Prognosticators of yore had it different. If what they foresaw turned out to be correct, they could stay in the prediction business for another season of prophecy fun and games. If, however, their forecasts strayed in some way from what eventually went down, were even a little imprecise, say, about the timing of the arrival of a plague or a rain storm, these seers typically wound up being a little dead.

So, it did not profit the prophet to be less than bold in his or her declarations of salvation or doom, victory or defeat, trouble or triumph ahead. If you’re going to lose your head if you’re wrong, even just a little wrong, or even thought to be just a little wrong, by all means, bold was the way to go with one’s predictions.

We’ll have none of this logical, incremental, evolutionary pussyfooting around that passes for forecasting these days. That’s like looking at tea leaves and uttering “Oolong” or “Darjeeling” and leaving it at that, which is only helpful if you’re allergic to or can’t stand the taste of Keemun.

Why go out on a limb at all if the limb is only three feet off the ground and there’s nothing to gain or lost if one falls?

So, no. Our predictions for the coming twelve-month stretch are not counterintuitive and contrarian merely for counter-intuition’s sake. Rather, it’s to recognize that anomalies—often in the form of extremes that defy norms—are more and more part of a business fabric that up to now hewed quite reliably and comfortably close to those norms. In ways, this time is different, and the trick is to try to not get wrapped around the axle arguing over the minutia of which ways are different, and which ones are a variation of cyclical themes of the past.

Our assumption is that the housing recovery we’re in bears significant resemblance—in ways we both see and don’t detect—to housing recoveries of the past century. What may differ fundamentally, however, is where this recovery is hitting against a broader economic backdrop of slowing aggregate demand in the United States.

Whatever. We believe that in some ways this housing recovery is different, and that only bold predictions on what may occur in the next year to 18 months will do justice to the speed and drama with which change is happening in the home building community.

First, think back. What—be honest, now–were you sitting there guessing would happen in your world this time last year?

I, myself, was quite off-base about 2013 as I looked from the vantage point of a year ago. My speculation gravitated in a biased way toward the groundbreaking, amped up forays among single-family players—namely Lennar and Toll Brothers—into more classic multifamily project work, including apartment towers and student housing. As well, the single-family for-rent model and the joint venturing of for-sale and for-rent players—Toll and Equity Residential, for instance, and Toll and Forest City—appealed to me as likely to characterize 2013 as a year of “hedging homeownership” in a definitional and business-model sense.

What I have to admit I failed to detect last year at this time was the already-brewing and bubbling capital market global barrage that would pump billions of institutional investment dollars into the believe that the housing parabola signaled the moment had come. Land, from that moment forward, would either be priced right for sale to people who wanted to buy a home, or would be priced right or wrong for a host of other would-be buyers, investors, and speculators looking for constrained assets to trade.

The freshly-sparked interest of worldwide investors to park themselves into an updraft in for-sale housing in the United States, and one result was emergence of seven brand new publicly-held home building companies, with a total market capitalization just shy of $5 billion, not to mention several billion more in added equity and debt in the already-extant public home builder set.

So, rather than 2013 signaling the “big hedge” vs. homeownership in strategic moves by home builders, the year, by our lights, testified to a good old-fashioned belief in the power of a cyclical upturn in for-sale housing, and that all the raw materials of pent-up demand, low supply, and accommodative financing were in place for a healthy, sustainable recovery trajectory.

In broad strokes, what occurred in 2013 was the result of hyperbolic activity among investors absorbing housing’s “overhang” of distressed and unaccounted for residential properties, followed by the “it’s safe now” set of primary residence seekers with the wherewithal to dispose of current properties so they could acquire the ones they wanted.

So, the beginning of the shift from an investor-fueled absorption impetus to individual buyers occurred in 2013.

Those first-time, second-time, and third-time move up buyers account for a number of the trends that occurred in 2013. Pricing, for one. The mix of sales, which sprang from heavily dosed with distress portfolio transactions, to higher-end individual purchases made everybody do a double-take when they saw the shift in prices from where they’d been to the newer levels.

Misperceptions abounded. Many observers said it was that the builders were being too aggressive with their pricing between this time last year and the end of the Spring. True, they were being aggressive with their pricing, but the fall-off in sales probably had more to do with tapping out the “move-up” segments of the market, and to some extent pulling them forward during the low-low-low interest rate periods, to the detriment of later months’ sales pace.

So, if you’re selling higher end homes to the higher-end market, the contrast in sales averages and medians from the earlier periods looks conspicuously dramatic.

