a market turn in sight as well as when they are back in the open waters of a housing expansion.

–Eric Belsky is executive director at the Joint Center for Housing Studies at Harvard University.