The Census Bureau spewed forth data that had been pent-up since the October government shutdown, and whoa, the news was favorable to believers in a steady recovery in 2013.

Here’s a pop from the Wall Street Journal’s Jonathan House and Jeffrey Sparshott to give you a sense of the mainstream business media take on the data print from the Commerce Department.

Here’s the top line from the Census Bureau release:

BUILDING PERMITS

Privately-owned housing units authorized by building permits in November were at a seasonally adjusted annual rate of 1,007,000.

This is 3.1 percent (±1.1%) below the revised October rate of 1,039,000, but is 7.9 percent (±1.6%) above the November 2012

estimate of 933,000.

Single-family authorizations in November were at a rate of 634,000; this is 2.1 percent (±1.1%) above the revised October figure of

621,000. Authorizations of units in buildings with five units or more were at a rate of 346,000 in November.

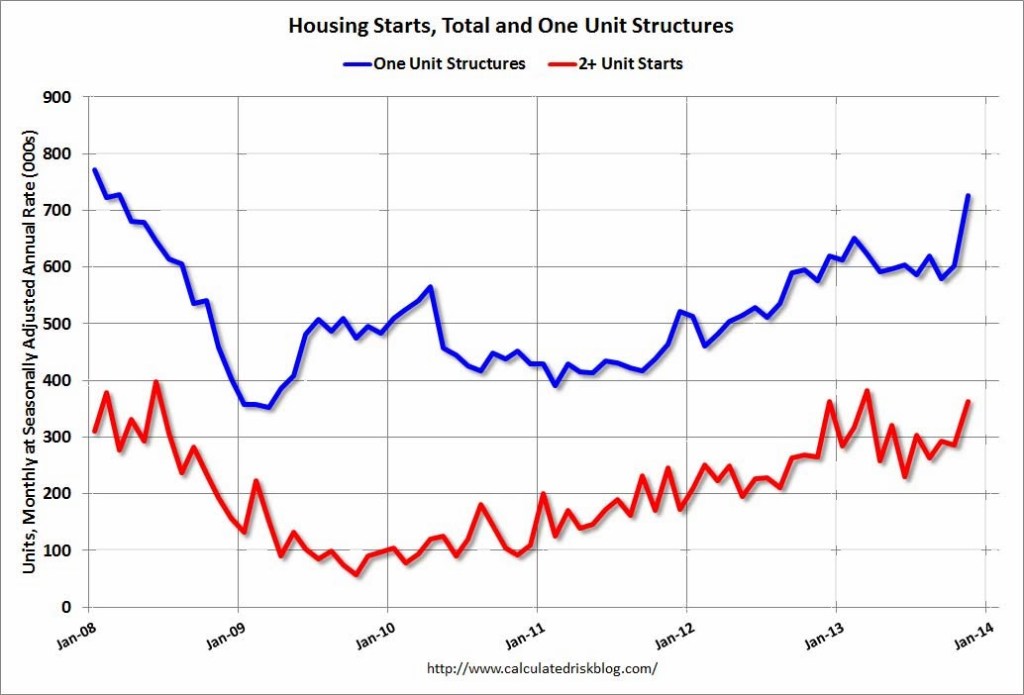

HOUSING STARTS

Privately-owned housing starts in November were at a seasonally adjusted annual rate of 1,091,000. This is 22.7 percent (±13.2%)

above the revised October estimate of 889,000 and is 29.6 percent (±19.8%) above the November 2012 rate of 842,000.

Single-family housing starts in November were at a rate of 727,000; this is 20.8 percent (±10.7%) above the revised October figure of

602,000. The November rate for units in buildings with five units or more was 354,000.

HOUSING COMPLETIONS

Privately-owned housing completions in November were at a seasonally adjusted annual rate of 823,000. This is 0.1 percent (±9.5%)*

below the revised October estimate of 824,000, but is 21.6 percent (±11.3%) above the November 2012 rate of 677,000.

Clearly, in the noise-vs.-signal shortsighted media cycle, today’s numbers reflect a sudden 180-degree turn to the positive in housing momentum, after so recently, reporters and analysts were ready to bang a nail into the coffin of the recovery in October and November.

However, it’s not really the case. What happened is that varying components of the demand pool have been impacted to varying degrees by interest rate gyrations, price sensitivity, credit access constraints, policy uncertainty, and supply availability, all under-arched by some structural questions about the ability of a jobs and income recovery to broaden beyond a rather finite set of geographies and industries.

Hits to the demand stream notwithstanding, a significant part of it has remained functionally intact. What hasn’t really sprung yet is the entry-level, first-time buyer domino. It’s this portion of home buyer-dom that gives demand its soundest base, and it’s these buyers who are the most sensitive to interest rate creep, price-point creep, jobs insecurity creep, and policy (i.e. Dodd-Frank lender rules and guidelines on ability-to-pay, etc.) creep.

Presumably, part of the first-time entry-level buyer population can qualify, wants to own, and sees interest rates and prices as still low enough to go for it rather than pour money into rent.

For pro housing observers, the Commerce Department figures come as a surprise neither to the up nor the downside.

I am not surprised to see the uptick in the government’s number, because we have been seeing strength in our own starts numbers all year. Even with the ‘pause’ in home sales, our data on housing starts have shown a continued upward trend,” says Brad Hunter, Metrostudy chief economist and director of consulting. “Putting this number in context, builders have recently experienced a slower pace of sales, but our expectation is that new home sales will revive in the next six months. Builders appear to be hopeful as well.”

Here’s a quick take from Calculated Risk’s Bill McBride:

This was well above expectations of 952 thousand starts in November. I’ll have more later … but this was a solid report.

As with national data releases of any sort, the helpfulness of starts and permits data in decision-support is limited at best. What the print does is to signal to investors, both domestic and global, that a cyclical housing recovery remains on track, held up in timing and trajectory only by household income trends at the entry-level end and credit access for both prospective home borrowers and builder/developers.

Fundamentals are moderately–not massively–supportive. Housing is healing.

Check back at this space for one more update later today.