Too much, too soon.

However, we feel the real imbalance kicked in as move-up buyers, and second-move up ones stopped being the ones with the most discretionary options. Instead, there came a cohort who actually needed to sell their homes in order to step up to the next purchase. Here’s where the rub is.

No entry-level, first time buyer market to speak of, which is the support base for most housing recoveries.

Until and unless there’s a robust entry-level housing market, this recovery’s momentum is subject to volatility and, potentially long stretches of anemic activity.

We’d say the year 2014’s biggest question for people in new-home building and development is whether—despite headwinds in housing finance regulation, household wage growth trends, corporate profitability and hiring patterns, household formation, and the increasing need for geographical flexibility—a fundamentals-based first-time buyer market can form.

We think yes.

We think yes, partly for this reason. You (see more on this below).

Here are our 10 bold predictions for 2014.

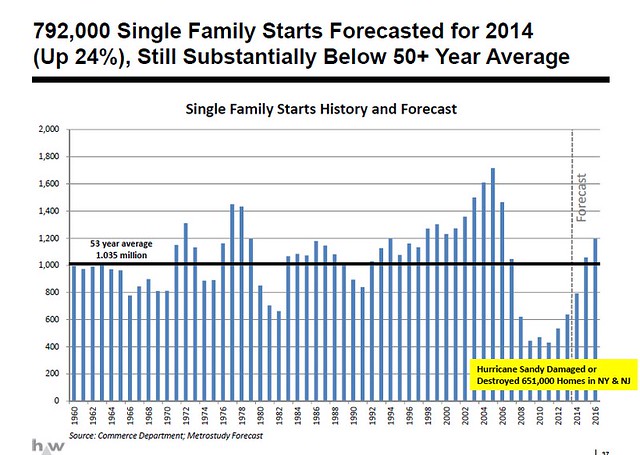

1. HYPER-LUMPY HOUSING STARTS: Single-family starts, says Hanley Wood chief economist Jonathan Smoke, are due to tap the breaks just short of 900,000 in 2014, busting through the one-million ceiling in 2015, on their way to 1.2 million in 2016. So, from a historical supply standpoint, next year will still feel like it’s contributing to even more pent-up demand rather than meeting it all. Our bold prediction is that an inordinate share of housing starts—one in four, we’ll guess–will concentrate in 20 or so geographical market arenas that continue to polarize as higher-income job producers.

2. ROBUST MERGERS & ACQUISITIONS: Need and need will both collide and converge here, fueling M&A partly because there’s an over-capacity in the over-all mechanisms for managing new home construction, and an under-supply of capital resources at the local store level. So, in a “fend for yourself” year, principals of privately-held companies will have to look hard at whether there may be diminishing returns on their current portfolios of owned land assets and access to new lots, and ponder whether they might just now get the maximum return on those assets because there are bigger well-capitalized companies still on the make for new communities and visible new incremental revenue. Our bold prediction: 15 to 20 small to medium-sized acquisitions in the next 12 months, and one-to-three mega-deals that combine companies with multi-regional holdings.

3. SCANT(ER) AD&C LENDING: Hey, we’re predicting, overall, a “fend for yourself” year. With risk-averse, Dodd-Frank rules and regulations kicking in at a new level in the early part of 2014, we don’t see an outpouring of enthusiasm among traditional regional bank lenders in the land acquisition and development lending space. Private home builders are going to have to tap their imaginations, their country-club investors, and their own bank accounts in order to stay in the game in 2014. Bold prediction: a new initiative that would increase the attainability–if not affordability–of acquisition and development funding for private home builders may see the light of day in the first couple of months of 2014. This could be a game-changer for private builder prospects. Otherwise, we’ll up the M&A number above by 25% to 30% more than we’ve estimated.

4. MORTGAGE FINANCE CIRCUS: Again, it’s “fend for yourself” time in home mortgage lending land. Banks are girding for new qualified mortgage and qualified residential mortgage rules and regulation, servicers are still convulsing from the non-stop binge of federal and local liability issues that stalk them since the housing crisis days, and consumers themselves continue to be plagued with uncertainties in job security and wage growth. The good news is households have done well at reducing their debt-laden balance sheets. The bad news is that when Joe the Plumber’s apprentice can qualify for a mortgage, things will start to look different for housing’s first-time buyer market, but probably not until then. The bold prediction here is that it won’t be long into 2014 before some high-volume builders really start to bore into BIG DATA to understand which young adults are apt to be able to qualify and move into their first owned homes.

5. TOP (HEAVY) TOP MARKETS: The “new geography of jobs” continues to filter out the unwanted from the wanted in terms of arenas to focus on for new housing and development. Here’s access to Metrostudy’s “healthiest markets” for 2014. The bold prediction here is that we see fiercely aggressive mergers and acquisitions initiatives in every single one of the top 20 healthiest markets, as community count growth, access to new home buyer learning, and gross margins suggest outsized potential in these markets where demand will eclipse supply for the foreseeable future. A subset of that prediction is that builders will overpay for lots in these markets, which means “there will be blood,” especially if it’s private home builders who overpay.

6. LAND PLAY TRADE-OFFS: Bold prediction here is that some of the bigger acquisition outlying-area plays of the past 12 months will wind up getting traded in for smaller, closer-in, more complex deals, where re-densification, and new more efficient product programs will allow for-sale builders true access to the up-and-coming young adult market. Yes, active adult and second- and third-time move up will be critical to the “fend for yourself” year. But the breakthrough will be products, programs, and land deals that forcibly pull renters out of apartments into new affordable urban, or urban-like communities.

7. ‘FEND FOR YOURSELF’ DESIGN: Here’s where the bold predictions shift from reactive mode to aggressive. “Fend for yourself” era design makes different assumptions. One, high-performance in a home–energy, water, health, and sustainability features–will each get called out on a price sticker like a new car’s MPG rating, and go into the appraisal and loan qualification valuation of the home. Two, a true primary-residence home vs. a home to flip as an investment, triggers different motivations in the buyer. A buyer who plans to live there for a while, wants it truly livable for him or her, not counting the “exit” as so important. So, contemporary feeling design that is simpler, more open, more flexible, and less cluttered will emerge in more and more forms, and traditional, classically substantial elevation and floorplan featuring will become less alluring.

8. TARGETED SALES & MARKETING: Hands down, the biggest, boldest prediction we can make this year on the sales and marketing front is that technology-driven, man-and-machine intelligent targeting will be one of the foundational changes in home building in the coming 12 months. The ability to get visibility into who’s graduating from STEM-based masters programs, who’s moving to which zip codes, who’s searching which web sites, etc. and match your program to his or her home preferences is one of the community’s one-day no-brainers. Someone, too, this coming year, is going to breakthrough and do something along the lines of what Pulte’s doing to test-market homes at the pre-community and construction level to draw how minimum value propositions and optimal value-creation opportunities.

9. OPERATION MARGIN-CAPTURE: Like sales and marketing, there’s nobody better than the well-capitalized multi-regional home builders to explore advanced technology production and distribution systems at the site level. Robotics, big data, building information modeling, logistics, drones, what have you. The 2014 “fend for yourself” year, thanks to growing margin pressures form labor and materials costs, may be the year that technology makes real headway into operations management, to take some of those local costs off the table.

10. PEOPLE: Have you been through this yet? Try looking at the job descriptions of 60% to 70% of the people you’ve got working for your organization and see how well they match up to what is required of them to make the business fly in the coming year. We have to do the same exercise. It’s not that you necessarily have the wrong people working there. It’s that the world of what they do to make a living and make your organization win has changed, big time. Our bold prediction here is that managements are going to have to go through and re-write more than three-quarters of the job descriptions of associates just to get them current with the way knowledge, skills, capabilities, and potential have evolved in the past five years.

Will the Fed still be talking taper? Yes, and hopefully the markets will be functioning well and strong enough to warrant a cut back in the amount of Uncle Sam stimulus required to keep them toiling toward unaided normalcy. Will the threat of government shutdowns and other political impasses continue their stranglehold on sane policy development? Hmmm, that’s a tough one. Will six or seven more privately held companies sell a piece of themselves to the public through initial public offerings of stock? Maybe one or two more. But where does that leave another handful of companies whose private equity and hedge fund investor groups covet an exit strategy? Clearly, we’ll see some action on the mega-deal front.

But, we’re relatively sure that what will characterize the year ahead will be a “you’re on your own, don’t ask me for help” mode. If you can survive, thrive, and dominate next year, there’s a good little stretch awaiting in the years after that.

I’ll bet my neck on it.

Also: TICK, TICK, TICK: time’s ticking away, and this is the week we’re completing our research on “home building’s 10 most influential women executives” in 2013. Go to the post; check out the list; add to it; tell us what we should be looking at for judging criteria; give us your thoughts. This is a moment to focus on a leadership talent pool that deserves attention and growth opportunity now, not later.